Stocks Little Changed Ahead of Tariff Deadline

- NASDAQ Composite -0.02% Dow -0.09% S&P 500 +0.03% Russell 2000 +0.19%

- NASDAQ Advancers: 1285 Decliners: 1073

- Today’s Volume (100 day avg) -8.6%

- Crude $58.67 +$0.24, Gold $1476.400 +$2.40, VIX 14.62 -0.19

Market Movers

- U.S. Initial Weekly Jobless Claims reported at 203,000 vs. consensus 215,000

- U.S. Continuing Jobless Claims reported at 1.693 million vs. consensus of 1.66 million

- October U.S. Factory Orders +0.3%, in-line with consensus

- October Trade Balance deficit of -$47.2 billion vs consensus -$48.5 billion

- September deficit revised better to -$51.1 billion from -$52.5 billion

- Reaction to earnings: DLTH +25%, SPWH +15%, PDCO +11, SIG +10%, RH + 10%, FIVE +6%, DG + 2%, HOME -35%, SNPS -2%, KR -3%, WORK -3.5%, MIK-6.3%

Chris’ Commentary

Stocks are trading mixed to flat as trade headlines (or lack thereof) are in focus. It was really a directionless open as we started in the green but slid into the red by late morning. Economic data today is neutral to slightly positive with unemployment numbers still a bright spot for the economy.

The S&P 500 rebounded yesterday closing up +0.63%, following Tuesday’s 1% sell-off. The market reacted positively to a Bloomberg report that suggested a trade deal with China is closer to be signed than the headline rhetoric we are accustom to seeing on the boob-tube. All the other major indexes finished higher by about 0.5%.

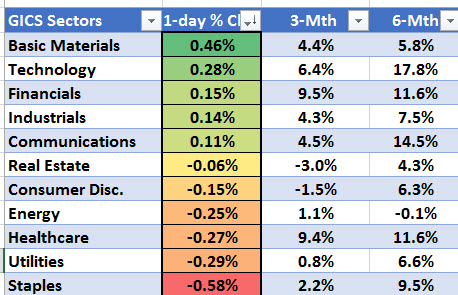

Currently, 5 of the 11 of the S&P 500 sectors are trading higher with Materials and Tech leading. Staples, Utilities and Health Care are the laggards. Crude oil is higher for the 4th day in a row, up 1% today and up nearly 7% for the week. Gold trades higher while the dollar is lower. The yield on the 10-yr stands at 1.81%.

Unemployment numbers released by the U.S. Department of Labor unexpectedly fell to a seven-month low. Reported Initial Jobless Claims were at 203,000 beating consensus of 215,000 new claims. Reported Continuing Claims were also a little worse at 1.693 million claims vs 1.66 million consensus. With yesterday’s ADP Employment number saying only added 67,000 jobs in November which is below half of what was expected, the numbers seem at odds. Tomorrow the Labor Department will report non-farm payrolls with the expectation of 184,000 new jobs added.

Oil prices continue to be a focus as OPEC meets in Vienna today. Expectations are for the cartel members and their allies (including Russia) to announce more outputs cuts. Crude is up 7% this week in expectation of another reduction announcement.

Holiday sales appear solid thus far pointing to a healthy consumer. Thanksgiving weekend drew nearly 190 million shoppers looking for deals. NRF President and CEO Matthew Shay said, “Whether they’re looking for something unique on Main Street, making a trip to the mall or clicking from the couch, this is when holiday shoppers shift into high gear." Online sales continue to gain share while brick and mortar traffic continues to decline. Adobe Analytics reported a 20% increase in e-commerce sales growth on Black Friday and Cyber Monday. Adobe reported $24.4 billion in internet sales for the four largest shopping days which was $0.2 billion less than expected.

Sector Recap

Brian’s Technical Take

So much of the headlines these days have been focused on the ongoing and emerging trade wars, which many of us point to as the reason(s) behind the one day moves in the markets. I often do not have the time to keep up with the wide range of reports these days, but I wonder if enough focus has been made about the recent monetary policy proposals getting around.

Last week Fed Governor Brainard spoke on inflation and employment and in it laid out a series of ideas outside of the Fed’s existing toolkit. In it she spoke about rate caps, curve targeting, and having an 12-month average inflation target vs. the existing 2% figure. Then just three days ago the FT ran an article saying the Fed may look to overshoot its 2% inflation target, which we briefly highlighted in our “November Review and Outlook” note. If there is credibility to these ideas, it seems the Federal Reserve’s dovish pivot from January 2019 could potentially evolve into “whatever it takes” mode that would be different from the negative rates strategy implemented by global central banks following the 2008 Financial Crisis. It remains to be seen how this unfolds, but maybe the December 11th FOMC will shed more light on this.

Markets generally anticipate what is coming down the pipeline so it is somewhat interesting to see the US Dollar Index (DXY) in the red for the fifth consecutive session, while today falling below its 200-day moving average. Not a major move at this time but it’s now on the radar.

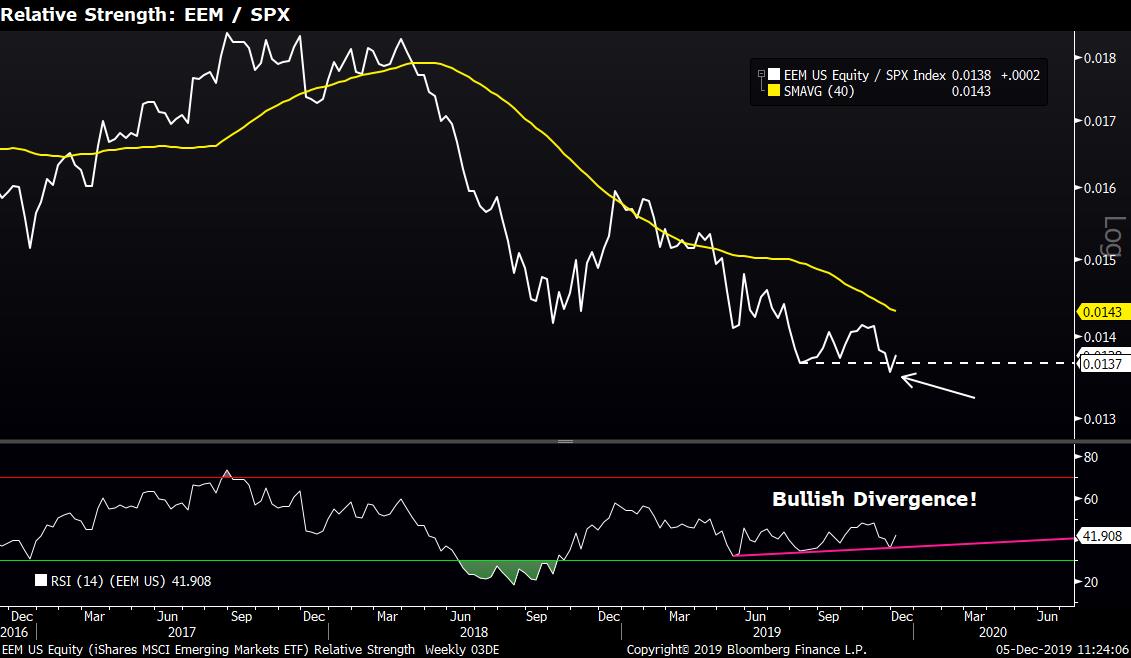

Accordingly there is some interesting price action this week in the emerging markets ETF (EEM). The EEM rebound 14% from its August lows to November highs before then giving back a modest 5% at this week’s lows. Now its second day in the green has it back above its 410-week moving average, an expected support level, and is currently sporting a common bottoming pattern (hammer candlestick) on the weekly time frame.

The week is not yet over and so we don’t want to jump the gun, but I wonder if the uptrend from the August lows has now resumed. The relative strength chart plotting the ratio of EEM over SPX leaves much to be desired from a technical perspective. Just last week the EEM / SPX ratio made a new 16 year low, however it was accompanied by a bullish divergence whereby the weekly RSI has been making a series of higher lows since May of 2019.

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen-based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen-based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq, Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Stocks

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio