A successful company eventually reaches the point where its best growth days fall behind it, and investors must grapple with what the stock will be moving forward. Enterprise software company Salesforce.com (NYSE: CRM) could be in the beginning stages of this soul-searching process with investors. The company was one of the first successful software-as-a-service (SaaS) stocks and has generated staggering 4,300% gains over its lifetime.

The company's $180 billion market cap could make the next 4,300% very difficult, but here are three reasons why Salesforce.com is still a stock worth buying today.

1. Growing the size of its pie

Salesforce.com started as a customer relationship manager (CRM), helping companies store information about customers, follow leads, and track their sales process. The company's cloud-based product was a hit, and it's been the world's No. 1 CRM software by revenue for the past nine years.

But over time, Salesforce.com began to expand its capabilities, using its CRM presence to start offering new products to its customers. Today, Salesforce.com is a diverse platform that touches marketing, sales, commerce, communications, and more. It bought collaboration platform Slack for $27 billion in late 2020, giving users an alternative to email and other traditional communications.

Management estimates that its global addressable market will grow to $284 billion by 2026; the company's $28 billion in revenue over the past four quarters underlines the ample room for future growth.

2. Steady, profitable growth

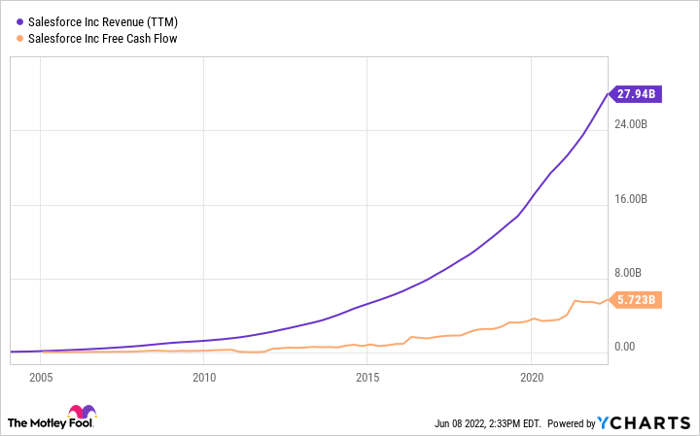

CRM software essentially guides a company's daily operations on the sales side of the business, which makes it extremely important. Below, you can see how resilient Salesforce.com's revenue has been over the years; the growth chart below shows a nearly perfectly smooth growth curve. Revenue has grown an average of 27% per year over the past decade.

CRM Revenue (TTM) data by YCharts.

Better yet, Salesforce.com is profitable, so growth isn't coming at the expense of the bottom line. Today, the business converts roughly $0.20 of every revenue dollar into free cash flow, which has helped fund numerous acquisitions.

Salesforce.com has become an enormous company; how much longer can the business grow at such a high rate, given its size? It's typically easier to grow from $2 billion to $20 billion than $28 billion to $280 billion. Management is guiding for 20% year-over-year revenue growth for the fiscal year 2023, ending Jan. 31, 2023.

Investors will need to wait and see whether this is a temporary slowdown, or if the business is maturing, easing to a slower rate. Only time will tell.

3. Shares have become a bargain

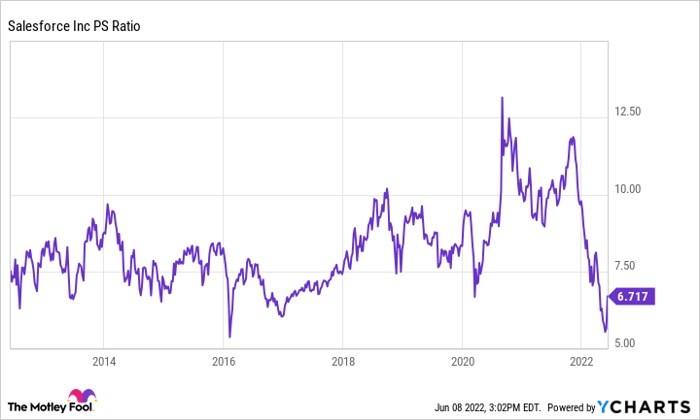

Market turbulence has brought the stock's valuation to near-decade lows. The stock's price-to-sales ratio has fallen by almost half, to just under 7. Investors buying the dip and expecting the stock's valuation to spring back to near highs could be asking for disappointment. Inflation is soaring, and the market seems reluctant to award sky-high valuations to stocks anytime soon.

CRM PS Ratio data by YCharts.

Investors would risk seeing shares punished if revenue growth slowed while trading at such a high valuation, but it seems the bear market has taken care of that already. Investors might instead see the stock rise in sync with revenue growth, since Salesforce's valuation has already reset to a lower level.

That would likely mean double-digit annual investment returns, barring a complete implosion by Salesforce.com, which doesn't feel probable given its consistent growth over the years. The stock might not grow 4,300% anytime soon, but it seems like a compelling opportunity to buy a proven compounder.

10 stocks we like better than Salesforce, Inc.

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Salesforce, Inc. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of June 2, 2022

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Salesforce, Inc. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.