Stocks Slide After ECB Signals Rate Cut

Market Movers

- ECB gave dovish signals but Draghi's commentary fueled concern about outlook.

- Earnings results weighed on stocks today.

- Durable Goods Orders rose 2.0% vs. 0.7% expected.

- Initial Jobless Claims of 206,000 were below the 218,000 expectation, reflecting a still-strong jobs market.

Mike’s Commentary

Markets are taking their cues from The ECB today. Even though the ECB committed to looking at further interest rate cuts and more quantitative easing, ECB President Mario Draghi said in his comments that the economy is getting “worse and worse,” which ended up hurting stocks in Europe and the U.S.

Mr. Draghi actually said, “This outlook is getting worse and worse. It’s getting worse and worse in manufacturing, especially, and it’s getting worse and worse in those countries where manufacturing is very important.” That does not exactly inspire confidence.

At first, stocks moved higher pre-open on the (expected) dovish commentary, but then gave back gains on discussion that the stimulus should have been even more given the increased possibility of a recession. So, a bad economy is good if the rate cuts help stock prices but that only goes so far. If an economy is really bad, then rate cuts will not be enough to stave off the earnings decreases.

In earnings news, 3M, Ford, Tesla, Dow, and PayPal were amongst the reporters with results to digest this morning. All five were trading lower, which of course contributes to the weakness in stocks this morning. Tonight we’ll look for Amazon and , among many others.

Still, even with the ECB news and the earnings drag, stocks are down “only” about 0.5% or 125 Dow points - not too far from recent records.

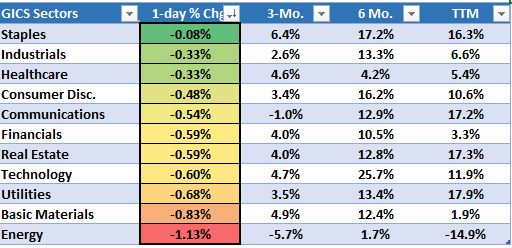

Each sector is lower today, with Energy and Materials the worst performers and Staples and Healthcare among the “least worst.”

In economic news, Durable Goods Orders rose 2.0% vs the 0.7% forecast after declines in three of the past four months. It seems the factory sector in the U.S. is doing better than much of the rest of the world. Let’s hope these orders flow into actual manufacturing production in future months. The employment picture was also good, with initial jobless claims falling 10,000 to 206,000 from vs. 218,000 and 216,000 last week.

Sector Recap

Brian’s Technical Take

The ECB did not take any action today but strongly signaled it can cut rates deeper and potentially restart buying bonds if needed. Draghi specifically noted the economic outlook is “getting worse and worse” and highlighted concerns about manufacturing activity and falling inflation.

The EURUSD currency pair made a new 52-week low before rebounding towards the midpoint of this week’s range. Today marks the 4th time the 1.112 level has been tested since late April thus making it a critical support level.

The ball is now in the Fed’s court. Next week’s FOMC is widely expected to be the start of the first rate cut cycle since the early days of the housing crisis. The 25bps rate cut is all but a given. The focus will be whether the committee starts this cycle with a 50bps cut like the prior two cycles, and any clues as to the expected magnitude of cuts into year end 2020.

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Stocks Earnings Central Banks

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.