Stocks Higher on Trade Optimism

- NASDAQ Composite +0.70% Dow +0.30% S&P 500 +0.33% Russell 2000 +1.03%

- NASDAQ Advancers: 1610 / Decliners: 730

- Today's Volume (vs. Tuesday) -16.01%

- Crude -0.64%, Gold +0.24%

Market Movers

- MBA Mortgage Applications for the period ending 9/6 came in at 2.0% vs. prior -3.1%

- August US PPI +0.1% vs. consensus +0.1%; August ex-Food & Energy +0.3% vs. consensus +0.2%.

- Wholesale Inventories climb 0.2% in July, in line with consensus while sales were flat

- DOE reports crude oil inventories (6.91M) barrels vs consensus (2.9M) barrels

- Hong Kong Exchange makes $36.6 billion bid for the London Stock Exchange

Charlie’s Commentary

Equities finished in mixed territory yesterday staging a late day rally erasing earlier losses. A lot of the late day buying was in the under-owned value/cyclical stocks. Much has been made lately of the recent rotation in the market. Value is Vogue at the moment with previously favored momentum stocks left on the sideline. Perhaps no better example of this was in the performance of two ETF’s. Bespoke Investments noted that on Monday the MSCI USA Value Factor ETF (VLUE) rose 1.8% on Monday and continued to climb by 1.4% yesterday. In contrast the MSCI USA Momentum Factor ETF (MTUM) fell 1.7% on Monday and continued to fall 1.5% yesterday. Monday’s divergence between the value and momentum ETF was the largest since its inception on 2013. The shift in investor sentiment is front and center as growth stocks have outperformed the S&P 500 over the past five years. The MTUM ETF is up more than 130% during that five year period while the more conservative VLUE ETF has gained 70%. Will this trend continue? We shall see.

Stocks have come out of the gate in cautious territory this morning following modest gains in Europe and Asia. Trade remains an underlying theme for the market as China released a tariff exception list on certain US products earlier this morning. Despite that conciliatory gesture US companies remain skeptical of any near term resolution and continue to make contingency plans away from China as a result. Investors remain cautiously optimistic in the market awaiting several policy announcements later this week and next. Specifically the ECB will be meeting this Thursday, widely expected to cut interest rates while reviewing all options that will include quantitative easing. Next week both the Federal Reserve and the Bank of England will be meeting to discuss monetary policy. Domestically, market expectations for a September rate cut are at 91.2%, according to the CME Group’s FedWatch tool.

On the economic front US producer prices rose in August. The Labor Department reported that producer price index rose by 0.1% last month due to a rise in the cost of services that offset a drop in the price of goods that was the largest in seven months. In the twelve months since August, the producer price index has risen 1.8% after increasing 1.7% in July. Core producer prices that strips out volatile food and fuel increased 2.3% in August from a year earlier which topped consensus estimates. The Fed tracks core personal consumption expenditures as it reviews monetary policy. The core PCE price index increased 1.6% on a year over year basis in July. The U.S. central bank is largely expected to lower rates in a meeting next week.

According to the Mortgage Bankers Association, total application volume rose by 2% last week compared to the prior week. Volume was up 69% compared the same week last year when interest rates were much higher. It appears that low rates, more moderate home prices and anxious sellers are bringing buyers back to the market.

According to the Commerce Department, wholesale inventories for the month of July rose 0.2% rising from a small decline the prior month. An increase in inventories adds to gross domestic product. The ratio of inventories to sales (how many months it would take to sell all the inventory on hand) was unchanged at 1.36%.

Turning to the commodity space, oil is falling despite a reported sharp drop in U.S. crude stocks. The Department of Energy recently reported a draw of 6.91 million barrels vs. the consensus 2.9 million barrels. Data recently from the American Petroleum Institute showed U.S. crude stocks fell last week by 7.2 million barrels, more than twice the amount analysts had forecast. Iraq’s oil minister said that OPEC exporting countries would discuss deepening cuts when they meet on Thursday. He said OPEC had discussed cuts of 1.6 million to 1.8 million bpd, when considering output curbs last year. Gold prices are creeping up today after being down for four consecutive days as investors buy the dip ahead of expectations that the European Central Bank will cut rates and provide stimulus.

Turning to sector performance, Energy lead currently up by +0.94% followed by Communications (+0.53 ) and Technology (+0.47). Lagging are Real Estate (-0.48), Financials (-0.06) and Consumer Discretionary (0.01).

Sector Recap

Brian’s Technical Take

The reflation trade is permeating throughout the markets so far in the month of September. In the rates complex the long end of the curve has moved sharply higher with the 10YR UST yield +30bps to 1.73% from just last week’s low, 1.43%. The bear steepening in the yield curve has lifted the 10YR-2YR spread from –5bps two weeks ago to +7bps today. 10YR breakeven have risen from 12bps to 1.61% from last week’s three year low, 1.49%.

The Bloomberg Commodity Index (BCOM) has gained a relatively modest 2.4% in September. Gold is BCOM’s biggest weighting and is down 1.9% after an otherwise strong year including four consecutive months of healthy gains. The 2nd biggest component, crude oil, is +5% MTD and +11% from last week’s low. #3 natty gas is +10.7% MTD, coffee +6.9% MTD, and Dr. copper +2.8% MTD.

Overseas 26 of the 30 global equity indices we track are higher on the month led by Japan, China, South Korea, Russia, Germany and Sweden. The MSCI World Index is +1.9% MTD and the MSCI Emerging Markets Index is +2.4% MTD.

Locally in the U.S. it is small caps outperforming large led by the Russell Microcap Index (+4.5% MTD) and Russell 2000 (+3.4%) vs. the large cap S&P 500 (+1.8%) and Nasdaq 100 (+2.7%). The Russell 1000 Value Index is +3.5% MTD vs. the Growth Index which is barely positive at 0.2% MTD.

Energy (+5.9% MTD) and financials (+3.9% MTD) are leading the eleven Level I GICS sectors. Coming in third is the Industrials sector (+3% MTD) which from a technical perspective has a very interesting setup.

The S&P 500 Industrials Index (S5INDU) is currently +21% YTD but like many global indices made its cycle high back in January 2018. At that time the industrials Index was coming off annual gains of 16% and 19% in 2016 and 2017 and its weekly RSI (a measure of momentum) reached an extremely overbought, 14 year high of 81. It then went on to give back 26% at its December 2018 lows and a decline of 15% for calendar year 2018, its worst annual performance since 2008.

The Industrials Index now remains 3.5% from its January 2018 high. This long period of corrective price action has morphed into a large “continuation pattern” (inverse head & shoulders) seen in the below chart 1. A breakout above the slightly declining neckline carries a minimum measured move to the 825 level, +25% from last sale.

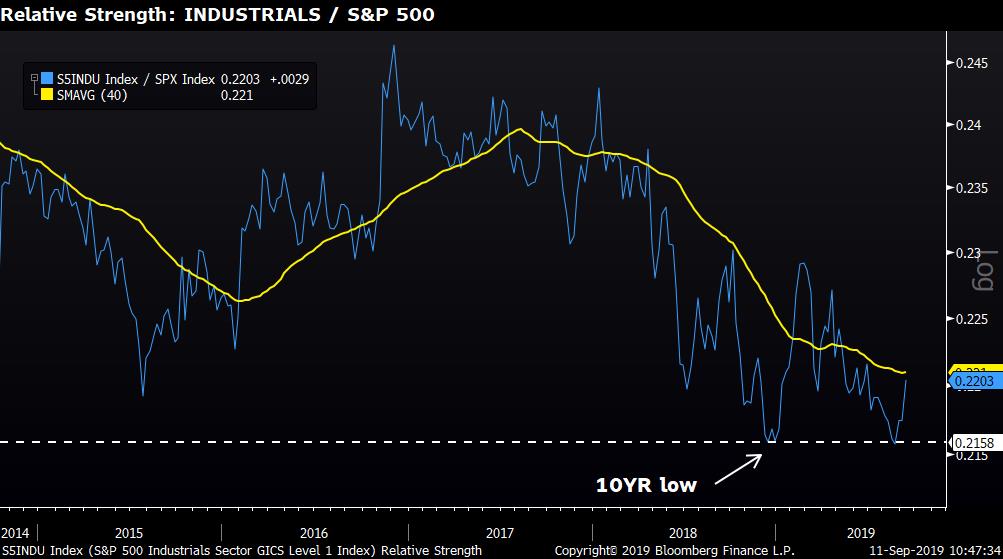

Relative to the S&P 500 the Industrials index has work to do but there are reasons to believe the recent outperformance can continue. The ratio of the s5INDU/SPX made a ten year low in December 2018 which at the time formed a small “double bottom” pattern. Two weeks ago it retested this key support and is now rebounding higher reflecting the recent outperformance. The first key test from here will be a move back above the 40-week moving average (yellow line) which many use as a bullish signal, followed by a move above its 2019 high.

With growing expectations for increased fiscal stimulus across the globe, particularly in Germany, there are reasons to believe we just may be in the early stages of a prolonged rotation into previously underperforming cyclicals like Industrials and materials. However if global policymakers and bankers fail to follow through with fresh stimulus outside of deeper negative rates, this September start could turn into a dead cat bounce.

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Stocks

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio