Trump's Trade Tweet Moves Markets Higher

- NASDAQ Composite +0.95% Dow +1.01% S&P 500 +0.98% Russell 2000 +1.05%

- NASDAQ Advancers: 1795 Decliners: 695

- Today’s Volume (vs Wednesday) +44%

- Crude $59.40 +$0.65, Gold $1468.00 -$1.40, VIX 14.00 -0.77

Market Movers

- Markets higher after Trump tweets “VERY close to a BIG DEAL with China”

- U.K. general elections today

- ECB left policy unchanged

- U.S. November PPI flat vs. +0.2% consensus

- November ex-Food & Energy -0.2% vs. +0.2% consensus

- PPI Y/o/Y increased 1.1% vs +1.3% consensus

- U.S. Initial Weekly Jobless Claims reported at 252,000 vs. consensus 214,000

- U.S. Continuing Jobless Claims reported at 1.667 million below consensus of 1.678 million

- Reaction to earnings: CIEN +12%, OXM +2%, LULU -5%, LOVE -10%

Chris’ Commentary

Yesterday, as expected, the FOMC voted unanimously to leave the target range for the fed funds rate at 1.50-1.75%. The markets reacted positively to the news and rallied into the close. The S&P 500 closed up 0.29%, the Dow up 0.11%, the Nasdaq was higher by 0.44% and the Russell 2000 finished slightly positive. More importantly, yesterday’s positive reaction for stocks can be attributed to the median projection for the policy rate in 2020 signaling no change. Fed Chair Powell in his press conference afterwards reiterated he would need to see a persistent and significant rise in inflation to hike rates. Despite the positive reaction, trading volumes on the consolidated tape continue to lag below the yearly average.

Today we opened higher after President Trump tweeted that the U.S. is "VERY" close to a "BIG DEAL" with China. All the major indexes are up about 1% in a risk-on environment. Risk of a Phase One trade deal not being done has been the albatross around the markets neck. Any inkling of a deal being announced before this Sunday’s tariff deadline should be viewed as a positive for traders.

Currently, nine of the 11 of the S&P 500 sectors are trading higher with Energy and Financials significantly outperforming. As a matter-of-fact, 7 of the 11 GICS sectors are up over 1%. Real Estate is the main laggard down over 0.5%. Crude trades higher following the dovish Fed comments. Gold is lower. The dollar is higher while the yield on the 10-yr stands at 1.88% as traders sell bonds to buy stocks.

The Producer Price Index (PPI) measures price change from the perspective of the seller. November’s numbers were weaker than analysts’ expectation as were the year-over-year comps. PPI final demand was flat in November verse +0.4% in October. November consensus was for 0.3% growth. Ex-food and energy declined by 0.2% (consensus +0.2%). The year-over-year change for these measures came in at +1.1% and +1.3% respectively. This report shows signs of disinflation and low inflation expectations which ties into the FED narrative to keep rates unchanged into next year.

Unemployment numbers released by the U.S. Department of Labor reported the largest increase of new claims in nearly 2 years. Though still running near record lows, the number of new applications was higher than most economists thought. Reported Initial Jobless Claims rose to 252,000 vs 214,000 consensus. Reported Continuing Claims were below estimates at 1.667 million claims. Continuing and initial claims were both revised slightly higher. Continuing claims were revised slightly higher last week to 1.693 million from 1.689 million.

Sector Recap

Brian’s Technical Take

There is a new sheriff in town. Today is Christine Lagarde’s first monetary policy meeting as ECB President and local banks appear to like what she is saying. In the press conference, Lagarde said the central bank’s new policy review will start in January. She also believes downside risks are becoming less pronounced and the two year economic slowdown is showing signs of bottoming. The market read is Lagarde’s comments indicate further rate cuts are unlikely in the near term which is welcome news to the rate sensitive financials.

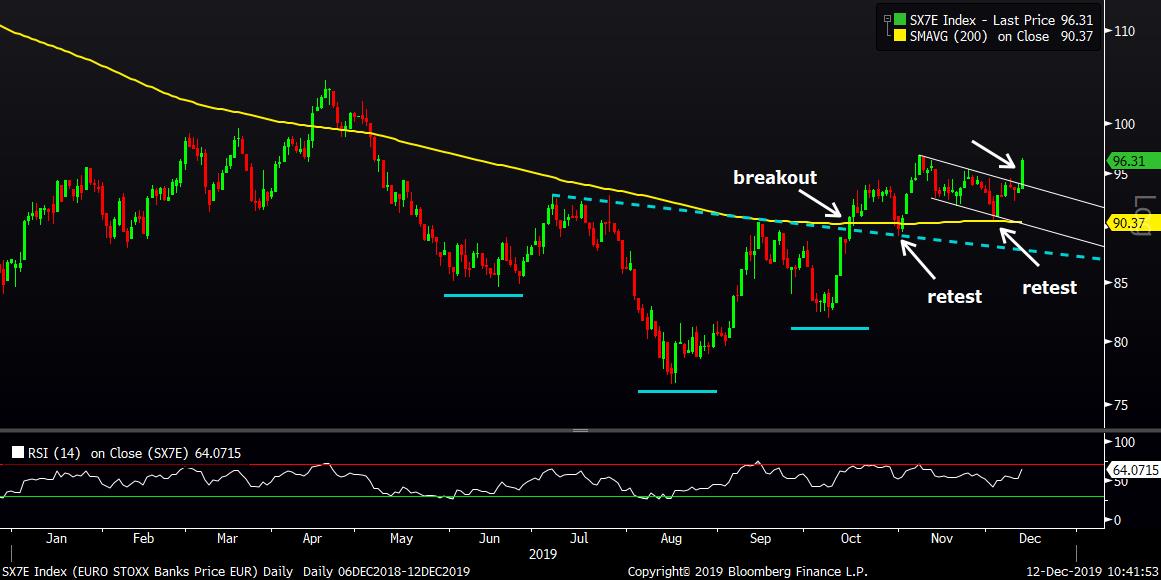

The Euro Stoxx Bank Index (ticker SX7E) is +3.2% in today’s session. The large cap bank index bottomed in August at a clearly defined, SECULAR support level (chart 1, monthly period) which we previously identified back in the August 15th and September 23rd MIDDAY Updates. It now stands +25% from those August lows.

The now four month uptrend in the SX7E Index made a “bullish breakout” above the neckline of a common bottoming pattern (IHS) in mid-October, as seen in the daily period, chart 2. The neckline coincided with the 200-day simple moving average, a common support/resistance line. Two weeks later in late October it retested this prior resistance, common technical price action, which successfully held as support. Just last week it again retested its 200-day sma, and again it held support. Today’s gains are now “breaking out” of a four week declining price channel and thus resuming the prior four month uptrend.

With a new ECB president, market participants may be looking long term with expectations that the era of increasingly negative rate cuts may finally be a thing of the past. The new sheriff and her deputies are exploring fresh ideas to add to their monetary policy toolkit, as is the U.S. Federal Reserve. Likely to the dismay of the Austrian school economists, central bankers could directly or indirectly pressure local governments to step up and carry some of the stimulus burden through fiscal measures.

The fruits of such potential monetary and fiscal policy action are unlikely to be reflected in bank’s bottom line over the near to intermediate term, let’s call it quarters, however expectations and thus price action often lead fundamentals.

While the SX7E index is already +25% from its August lows, it is has another 48% to go just to reach its 2018 highs. For context it will take 150% to reach its 2009 highs, and more than 400% to get to its 2007 highs. Oh by the way its monthly MACD (12,26), lower panel of chart 1, just last month made a bullish cross above its signal line (9).

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen-based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen-based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq, Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio