Stocks Rally After Jobs Report

Market Movers

- Nonfarm Payrolls rose 136,000, below the 145,000 estimate.

- Private Payrolls rose 130,000, also below estimates (114,000)

- Average hourly earnings rose 2.9% against a 3.2% estimate

- The Unemployment rate, however, fall to 3.5% from 3.7%, the lowest since 1969.

- August Nonfarm payrolls were revised upward by 38,000 to 168,000.

- Stocks reacted positively to the Jobs report and to later comments about a China trade deal from President Trump

Mike’s Commentary

Today the market is solidly in positive territory after a “Goldilocks” Payrolls number that was strong enough to provide comfort about consumer spending (and assuage some fears of recent ISM numbers) but weak enough to keep a Fed rate cut on the table.

Yesterday the attention was on the ISM Services number as a confirmation of manufacturing weakness. The disappointing release cause an immediate 200+point drop in the Dow and brought the three-day loss to almost 1,100 points. Then a funny thing happened. The market rallied back to unchanged. People were scratching their heads. I sure was. With no fundamental or trade headlines to drive stocks higher we started to think of short covering as investors locked in gains or maybe just that oversold conditions let to a buying spree. Another possibility was the 2% yield on the S&P 500 was now attractive. All of these made sense but the most likely culprit was the well-known “Fed Put”. Sure enough, a check of Fed Fund Futures yesterday showed a 93% chance of a rate cut at the end of this month, double the 49% chance of only a week ago. Today the odds are 80%. The return to “bad news is good” seemed to best explain the market dynamic yesterday amid the drumbeat of weaker economic indicators here and abroad.

For confirmation of this, we look to jobs numbers this morning. Private payrolls missed an already low estimate of 130,000 job gains, with hiring only at 114,000 in September. Nonfarm payrolls rose 136,000, below the 144,000 estimate. The market reaction? Up. Futures rose and bonds fell on the release, which seems to suggest investors are now expecting the Fed to act on the recent data and cut rates by 25bp to a target range of 1.50%-1.75%.

The jobs report also had some bright spots including a 2.9% increase in hourly earnings even though this was below the 3.2% estimate, and a 50 year low for the unemployment rate to 3.5% from 3.7%. August payrolls were also revised higher by 38,000 jobs to 168,000. The release seems to have something for everyone since one can argue it’s strong enough to indicate we’re not at risk of an imminent recession since consumers still have spending power but weak enough to allow for more Fed rate cuts.

Does a further 25bp cut allow for business & consumers to borrow more cheaply and stimulate the economy? Maybe. Will it help rein in a stronger dollar and help exporters? Maybe. But either way the market likes rate cuts and stocks rose over 200 points by mid-morning and currently up about 235 in choppy trading. News that White House economic adviser Larry Kudlow said there could be “positive surprises” coming out of the trade talks between the U.S. and China next week in Washington also helped stocks. They gained further when President Trump hinted at the same. With two 1% declines totaling 837 points this week, I’m sure the bulls would settle for some modest gains yesterday and today and a weekend to regroup.

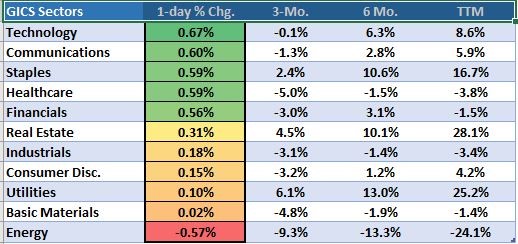

Risk is back in fashion today as the Technology and Healthcare sectors are leading the charge higher and only Energy stocks moving lower. Oil is up but some of the E&P companies are trading down.

Sector Recap

Brian’s Technical Take

Equities are responding favorably to the monthly payroll figures but not so much for the bond market. While rates are a smidge higher on the short end, yields from the 5YR maturity and out are down 1-2bps.

Markets are still pricing close to an 80% probability the Fed will cut the overnight rate later this month for the third consecutive FOMC. This has been the base case for months and makes sense with the overnight rate still one of the highest along the curve and compared to many global yields. In addition the Fed will have to instill a more permanent solution for the illiquidity in the short term money markets.

The weak ISM manufacturing and services data released earlier this week has increased the likelihood that Powell’s mid-cycle adjustment forecast, widely interpreted as three cuts a la Greenspan in the 90’s, is not going to be enough. As of yesterday markets were pricing in a 58% probability for a fourth rate cut by year end, the highest odds this year. While equity investors usually do not do well when fighting the Fed, the bond market often makes a living from it.

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen-based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen-based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq, Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Stocks

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio