Credit: Shutterstock photo

Credit: Shutterstock photoBy Alerian :

By Karyl Patredis

What are the different types of MLP GP models?

On the heels of the Plains All American Pipeline ( PAA ) and Plains GP Holdings ( PAGP ) simplification announcement , we've received many questions about MLP GPs. Today I'll discuss the types of publicly traded GP structures in existence today and the significant considerations related to each.

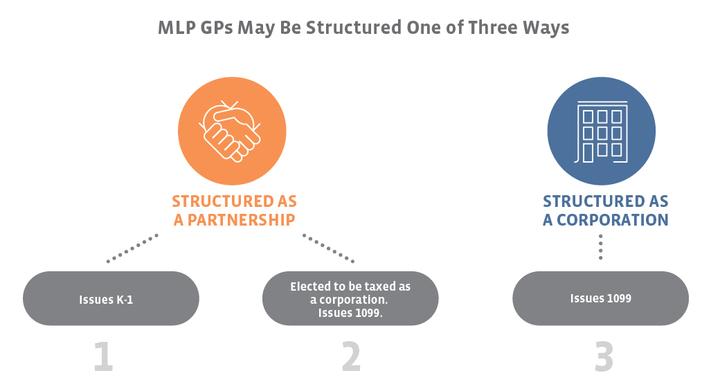

Currently [1], publicly traded MLP GPs fall into one of these three buckets:

- Formed and taxed as a partnership. Issues a K-1.

- Formed as a partnership but elects to be taxed as a corporation. Issues a 1099.

- Formed and taxed as a corporation. Issues a 1099.

For those of us that need a visual to understand things, our multimedia designer has it covered:

Buckets 1 and 2

Alliance Holdings GP ( AHGP ) [2], Energy Transfer Equity ( ETE ) [3], and Western Gas Equity Partners ( WGP ) [4] are a few [5] examples of the names in group one. EnLink Midstream (ENLC) [6], Plains GP Holdings ( PAGP ) [7], and Tallgrass Energy GP (TEGP) [8] fit into group two. From a technicality standpoint, Alerian considers the companies in groups one and two to be MLPs and they are included in the count for total number of MLPs.

Bucket 3

Group three requires a bit more explanation. To begin, some of these businesses were public corporations before forming an MLP while others were private MLP GPs that took their interests public into a C corp structure. Generally, the latter group goes public when the underlying MLP is approaching or has exceeded its highest (usually 50%) IDR split level. Examples of companies that were already public corporations before their MLPs were born are Spectra Energy Corp Corp (SE) [9] and TransCanada (TRP) [10]. The list of GPs of MLPs that were taken public as corporations after their MLPs already existed is, well, non-existent anymore. The corporations are still in operation, but the MLPs that made them relevant to this discussion are a thing of the past due to roll-up [11] transactions. For example, we have Kinder Morgan (KMI) who purchased its MLPs in 2014 leaving only a large corporation intact. Targa Resources (TRGP) would also have been in this group, but it acquired its MLP , Targa Resources Partners (former ticker: NGLS) earlier this year.

Why would a GP choose a certain bucket?

Clearly, if you're in bucket three, already a public corporation, and later decide to create an MLP, the structure is already in place. But if you're a private MLP GP and you're deciding whether to take the GP public as a partnership vs a corporation and the method of taxation, there are a few things to consider. First, there is the obvious K-1 or 1099 question. This may not seem like a big deal, but you'd be very surprised how many investors want K-1s about as badly as they want bed bugs. Capturing the right investor base may also be a consideration. If management teams are hoping to cast a wider net, forming as a corporation could make more sense as nearly all investors are familiar with 1099s. If management teams are looking to raise capital from dedicated energy investors, the MLP structure might be more appealing to those familiar with K-1s and who want to take advantage of the pass-through structure.

Tax implications for investors are also a concern. Some investors looking to own MLPs in a retirement account worry about UBIT . Owning corporations in tax-advantaged accounts may not spark the same concerns. The tax considerations of the companies themselves are paramount. For example, there could be some GPs whose full list of assets would not meet the qualifying income standards according to Section 7704 . For this reason, being taxed as a corporation might be logical. On the other hand, if the corporate structure is chosen, then the company is subject to income taxes. Some entities have enough deductions to avoid taxes for a handful of years, but it's still something to consider once those losses are exhausted. Finally, governance should also be considered. The partnership structure has looser governance requirements and may allow the general partner to retain the level of control that it desires after going public.

Anyone in the pipeline to become a public GP?

As I mentioned, when an underlying MLP is in or approaching the high splits, it could be a signal of a public GP on the horizon. American Midstream Partners (AMID) and TransMontaigne Partners (TLP) are both already in the high-split zone, but Arclight Capital Partners is the general partner of both. Since ArcLight is a private equity company, it's most likely they won't go public with GP interests. Martin Midstream Partners (MMLP) is also in the high splits [12] with a private GP. Martin Resource Management Company formed MMLP back in 2002. It's been six years since they hit the splits and since they didn't go public then, it's hard to imagine them going public now, especially since management just announced a strategic review to bring coverage up and leverage down, but we've learned never to say never [13].

Summit Midstream Partners (SMLP) is not quite in the 50/50 splits, but is getting close. SMLP's GP is Energy Capital Partners. A $0.5750 distribution was just declared and the 50% split level is $0.60. With only 4.3% more growth needed, there could be a case to take the GP public if Energy Capital Partners is looking to monetize its investment. However, with SMLP currently trading at levels similar to its IPO from September 2012, it might not be the best time.

Footnotes:

[1] Hedging myself here, because tax lawyers are notorious for coming up with new structures. Also, some would probably argue (and reasonably so) that the Up-C structure should be its own bucket, or at the very least, Bucket 2B.

[2] General partner of Alliance Resource Partners (ARLP).

[3] General partner of Sunoco (SUN) and Energy Transfer Partners (ETP). Also, ETP is technically the GP of Sunoco Logistics Partners (SXL), but ETE holds a 90.05% interest in the IDRs of SXL via Class H shares in ETP.

[4] General partner of Western Gas Partners (WES).

[5] Click the link on the word "examples" to download our Energy MLP Universe file which contains the full list under "Schedule K-1 Issuing GPs."

[6] General partner of EnLink Midstream Partners (ENLK).

[7] General partner of Plains All American ( PAA ).

[8] General partner of Tallgrass Energy Partners (TEP).

[9] SE was formed in late 2006. It's sweet little bundle of joy, Spectra Energy Partners (SEP) came along in mid-year 2007. SE is also a 50/50 joint venture owner (with Phillips 66 (PSX)) of DCP Midstream LLC, the general partner of DCP Midstream Partners (DPM).

[10] TRP was founded in 1951. It's MLP, TC Pipelines (TCP), held its IPO in 1999.

[11] A "roll-up" is a merger that results in the MLP being combined with the sponsor of the MLP. A "simplification" is an exchange, merger, contribution, or other transaction that results in elimination of the IDRs and the continued trading of the MLP's common equity.

[12] It's worth noting that AMID, TLP, and MMLP are all small cap MLPs, and an IPO of their general partner and IDR interests may not garner the same level of interest that other GP IPOs have over the past few years.

[13] #nevertrump

Disclosure: © Alerian 2016. All rights reserved. This material is reproduced with the prior consent of Alerian. It is provided as general information only and should not be taken as investment advice. Employees of Alerian are prohibited from owning individual MLPs. For more information on Alerian and to see our full disclaimer, visit http://www.alerian.com/disclaimers.

Karyl Patredis is the Logistics Coordinator at Alerian, which equips investors to make informed decisions about Master Limited Partnerships (MLPs) and energy infrastructure. Ms. Patredis leads the firm's ongoing efforts toward greater organizational efficiency. She also oversees Alerian's feedback process for creative output. Ms. Patredis graduated with a Master of Science in Accounting and a Master of Business Administration from the University of Dallas, as well as a Bachelor of Arts in Communication and a minor in Psychology from Texas A&M University.

See also Why Kinder Morgan Is Still A Screaming Buy, BUT Only If You Can Stand The High Risks on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}