AppLovin Corporation APP will report its third-quarter 2024 results on Nov. 6, after the bell.

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

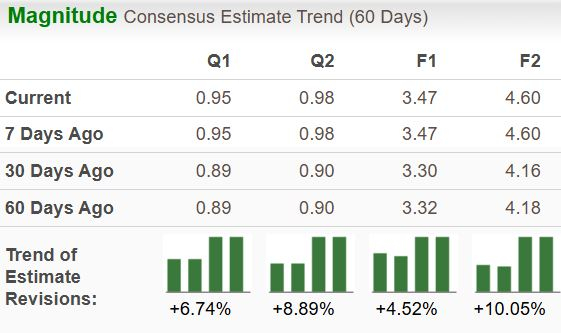

The Zacks Consensus Estimate for earnings in the to-be-reported quarter stands at 95 cents, indicating 216.7% growth from the year-ago reported quarter. The consensus estimate for revenues stands at $1.13 billion, implying 30.8% year-over-year growth.

One estimate for the to-be-reported quarter has been revised upwards over the past 30 days versus no southward revisions. Over the same period, the Zacks Consensus Estimate for 2024 earnings has increased 6.7%.

br< Image Source: Zacks Investment Research

br< Image Source: Zacks Investment Research

The company has an impressive earnings surprise history. Earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, with an earnings surprise of 21.1% on average.

AppLovin Corporation Price and EPS Surprise

AppLovin Corporation price-eps-surprise | AppLovin Corporation Quote

Q3 Earnings Beat Seems Unlikely for APP

Our proven model doesn’t conclusively predict an earnings beat for APP this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they're reported with our Earnings ESP Filter.

APP has an Earnings ESP of -4.71% and a Zacks Rank #2.

You can see the complete list of today’s Zacks #1 Rank stocks here.

All Round Healthy Business Should Drive Performance Growth

We expect year-over-year improvement in the company’s top line in the to-be-reported quarter to be driven by an increase in the Software Platform, as well as Apps revenues. The consensus estimate for the Software Platform revenues is pegged at $763.44 million, indicating 51% year-over-year growth. The consensus mark for Appsrevenuesis pegged at $367.72 million, suggesting 2.2% year-over-year growth.

The consensus mark for Software Platform’s adjusted EBITDA is pegged at $559.3 million, suggesting 53.6% year-over-year growth. App’s adjusted EBITDA is expected to increase 50.8% year over year.

APP Stock is in a Great Mood

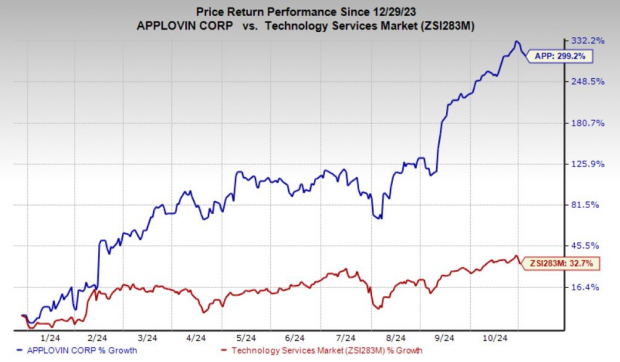

APP has rallied a massive 299.2% year to date, significantly outperforming the industry's 32.7% rally. This is in line with its competitors in the in-game mobile advertising space, as Alphabet Inc. GOOGL has gained 21.2%, and Meta Platforms META has surged 58.5% year to date.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Despite such an impressive rally, the stock is in the undervalued zone. Based on training 12-month EV-to-EBITDA, APP is trading at 34.11X, way below the industry’s 49.45X. If we look at the forward 12-month Price/Earnings ratio, APP shares are currently trading at 35.92X forward earnings, below the industry’s 38.13X.

Investment Risk and Rewards for APP

The introduction of AXON 2.0 technology and strategic expansion in gaming studios have significantly boosted APP’s revenue growth. Management has shown interest in expanding the software business by moving into new verticals from its original gaming background. In the second quarter of 2024, AppLovin launched a pilot program that enables e-commerce shops with websites to purchase in-app mobile game video ad inventory.

These advertisements direct game users to the website of the e-commerce shop. The crucial part is that management anticipates its software business to grow by 20-30% in the longer run without being dependent on the expansion of its verticals beyond gaming. Therefore, AppLovin’s successful expansion outside gaming could boost the software business and help it grow beyond the original goal.

Although there are potential risks, such as the possibility of slowed growth in the in-game advertising segment and the uncertain impact of non-gaming ventures, AppLovin appears well-positioned for continued growth thanks to its technological advancements and strategic expansion efforts.

What You Should Do With APP Stock?

Given AppLovin’s impressive financial performance, growth potential, and undervalued stock price, it presents a strong buying opportunity for investors. The combination of strong revenue and earnings growth, coupled with increasing analyst confidence, makes APP a compelling investment. While the stock has surged considerably, its current valuation suggests there is still room for further upside.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 228 positions with double- and triple-digit gains in 2023 alone.

AppLovin Corporation (APP) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.