Credit: Shutterstock photo

Credit: Shutterstock photoBy Renoir Vieira :

Editor's note: Seeking Alpha is proud to welcome Renoir Vieira as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to the SA PRO archive. Click here to find out more »

Successful investors must have variant perceptions that turn out to be correct over time. This basically means an investor holds a strong viewpoint that is substantially different from what is priced in the market and which subsequently proves to be correct. In most cases, markets are efficient in assigning payoffs and probabilities to each and every scenario, and market prices reflect the net present value. Nevertheless, on occasions, markets do not exactly work as good predictors, and, therefore, market prices can deviate significantly from the expected net present value.

There is a very active line of research on the replacement of opinion polls for prediction markets where traders negotiate contracts in which the contract price reflects the probability of an event. Berg et al (2008, BRG ) show that the prediction markets outperformed polls by a factor in American elections. If that conclusion holds and prediction markets tend to outperform polls, there should be no reason for market prices not to accurately reflect the risk premium for each and every possible electoral scenario. However, multiple studies show that accuracy is highly affected by:

- average knowledge of the market participants on the subject - O'Leary (1999) and Rodrigues & Watkins (2009) show that for prices to converge, there is a critical point in which the average probability of traders' forecasts being correct is over 50%;

- events with intermediate probability (15%-60%) - according to Coles et al. (2007, CLS ) those are generally poorly priced ;

- liquidity and market manipulation - Forsythe et al (1999, FRT ) show that market participants have significant bias and Rhode et al. (2008, RHD ) show that in some cases a particular outcome may be especially important to some participants, in which case they may try to influence the market.

I believe that the Brazilian Presidential Election in October is an event that meets all three characteristics above: i) market participants' average knowledge of the subject is considerably low, and the event is surrounded by idiosyncrasies and one-offs ; (ii) there are several candidates from politically important parties which naturally implies candidates' chance of winning is in range between 15% and 60%, an interval in which events are generally poorly priced ; iii) liquidity in the Brazilian market is low in general and has been even lower in recent months, as there are market participants that have excessive pricing power and a probably biased view.

This is a unique election (but not that unique). There are many candidates, the leading candidate in polls, Lula, is in jail; in the second place a controversial right-wing candidate, Jair Bolsonaro; The alternative left-wing candidate, Ciro Gomes, has a history for bad temper and is viewed as unreliable by the establishment. Opinion polls are subject to intrinsic uncertainties, including whether or not the leading candidate will be able to run, and to what he will be able to influence voters. In this scenario, there are many conditional probabilities to estimate, no historical reference, time series or case studies. The lack of reference points contributes to the low average knowledge of market participants on the subject.

Considering that I am a market participant myself and I may also have my own biases, I think it is better to look objectively at the data available.

The Importance of Political Support

Around 70% of the Brazilian cities have 80% of their budget coming from external sources - the Municipality Participation Fund and Parliamentary Amendments. Brazilian cities are together the biggest employers in the country, they employ approximately 6.3 million employees (IBGE, 2012), which represents 77x more than Petrobras ( PBR ), 63x more than Banco do Brasil ( BDORY ), 140x more than Casas Bahia - one of the biggest Brazilian retailers... ok, you got it already.

This number includes only the direct employees, therefore, disregarding the indirect jobs generated by public works, outsourcing, and others. In many cities, the government is the biggest direct employer. In some cases, the number of public servants (considering Federal, State, and Municipal) exceeds 40% of the total number of employed persons. These numbers are even higher if you take into account the indirect jobs that are created by the public administration. Not surprisingly, for many cities, payroll exceeds 50% of their budget.

The reality of the municipal finances shows that any investments beyond the basic maintenance of the public services depend on Parliamentary Amendments. In 2018, each congressman will have redirected R$ 14.8 million from the Federal budget to cities and states. In total, the Congress will allocate R$ 8.8 billion discretionarily. Parliamentary Amendments committed per year has been growing over time (see chart below). These funds are destined to improvements in the area in which the congressman usually gets most support in elections. Of course, congressmen do not deploy those funds in a random, it is fairly reasonable to assume political affiliates get most, and in return, they provide political support in elections.

Source: Created by the author using data from the Congressional Budget Committee

The relevance of cities as big employers and regional economic agents shows the importance and potential influence of mayors in Presidential Elections. Candidates who can gather the support of mayors and congressmen - and therefore increase capillarity - have a huge advantage over the opponents. The importance of capillarity is greater than commonly acknowledged. The polls typically ask questions like: "If candidate X is supported by Y, would you consider voting for Y?". National polls, however, do not reflect the influence of mayors, congressman, etc.

TV x Social Media

There is a recurring argument that campaigning on TV has lost importance and because of that non-traditional candidates could have a fighting chance. There is some truth in this argument. In theory, the internet opens a path to direct communication with little (or no) mediation between the candidate and potential voters. It is possible that the importance of TV and radio time has decreased, but in assessing to what extent, it is important to consider some differences (source BMS ):

TV

- available in 90% of Brazilian homes;

- 63% of Brazilians name it as their main information source;

- 54% of people say they trust information displayed on TV always or most of the time;

- 35% of the electorate names it as the main media influencing their voting decision;

Internet

- available in 63% of Brazilian homes;

- 26% name it as their main media;

- 20% of people say they trust information displayed on the Internet always or most of the time;

- 20% of the electorate names it as the main media influencing their voting decision;

In a scenario where much of the electorate is undecided, TV and radio time is actually a key factor. The argument that TV and radio time may not have as much influence as before disregards the fact that in social media users have to take some kind of action such as clicking a link, reading a post, news etc., whereas TV and radio user experience is more passive, potential voters are exposed to the content. In addition, special broadcast which is aired by all Brazilian TV and radio stations two times a day, candidates also have ads aired throughout the TV and radio stations' regular schedule. Considering that 52% of people are little or not interested at all in the elections (see chart below), the risk is that candidates whose campaigns are based on social media will only reach their own supporters.

Case Study

It is worth analyzing the 2010 Presidential Election, in which Dilma was elected for the first time. The economy was booming, inflation was under control, the job market was in great shape, then President Lula was at the height of his power and influence... and even with all this in her favor, the number of votes Dilma obtained in the first round was similar to the sum of the votes that the candidates for Congress in her coalition obtained in the 2006 Congressional Elections. Surprisingly, this finding also holds for the coalition headed by Jose Serra (PSDB).

In 2014, even with Lava Jato at its peak, signs of recession and soaring inflation, the coalition party headed by PT managed to squeeze the majority of votes and Dilma was re-elected. Those cases support the hypothesis that removing the incumbent is by no means an easy task. The coincidence between the order of the votes obtained by the congressmen from the parties in a coalition and the votes obtained by the coalition's Presidential candidate in the subsequent election is very interesting and adds to the hypothesis that the parties in a coalition have a decisive impact on the electorate.

Garbage In, Garbage Out…

After the Brexit and the 2016 US Presidential Election, there seems to be a consensus that polls no longer work. Jennings and Wlezein (2018, JWN ) analyze 30,000 national opinion polls related to 351 general elections in 45 countries (including Brazil) between 1942 and 2017. The study reveals that reality is remarkably different from the current consensus narrative, the accuracy of polls did not worsen over time, but polls' performances can vary according to the political context.

Initially, the study correlates the absolute error between the actual results and the polls with the number of days to the Election Day, using the methodology introduced by Jennings and Wlezein (2016, JWE ). It is expected that polls converge to the actual result of the election over time. On the day of the election, the actual result should be within the poll's confidence interval. In fact, Jennings & Wlezein (2018) show that the average absolute error in the dataset they analyzed gets closer to 2% as the Election Day approaches (see graphics below).

I analyzed that data in a similar way as the theoretical reference just described for in the following events:

- 2010 Presidential election

- 2014 Presidential election

- 2016 São Paulo Municipal election

The broad results are on convergence are similar: the absolute error gradually decreases as the Election Day approaches. However, there is an important caveat: polls seem to present biased estimations for PSDB's Candidates. On three different occasions, the polls conducted 1 or 2 days prior to the Election Day had errors far superior to the 2% margin of error with 95% confidence.

It does not seem reasonable to suppose that this effect is due only to statistical variation. It also unlikely that 18.3% voters in São Paulo decided to vote for João Dória a day before the election. There are many other more reasonable explanations, including i) the samples used in the surveys are not diverse/representative enough to properly reflect PSDB's supporters; ii) the strategic behavior of the voter/tactical voting; iii) polls reflect only declared preferences and some parties'/candidates' supporters may decide not to reveal their preferences in polls, especially, in a polarized environment. Those possibilities assume that polling firms are not influenced by contractors or third parties, which may not be the case.

Market participants and the general public base their expectations on polls. The data unequivocally show that polls have been biased, therefore, the market participants' and the general public's expectations about the outcome of the election are greatly mistaken. Another relevant point is that convergence takes time, polls converged in probability to the actual results for other candidates but only 15 days prior to the election day.

Votes by Party

The total number of votes each party gets every election is roughly constant. Not surprisingly, the congressional renewal rate is very low in Brazil. For instance, it was only 43% in 2016, while in France, it reached 78%. The renewal rate in Brazil is probably even lower as it is not uncommon for a politician to be replaced by someone in his family or political group. Considering the total number of votes each party gets in the Congressional and Municipal elections, it is possible to see that changes in party's share of the electorate happen very slowly. Between two consecutive elections, the number is virtually constant (see chart below).

In the last three elections, the number of votes in parties that would be considered left-wing and center-left (PT, PSB, PDT, PCdoB, and PSOL) decreased (see graphic below). PT had a particularly poor performance in the 2016 Municipal Elections. There are no signs that this trend will significantly reverse in short term. PDT does not have a significant share of the electorate either at the municipal level or at the national level, and it seems unlikely that Ciro Gomes will have the structure to sustain his campaign and achieve a result much different to the party average.

Current Situation

In the coalition between Alckmin and the "center" is confirmed, Alckmin will have around 5 and a half minutes of each 12 and a half minutes block of TV and radio time reserved to political parties. Meanwhile, PT would have 1 minute and 35 seconds, Ciro Gomes would have 32 seconds, Bolsonaro would have 7 seconds, and Marina would have 11 seconds. This scenario may change if PSB decides to make a coalition with Ciro Gomes or with PT. In any case, the scenario will not change substantially, considering that Alckmin will have guaranteed support from the parties with the most of TV and radio time.

The parties of the "PSDB + Centrão" coalition have in total of 320 congressmen and had approximately 53 million votes in the 2014 Congressional Election. Considering the previous data, it is conceivable that Alckmin has at least the amount of votes necessary to go to the second round. Alckmin would have between 45 and 55 million votes in the first round based on the data from previous elections. I argued in the introduction that prediction markets are more efficient than polls to anticipate election results: Alckmin quote has increased on PredictIt recently (see chart below).

Market Impacts

The most important reason for the excess risk premium in Brazilian assets is the uncertainty about the reforms. If Alckmin wins, it should significantly reduce uncertainty about the implementation of major reforms and the fiscal consolidation. Alckmin has a pro-reforms/market-friendly agenda and is seen by 51% of people as able to approve economic reforms, more than any other candidate (see chart below). Considering, PSBD+Centrão coalition, Alckmin's election would probably mean the election of a constitutional majority in Congress. For the majority in the Congress to be reached, it is only necessary that the parties maintain the same performance they had in the previous elections, which seems to be a very reasonable hypothesis.

Liu (2017, YNL ) constructed a model for the risk premium required by the market given the fiscal uncertainty. In the model, there is an explicit mechanism transmitting the fiscal uncertainty to the risk premia in fixed income and equities. This model is particularly interesting because it allows calculating the price target for equities (IBOV/EWZ) based on a forecast of the budget deficit. Alckmin reinforced his plan to reduce the budget deficit to zero in the first two years of his term, which is a rather ambitious but achievable goal considering that Deficit/GDP is currently around 7.4%. Assuming that it is possible to implement measures that effectively eliminate the deficit by 2020, the IBOV's P/E should grow 45%, which would take valuations closer to its peers (see table below).

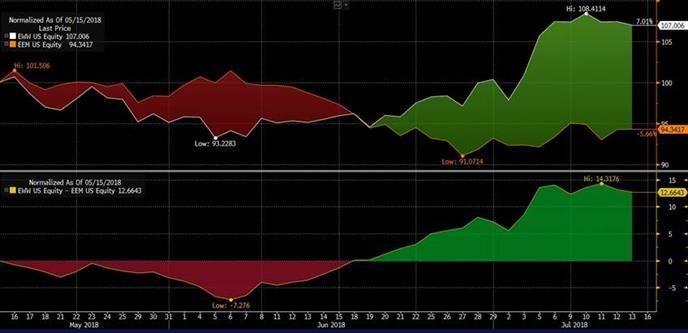

Since Trump's election and the Brexit referendum, markets have discounted any election risk. The Mexico election clearly shows that: even though AMLO won - which was probably the worst option in the market view - the EWW (Mexican ETF) outperformed its EM peers after the election on June 1st (see chart below). Even if a market-unfriendly candidate wins, depending on the stance he takes, it is possible that risk premium will decrease.

Given the current levels in valuations, I think the stock market is the most discounted asset. Therefore, EWZ is my preferred position to bet on the improvement of the electoral landscape. I expect equities to return 45% in BRL, the BRL to return 15%-20%, and the Brazilian CDS falling 150 points in case the scenario I described above materializes.

See also Superior Energy ( SPN ) Presents At Barclays CEO Energy-Power Conference - Slideshow on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}