Polaris designs and manufactures powersports vehicles in the United States, Canada, and internationally. Its founders pioneered an early snowmobile in the 1950s, leveraging the company’s strength in powertrain, manufacturing, and distribution. Polaris then expanded its vehicle offering, targeting military and commercial applications.

The company now provides a full-range lineup including utility and side-by-side vehicles, motorcycles, and boats. It also offers accessories such as wheels and tires, lighting and audio systems, and gear and apparel. Polaris markets its products through distributors as well as via e-commerce marketplaces.

The Zacks Rundown

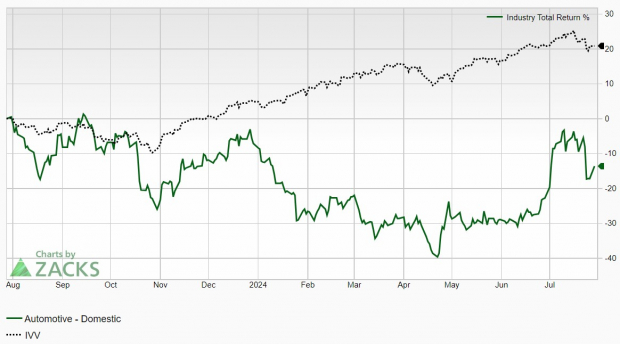

Polaris PII, a Zacks Rank #5 (Strong Sell), is a component of the Zacks Automotive – Domestic industry group, which currently ranks in the bottom 33% out of approximately 250 Zacks Ranked Industries. As such, we expect this industry group as a whole to underperform the market over the next 3 to 6 months, just as it has over the past year:

Image Source: Zacks Investment Research

Candidates in the bottom tiers of industries can often be attractive short candidates. While individual stocks have the ability to outperform even when they’re part of a lackluster industry, the inclusion in a weaker group serves as a headwind for any potential rallies and the journey forward is that much more difficult.

Along with many other auto stocks, PII shares have been struggling this year while the general market reached new heights. The stock is hitting a series of lower lows and represents a compelling short opportunity as we head deeper into the latter half of the year.

Recent Earnings Misses & Deteriorating Outlook

The Medina, Minnesota-based company has fallen short of earnings estimates in three of the past four quarters. Just last week, Polaris reported second-quarter earnings of $1.38/share, missing the $2.27/share Zacks Consensus estimate by -39.2%.

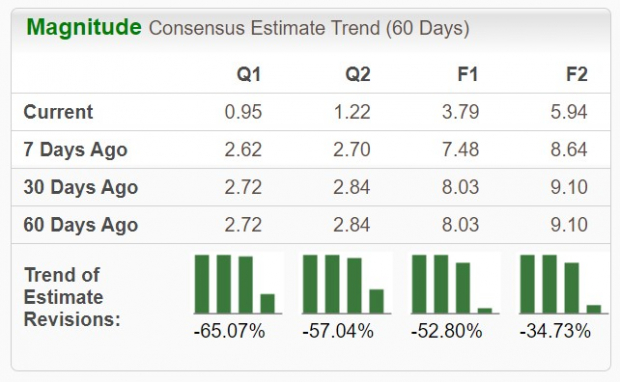

Consistently falling short of earnings estimates is a recipe for underperformance, and Polaris is no exception. The powersports vehicle provider has been on the receiving end of negative earnings estimate revisions as of late.

Looking at the full year, analysts have slashed estimates by -52.8% in the past 60 days. The 2024 Zacks Consensus Estimate is now $3.79/share, reflecting negative growth of -58.6% relative to the prior year.

Image Source: Zacks Investment Research

Falling earnings estimates are a huge red flag and need to be respected. Negative growth year-over-year is the type of trend that bears like to see.

Technical Outlook

As illustrated below, PII stock is in a sustained downtrend. Notice how the stock has continued to meet resistance at its 200-day moving average (red line). Also note how both moving averages are sloping down – another good sign for the bears. A recent uptick presents an appealing entry for a potential short position.

Image Source: StockCharts

Polaris stock has also experienced what is known as a “death cross,” whereby the stock’s 50-day moving average (blue line) crosses below its 200-day moving average. Shares would have to make an outsized move to the upside and show increasing earnings estimate revisions to warrant taking any long positions. The stock has fallen more than 35% over the past year.

Final Thoughts

A deteriorating fundamental and technical backdrop show that this stock is not set to power its way to new highs anytime soon. The fact that Polaris is included in one of the worst-performing industry groups provides yet another headwind to a long list of concerns. A history of earnings misses and falling future earnings estimates will likely serve as a ceiling to any potential rallies, nurturing the stock’s downtrend.

Potential investors may want to give this stock the cold shoulder, or perhaps include it as part of a short or hedge strategy. Bulls will want to steer clear of PII until the situation shows major signs of improvement.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpPolaris Inc. (PII) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.