Stocks Continue to Add to Modest Gains

Market Movers

- A significant amount of economic data released today shows a resilient economy and low inflation pressure

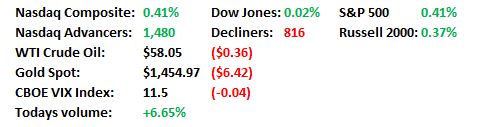

- Indexes are mixed, with the S&P 500 and Nasdaq 100 hitting new intra-day records while the Dow slipped slightly.

- Stock markets will close tomorrow for thanksgiving and will have a 1 p.m. close on Friday.

Mike’s Commentary

Stocks were quiet yesterday as expected. The modest gains in the Dow, S&P 500 and Nasdaq 100 were enough to lift each to new record highs. The mood on Wall Street is good especially after what was deemed a positive phone call between US and China trade representatives. The calendar is in our favor too. The Dow Jones Industrial Average has only suffered 16 losses in the past 66 years for the Wednesday before Thanksgiving and the Friday after combined, according to the Stock Trader’s Almanac. The Dow gained nearly 350 points in the days before and after Thanksgiving in 2008, the best two-day performance since 1952, according to the Stock Trader’s Almanac. The worst two-day performance goes to 2011, when the Dow lost 261 points during those days around Thanksgiving.

So far today the slow upward inertia continues as overseas markets handed off the lead to the US. With the MSCI rebalance out of the way, we'd expect volumes to slow today and even more so on Friday's half day session - usually one of the year's lightest.

Over the past two days we've had a week's worth of economic releases. Today, the second look at Q3 GDP showed 2.1% growth vs. the survey estimate - and advance GDP report - of 1.9%. Personal consumption of 2.9% also beat the 2.8% estimate. Consumer spending is of course a key driver for the economy. Core prices rose 2.1% in Q3, which while below the 2.2% survey estimate may cheer the Fed which wants to see 2% inflation. October Durable Goods Orders - namely US business equipment - unexpectedly rose 0.6% instead of the 0.9% decline forecast for the strongest reading since the start of the year. Durables ex-transportation rose 0.6% against a 0.1% forecast and capital goods orders and shipments also had better than expected results.

Investors that were watching with concern the decline in capital spending therefore have something to like here. Initial jobless claims fell to 213,000 vs. the survey estimate of 221,000 and the prior revised reading of 228,00 with continuing claims of 1.64 million also below the 1.69 million estimate. So there was something positive in virtually all of the data released pre-open.

At 10:00 a.m. new data releases were more mixed but did not impact stock performance much. Personal income was flat instead of a 0.3% expected gain. Consumer purchases adjusted for inflation rose only 0.1%. This was better than the forecast for no gain but was the weakest reading since February. Home sales fell 1.7% instead of a 0.2% expected gain with all regions except the Northeast seeing declines. And the Fed's preferred inflation measure, the PCE Core Deflator showed a 0.2% gain (vs. 0.3% estimated) which indicates low inflation. One side of that coin is room to cut rates. The other is slow growth. The releases fit well into the stock-market-friendly "goldilocks" narrative of a not too hot or cold economy as the Fed holds steady, while remaining accommodative.

So, the S&P 500, Nasdaq Composite and Nasdaq 100 indexes show slight gains as of mid-morning, putting them at new records. The Dow is lagging, dragged down by Boeing's developments but slightly in the green as we write.

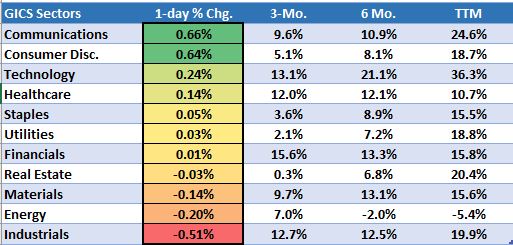

Sector performance shows strength in growth areas like Tech and Healthcare and weakness in some of the more economically sensitive sectors like Materials and Industrials. All of this is at the margin of course given the modest movements.

Finally, for those of not you on the road as part of the estimated 54 million travelers (89% of whom will drive) this Thanksgiving, expected to consume 46 million turkeys Thursday, you are still at work just like me. My guess is that readership for today’s note, the last of the week due to Friday’s early close, will be sparse. In the meantime, check out Jason Gay's "25 Rules for Thanksgiving Football" - a must read every year - in the WSJ. Happy Thanksgiving everyone!

Sector Recap

Brian’s Technical Take

Consumer Discretionary and Technology were the leading cyclicals driving the market higher in 1H’19. August brought with it widespread selling for all groups, however the ensuing rebound off the lows saw Technology quickly resume to new highs. That has not been the case for Discretionary which until this week has seen four months of corrective price action.

Today Discretionary is leading all of the eleven GICS sectors with a again of 0.7%. This is its fourth consecutive day in the green and over the last five sessions it also leads all groups with a gain of 2.5%. More importantly this week’s gains are “breaking out” from the declining four month trend line which may signal a transition from consolidation to trend.

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen-based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen-based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq, Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Stocks

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio