It’s that time of the year again. Earnings season has officially kicked off, with a multitude of companies reporting quarterly results daily.

Investors are anxious to see how companies have fought back against skyrocketing inflation, supply chain disruptions, and increased labor costs. Needless to say, we’ve found ourselves in a highly unique economic situation.

One company slated to release its 2022 Q2 results next week on Tuesday before the opening bell is the widely-recognized United Parcel Service UPS. United Parcel Service is the world's largest express carrier and package delivery company.

In addition, UPS is currently a Zacks Rank #3 (Hold) with an overall VGM Score of an A.

We see them delivering packages all the time. Can they deliver in their quarterly report? Let’s take a closer look at how the company is standing heading into the earnings release.

Share Performance & Valuation

Year-to-date, UPS shares have struggled notably, declining more than 11% in value. However, shares have outperformed its Zacks Sector by a fair margin, undoubtedly a positive.

Image Source: Zacks Investment Research

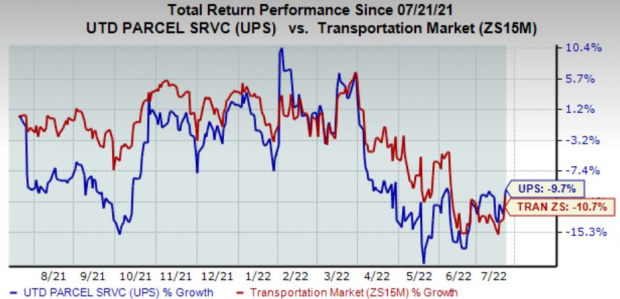

Upon widening the timeframe to encompass a year’s worth of price action, we can see that UPS shares traded sideways for some time from late 2021 to early 2022 but have overall declined nearly 10% in this timeframe.

Image Source: Zacks Investment Research

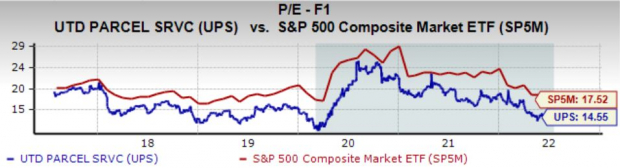

UPS shares could be considered undervalued, further displayed by its Style Score of a B for Value. The company’s forward earnings multiple resides at 14.6X, well below its five-year median of 16.4X and nowhere near highs of 25.6X in 2020.

In addition, shares trade at an enticing 17% premium relative to the S&P 500.

Image Source: Zacks Investment Research

Growth Estimates

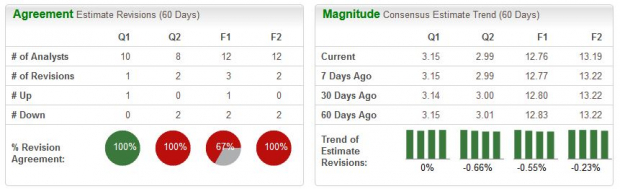

The Zacks Consensus EPS Estimate for the quarter to be reported resides at $3.15, reflecting a solid 3% uptick in quarterly earnings year-over-year. In addition, one analyst has upgraded their earnings outlook for the upcoming quarter.

Image Source: Zacks Investment Research

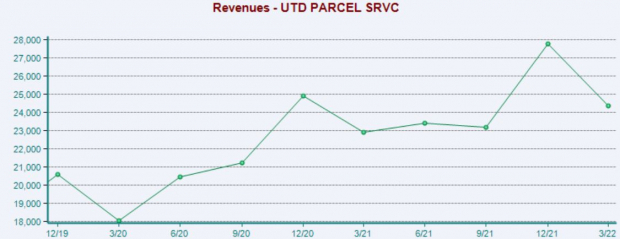

Top-line projections also display strength; UPS is forecasted to generate $24.8 billion in revenue for the quarter, a solid 5.7% uptick compared to year-ago quarterly sales of $23.4 billion.

Image Source: Zacks Investment Research

Quarterly Performance & Share Reactions

Recording bottom-line beats has been the norm for UPS – the company has impressively chained together eight consecutive EPS beats. In its latest quarter, UPS recorded a solid 6.3% bottom-line beat.

Quarterly revenue results have been stellar as well. Over the company’s previous ten quarterly reports, it’s posted nine top-line beats, all by at least 1.5%.

The market has generally reacted positively to EPS beats as of late, with shares increasing in value following four of the company’s previous six bottom-line beats.

Bottom Line

UPS looks to register single-digit revenue and earnings growth, undoubtedly a major positive amid a harsh macroeconomic backdrop.

In addition, quarterly results have been robust, and the company sports solid valuation levels. For these reasons, investors should feel optimistic heading into the quarterly report.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +24.8% per year. So be sure to give these hand-picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United Parcel Service, Inc. (UPS): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.