Solventum SOLV enters 2026 with a mix of momentum and moving parts. First-quarter 2026 results showed organic sales growth across all segments and adjusted earnings per share above expectations. Management kept its full-year organic sales growth outlook at the high end of its range and still sees earnings trending toward the top end.

The market is now debating how long operating discipline can carry the story, especially as tariffs and portfolio simplification create cross-currents.

The Setup for a 2026 to 2027 Margin Story

The core setup is a multi-year operating discipline narrative that can extend into 2027. Solventum’s Transform for the Future initiative and ongoing separation execution are positioned to support margin expansion over time, even as near-term pressure points remain.

Separation progress is a key part of that foundation. The company has exited just over half of its transition service agreements and expects to exceed 90% by the end of 2026. Management also expects the final large enterprise resource planning cutover in the United States and Canada in the third quarter of 2026, which can reduce disruption risk and free up resources for efficiency work.

Image Source: Zacks Investment Research

Solventum AI Coding Could Reshape HIS Growth

Health Information Systems is increasingly tied to customer demand for automation, and that includes rising interest in AI-enabled autonomous coding. Solventum points to its reimbursement data sets, proprietary workflows, and deep coding expertise as advantages in building tools that improve accuracy, compliance, and scalability for providers.

That positioning connects directly to what showed up in the first quarter. Health Information Systems posted 4.7% organic growth, with strength in revenue cycle management and performance management solutions. Management highlighted traction in autonomous coding offerings across inpatient and outpatient settings, supported by retention, backlog conversion and international expansion.

SOLV’s Transform for the Future Cost Savings Path

Transform for the Future targets about $500 million of annual cost savings through operational efficiencies, system streamlining and automation. The timing matters: most of the benefits are expected in 2027 and beyond, which is why investors are framing 2026 as a bridge year rather than the destination.

Even so, management is still targeting 50 to 100 basis points of operating margin expansion in 2026. That goal reflects sales leverage, programmatic savings, and portfolio actions, and it is being maintained despite higher tariff costs.

SOLV 3M Supply Agreement Risk in 2027

Another margin debate sits beyond 2026. Under Solventum’s long-term supply agreement with 3M Company MMM, 3M holds a contractual option in 2027 to raise the cost of certain raw materials supplied to Solventum. If exercised, that step-up could create a 100-basis-point margin headwind.

Mitigation is already part of the plan. Solventum has said it is working with 3M to explore alternatives, and it also owns the intellectual property rights for these materials within its field of use. That structure gives Solventum the option to source the materials from other chemical manufacturers if needed.

Solventum SKU Exits Create a 2026 Growth Trade-Off

Portfolio simplification is also creating a measurable growth trade-off in 2026. Solventum is continuing a multi-year SKU rationalization program, and management said SKU exits reduced first-quarter organic sales growth by about 100 basis points. The company expects the same 100-basis-point reduction to full-year 2026 organic sales growth from continued exits.

The impact is most pronounced in MedSurg, particularly within Infection Prevention and Surgical Solutions. Investors may still view this as an investment in simplification that can improve execution and efficiency over time, even if it makes the 2026 growth comparison less clean.

SOLV What Would Change the Narrative

The upside markers are tied to execution and cadence. Solventum, currently carrying a Zacks Rank #3 (Hold), expects to launch nearly 20 new products over the next two years, with a meaningful portion in key growth-driver categories. Sustained commercial execution, selective tuck-in acquisitions, and share repurchases also sit on the list of potential narrative shifters. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The downside markers are clearer and easier to model. Tariffs remain a watch point, SKU exits are a known 2026 headwind, and the 2027 raw material step-up under the 3M agreement is a defined risk if not mitigated.

In the broader healthcare landscape, peers such as Stryker SYK are also judged on mix, operational discipline and procedure-driven demand. For Solventum, the near-term debate is whether efficiency and product momentum can outlast the policy and portfolio noise, and whether the 2027 setup improves as execution milestones are cleared.

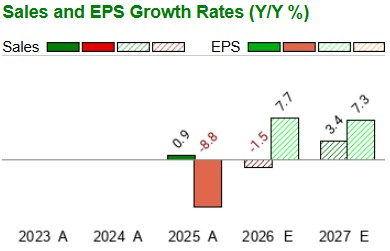

SOLV’s Sales & EPS Picture

In 2026, SOLV is expected to experience a 1.5% decline in revenues. On the profitability front, earnings per share are expected to improve 7.7% year over year.

Image Source: Zacks Investment Research

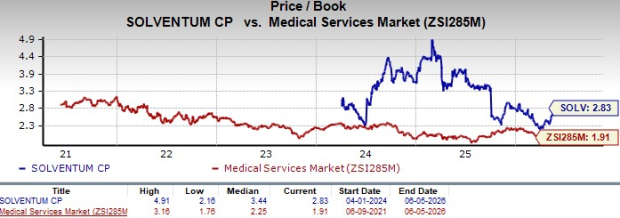

SOLV’s Valuation Picture

SOLV currently trades at a price-to-book ratio of 2.83X, well below its median level of 3.44X over the past five years.

Image Source: Zacks Investment Research

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up3M Company (MMM) : Free Stock Analysis Report

Stryker Corporation (SYK) : Free Stock Analysis Report

Solventum Corporation (SOLV) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.