Heico (NYSE:HEI) is set to give its latest quarterly earnings report on Tuesday, 2025-05-27. Here's what investors need to know before the announcement.

Analysts estimate that Heico will report an earnings per share (EPS) of $1.04.

The market awaits Heico's announcement, with hopes high for news of surpassing estimates and providing upbeat guidance for the next quarter.

It's important for new investors to understand that guidance can be a significant driver of stock prices.

Overview of Past Earnings

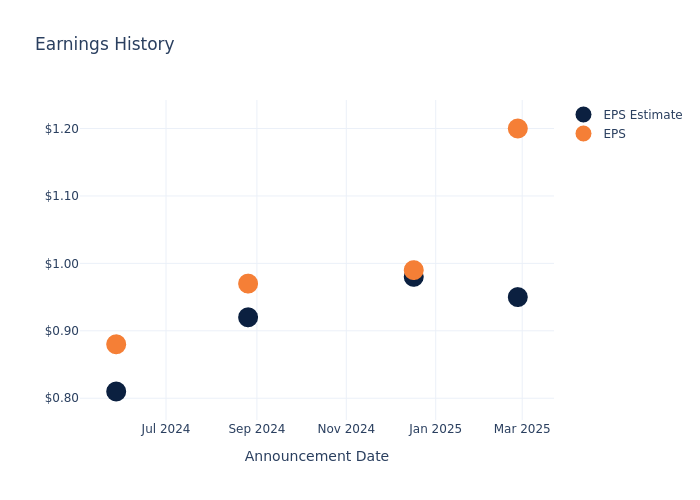

During the last quarter, the company reported an EPS beat by $0.25, leading to a 13.88% increase in the share price on the subsequent day.

Here's a look at Heico's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 0.95 | 0.98 | 0.92 | 0.81 |

| EPS Actual | 1.20 | 0.99 | 0.97 | 0.88 |

| Price Change % | 14.000000000000002% | -9.0% | 1.0% | 0.0% |

Heico Share Price Analysis

Shares of Heico were trading at $267.08 as of May 22. Over the last 52-week period, shares are up 26.41%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analyst Observations about Heico

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Heico.

With 3 analyst ratings, Heico has a consensus rating of Buy. The average one-year price target is $271.67, indicating a potential 1.72% upside.

Analyzing Ratings Among Peers

The below comparison of the analyst ratings and average 1-year price targets of and L3Harris Technologies, three prominent players in the industry, gives insights for their relative performance expectations and market positioning.

Overview of Peer Analysis

Within the peer analysis summary, vital metrics for and L3Harris Technologies are presented, shedding light on their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| L3Harris Technologies | Buy | -1.52% | $1.35B | 2.00% |

Key Takeaway:

Heico is positioned at the top for Revenue Growth among its peers, with a positive growth rate. It is also leading in Gross Profit margin, indicating strong operational efficiency. However, its Return on Equity is lower compared to peers, suggesting potential for improvement in utilizing shareholders' equity. Overall, Heico is performing well in key financial metrics compared to its peers.

About Heico

Heico is an aerospace and defense supplier that focuses on creating niche replacement parts for commercial aircraft and components for defense products. In commercial aerospace, Heico is the largest independent producer of replacement aircraft parts. In the defense market, the company produces niche subcomponents used in targeting technology as well as simulation equipment, among other categories. It operates as two segments: the flight support group,or FSG, and the electronic technologies group, or ETG, both of which supply the aerospace and defense sectors to different degrees. The company is persistently acquisitive, focusing on companies in similar or adjacent markets that are generating strong cash flow and profitable growth potential.

Heico's Economic Impact: An Analysis

Market Capitalization Analysis: Below industry benchmarks, the company's market capitalization reflects a smaller scale relative to peers. This could be attributed to factors such as growth expectations or operational capacity.

Positive Revenue Trend: Examining Heico's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 14.93% as of 31 January, 2025, showcasing a substantial increase in top-line earnings. As compared to competitors, the company surpassed expectations with a growth rate higher than the average among peers in the Industrials sector.

Net Margin: The company's net margin is a standout performer, exceeding industry averages. With an impressive net margin of 16.3%, the company showcases strong profitability and effective cost control.

Return on Equity (ROE): Heico's ROE stands out, surpassing industry averages. With an impressive ROE of 4.55%, the company demonstrates effective use of equity capital and strong financial performance.

Return on Assets (ROA): The company's ROA is a standout performer, exceeding industry averages. With an impressive ROA of 2.17%, the company showcases effective utilization of assets.

Debt Management: Heico's debt-to-equity ratio is below the industry average at 0.63, reflecting a lower dependency on debt financing and a more conservative financial approach.

To track all earnings releases for Heico visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Latest Ratings for HEI

| Date | Firm | Action | From | To |

|---|---|---|---|---|

| Apr 2025 | Truist Securities | Maintains | Buy | Buy |

| Apr 2025 | Wells Fargo | Initiates Coverage On | Equal-Weight | |

| Mar 2025 | Truist Securities | Maintains | Buy | Buy |

View More Analyst Ratings for HEI

View the Latest Analyst Ratings

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.