Stocks Pause Near Record Highs

Market Movers

REMINDER: Today is MSCI Semi Annual rebalance. You might see block trades at the close

- Advance Goods Trade Balance, -$66.5 B vs. -$71B est.

- Retail Inventories MoM 0.3% vs 0.1% est.

- October Wholesale Inventories in line at 0.2%

- Richmond Fed Manufacturing Index was -1 vs. 5 est.

- October New Home Sales better than expected 733,000 vs. 705,000 est. capping the best two months in 12 years according to Bloomberg.

- Consumer confidence fell to 125.5 from 126.1

Mike’s Commentary

Please note today is the MSCI Semi-Annual Index Review, which might mean larger than normal block activity at the close as firms rebalance various funds benchmarked to MSCI indices.

Stocks again hit record highs yesterday with the Dow reclaiming the 28,000 level and the S&P 500 and Nasdaq 100 indexes also closing at new highs. The three indexes are now up 20%, 25% and 32% year-to-date. The incremental news yesterday was that China had over the weekend indicated it would tighten intellectual property rules, which raised hopes that the U.S.-China trade deal. Helping was also news of a few large mergers and, frankly the fact that momentum has been positive. The Fed's expanding balance sheet is also offering a big assist.

Today, none of those themes have changed. With a slow week and essentially a four-day weekend expected, nobody wants to be a hero and get too long or short. We did have a few of economic releases this morning. The trade deficit fell in part due to lower imports from China, which may not be a good thing if economic activity is slowing. Imports fell to a two-year low of 202 billion so the deficit of $66.5 billion was lower than the $71 billion expected. Wholesale and Retail inventories rose 0.2% and 0.3% respectively. Rising inventories can be interpreted positively if merchants are stocking ahead of planned sales growth or negatively if goods are piling up on shelves. I'm honestly not sure which this is.

Consumer confidence fell for the fourth straight month to a still-not-terrible 125.5 from an (upwardly revised) figure of 126.1 reading last month and an estimate of 127. Job gains have been moderating slightly. Economists watch confidence closely since consumer spending is so important to the economy. Expectations for 2020 growth of about 2% remain intact.

Stocks today yawned at this economic date, pausing near highs but inching upward as trade rhetoric is de-escalating and the path of least resistance is up. We are getting to the point where the "good" trade news is priced in and the market will be looking for details.

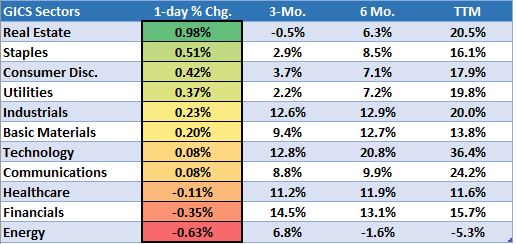

With stocks hovering around unchanged there is no overall theme to sector performance today. Real Estate is leading along with Staples and Discretionary. Energy is the worst performing sector, down about 0.6% as oil is up slightly to $58.32.

Sector Recap

Brian’s Technical Take

Yesterday there was a lot of buzz across the media channels regarding small cap stocks and rightly so. The Russell 2000 gained 2.1% for its best one-day gain in ten weeks. A minor achievement in and of itself, but more importantly the small cap index made its “breakout” above a nine month resistance line at the ~1,600 level. In general, breakouts from large ranges can signal a transition from consolidation to tend, and can often be accompanied by powerful momentum.

Just one week ago (11/19 MIDDAY Update) we wrote “now could be the time for small caps” and noted the recent change in character for the Russell 2000 given its tight consolidation, over two weeks’ time, along clearly defined resistance. This was in contrast to the prior three occurrences in May, August, and September when price failed at this same level and quickly reversed lower with declines of ~8%.

Another tell was the positive breadth readings where an increasing number of members were making fresh six and twelve month highs. In early November, 14% of its members reached six month highs (lower panel), the highest percentage since June of 2018.

Momentum is strong with the daily and weekly RSI’s now at 68 and 61. In early November the daily RSI reached new 52-week highs. Now the weekly RSI is itself breaking out to 14 months highs which reflects accelerating upside momentum. Both breadth and momentum can often lead price, case in point.

As always price is king and the small cap index needs to prove it can hold the breakout, unlike what happened in May when two day move to new highs quickly fizzled out and price reversed sharply lower. This time around the little guys have both breadth and momentum on their side. The minimum price projection based on the size of the prior 9-month range targets the 2018 high, +8% from yesterday’s close.

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen-based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen-based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq, Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Stocks

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio