Toll Brothers, Inc. TOL is scheduled to report fourth-quarter fiscal 2024 (ended Oct. 31) results on Dec. 9, after the closing bell.

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

In the last reported quarter, Toll Brothers reported earnings per share (EPS) of $3.60 (down 3.5% from a year ago), which beat the Zacks Consensus Estimate by 9.8%, and total revenues of $2.73 billion (up 1.5% year-over-year) topped the consensus estimate by 1.2%. The company delivered 2,814 homes at an average price of $968,000, generating record fiscal third-quarter home sale revenues of $2.72 billion. Adjusted gross margin was 28.8%, exceeding guidance by 110 basis points due to greater efficiencies in homebuilding operations and a favorable mix.

During theearnings call this luxury homebuilder raised its full-year delivery guidance and now expects to deliver between 10,650 and 10,750 homes, with a projected homebuilding revenue between $10.4 billion and $10.5 billion.

Toll Brothers has an impressive track record of surpassing earnings expectations, exceeding the consensus mark in three of the last four quarters and missed on one occasion. The average surprise over this period is 7.8%, as shown in the chart below.

Image Source: Zacks Investment Research

How Are Estimates Placed for TOL?

The Zacks Consensus Estimate for the fiscal fourth-quarter EPS has increased to $4.31 from $4.30 over the past 60 days. The estimated figure indicates 4.9% growth from the year-ago reported figure. The consensus mark for revenues is $3.16 billion, indicating 4.6% year-over-year growth.

Image Source: Zacks Investment Research

What the Zacks Model Unveils for Toll Brothers

Our proven model does not predict an earnings beat for Toll Brothers for the quarter to be reported. That is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) for this to happen. This is not the case here, as you will see below.

Earnings ESP: TOL has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Influencing Toll Brothers’ Q4 Performance

Toll Brothers’ fiscal fourth-quarter home sales are expected to have increased from the year-ago reported level, given higher deliveries. Although higher mortgage rates will impact the volumes to some extent, Toll Brothers has been capitalizing on operational efficiencies, robust demand across multiple regions, and an expanding inventory of speculative homes. The company is strategically positioned to leverage long-term demographic trends and address the persistent housing supply shortage.

This apart, its focus on luxury move-up buyers, who already possess a residence and are looking to shift to larger and better homes, will somewhat contribute to revenues. The company has also been benefiting from the strategy of broadening its product lines, price points and geographies, along with spec sales.

On the fiscal third-quarterearnings call TOL stated that it expects higher home deliveries within 3,275-3,375 units in the fiscal fourth quarter, up from 2,755 units delivered in the prior-year quarter at an average price of $940,000-$950,000 (suggesting a decline from $1,071,500 a year ago).

Higher land, labor and raw material costs, along with high incentives, are expected to put pressure on the fiscal fourth-quarter margins. Toll Brothers expects the adjusted home sales gross margin to be 27.5%, implying a decrease from 29.1% reported in the year-ago period. SG&A expenses are estimated to be 8.6% of home sales revenues, indicating a rise from 8.2% reported in the year-ago period. The company expects the effective tax rate to be approximately 26%.

Our Estimates

Our model predicts home sales revenues to grow 6.1% year over year to $3.13 billion due to 20.5% higher deliveries of 3,321 units in the quarter. We expect ASP to be down 12% year over year to $943,100.

We expect net signed contracts to be around 2,693 units, indicating an improvement of 32.2% from the prior-year reported figure.

Our model predicts a backlog of 6,141 units, indicating a decline of 6.6% from the year-ago period. The same for the backlog (in values) is pegged at $6.52 billion, implying a decline of 6.1% from the $6.95 million recorded at fiscal 2023-end.

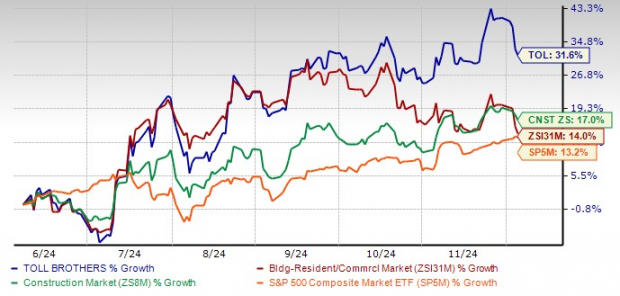

TOL Stock’s Price Performance & Valuation

Toll Brothers stock has exhibited an upward movement in the past six-month period and outperformed the Zacks Building Products - Home Builders industry.

TOL’s 6-Month Price Performance

Image Source: Zacks Investment Research

Let’s evaluate the value TOL provides to investors at its current price levels.

Currently, TOL is trading at a level roughly aligned with the industry average, as illustrated in the chart below. Despite the stock’s outperformance, TOL’s current valuation is still reasonably valued. It is also trading at a discount compared with big industry players like D.R. Horton, Inc. DHI, Lennar Corporation LEN and NVR, inc. NVR. DHI, LEN and NVR are trading with forward 12-month P/E multiples of 11.01, 11.61, and 16.94, respectively. Presently, TOL holds a Value Score of B.

Image Source: Zacks Investment Research

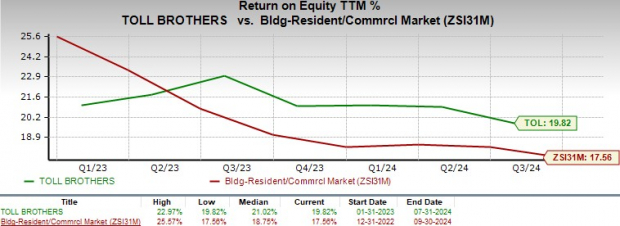

Again, TOL’s trailing 12-month return on equity is better than its industry average, as shown in the chart below.

Image Source: Zacks Investment Research

Investment Thoughts: Buy, Sell or Hold TOL Stock?

Toll Brothers presents a strong investment case despite challenges in the homebuilding industry. The Federal Reserve's recent rate cuts and the resulting drop in mortgage rates, now at 6.69% (for the week ended Dec. 5) compared with 6.81% last week and 7.03% a year ago, have significantly boosted homebuying demand. Favorable demographics, a robust customer base, and positive earnings revisions further support the company’s growth potential. Additionally, Toll Brothers’ attractive valuation and stock outperformance make it an appealing choice for investors seeking exposure to the homebuilding sector.

However, challenges like rising labor and material costs and a higher proportion of spec homes in its portfolio have pressured margins. Spec homes, while providing faster sales, yield lower profitability compared to built-to-order homes. The company's use of incentives, such as rate buydowns, to stimulate sales has also weighed on gross margins.

Despite these obstacles, Toll Brothers' strong fundamentals and ability to adapt to market conditions make it a worthwhile investment. For investors looking to capitalize on favorable housing market dynamics, TOL offers a promising balance of opportunity and resilience. Current stakeholders are advised to maintain their position in this stock.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpToll Brothers Inc. (TOL) : Free Stock Analysis Report

Lennar Corporation (LEN) : Free Stock Analysis Report

D.R. Horton, Inc. (DHI) : Free Stock Analysis Report

NVR, Inc. (NVR) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.