Some people have noticed that short interest is at all-time high levels. Today, we put that data in context and see that the rise in short interest is more than explained by the increases in shares outstanding.

In short, relative short interest hasn’t increased at all. In fact, it has fallen and remains relatively low.

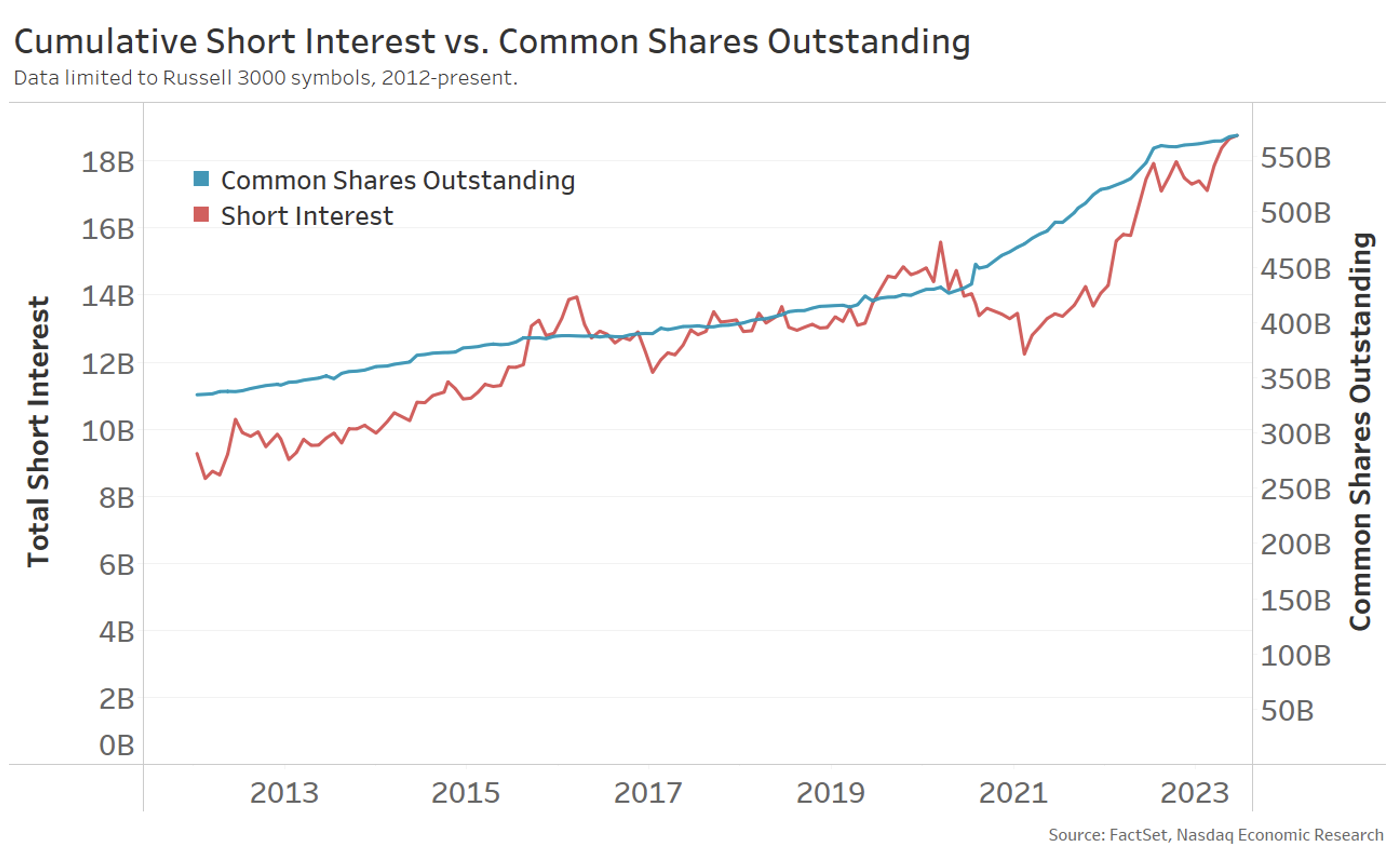

Shorts have increased as shares have increased

Looking at short interest alone (red line below), we see that overall shorted shares fell as the market sold off in 2020 due to Covid. It only fell a little more as the first wave of MEME stock trading, which was focused on the most shorted stocks, happened in January 2021.

Since then, it has increased, recently reaching new highs.

However, plotting short interest alongside shares outstanding tells a different story. Rather than being elevated, we see that short interest is tracking outstanding shares higher. Remember, we saw some significant stock splits in 2022 and a burst of IPO activity as the market recovered from Covid, with interest rates close to zero.

Chart 1: Short interest has mostly tracked shares outstanding higher

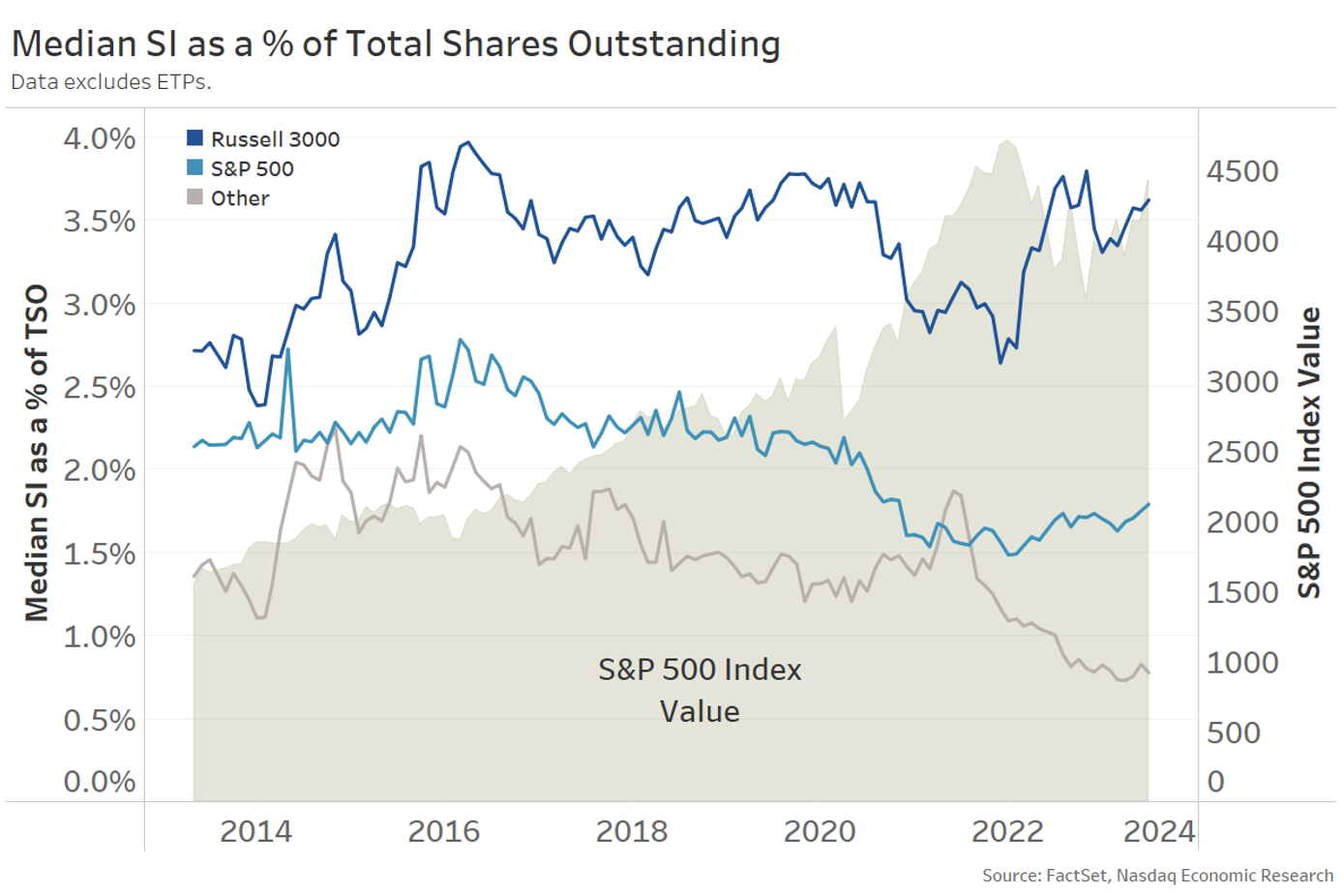

Shorts have fallen as a proportion of shares outstanding

If we look at the ratio of shorts to shares outstanding, we see that since 2023, that ratio has fallen. Especially for large-cap (S&P 500, light blue line) and micro-cap stocks (grey line), where the ratio remains near decade lows.

S&P 500 stocks may also be borrowed to hedge liquid NDX and SPX futures and options arbitrage positions, so it’s surprising they don’t have a systematically higher short interest.

Stocks that are in the Russell 3000, but not the S&P 500, could be considered small- and mid-cap stocks (dark blue line). Data shows these stocks typically have higher short interest, but that also stays consistently in a range of around 3-4%.

Short interest ratios are very stable, considering some large gyration in stock prices (grey area below), including the large Covid selloff in 2020 and record highs for the S&P 500 reached in December 2021, before rate hikes again caused stocks to sell off.

That shows that market highs and lows don’t change short interest much!

Chart 2: Short interest ratio has fallen over the past 10 years

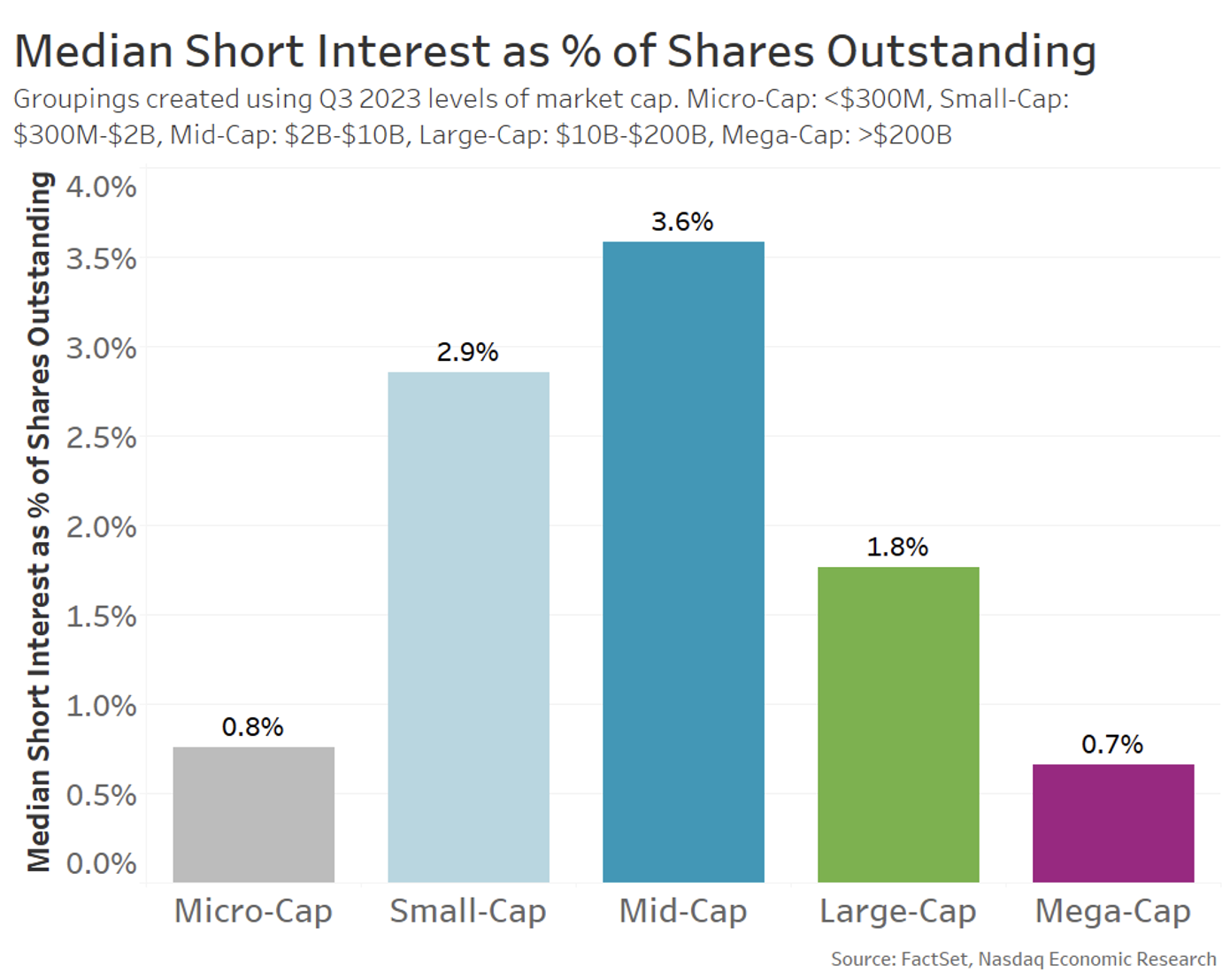

Looking at shorts by market cap

Looking at short interest ratios by market caps confirms what we see in Chart 2 – that stocks in the “rest” of the Russell 3000 (being mid- and small-cap stocks) tend to have higher short interest.

Interestingly, the mega-cap stocks that have led the U.S. markets higher have even lower short interest.

Short interest is also very low for micro-cap stocks.

Chart 3: Typical short interest (by market cap)

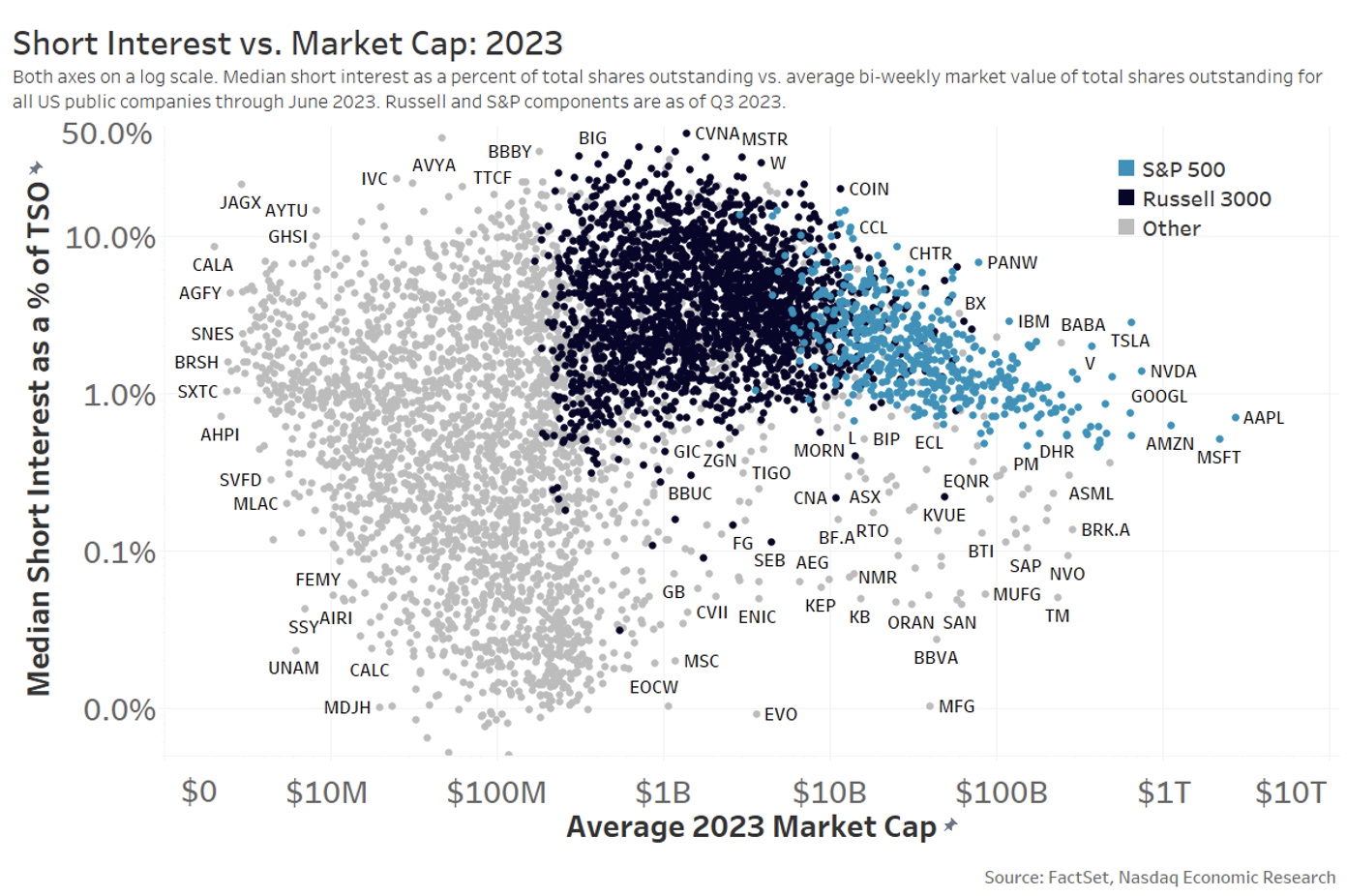

Looking at shorts by index membership

Looking at the short-interest ratio for each stock in the market as market cap increases (Chart 4) shows the ranges around the values in Chart 3 above. By coloring each stock (dot) by index membership – we see all the blue dots (in either the Russell 3000 or the S&P 500 index) are stocks likely held by institutional investors.

Being in institutional indexes clearly makes a difference to short interest. In general, almost none of those stocks have short interest below 1% of their shares outstanding. That alone would increase the median value of small- and mid-cap short interest (as it moves, the middle of the dark blue dot cluster is higher).

Why might this occur?

Index inclusion also means inclusion in ETFs, which represent net-long positions worth trillions of dollars. However, ETFs need arbitrageurs to keep prices efficient and are often used by hedge funds against a long stock position.

Chart 4: Short interest ratio for all stocks shows the impact of index inclusion

We also see that larger stocks that are not included in the S&P 500 (grey dots on the right, like BRK.A) tend to have much lower short interest.

In addition, micro-cap stocks (grey dots to the left of the Russell 300 cutoff) often have lower short interest, too. Remember from our blog last week these stocks also tend to typically have more retail trading.

That may also be because stocks outside of professional investor benchmarks aren’t set up as frequently to loan, making it harder to borrow those shares, which is required before putting on a short.

However, some micro-cap stocks do have high short interest. One stock worth highlighting is BBBY, which in April 2023 filed for Chapter 11 bankruptcy protection. That’s consistent with other research that shows shorts tend to improve price discovery in the stock market.

Study shows shorts are down

This data shows it’s important to think about short interest properly.

Although short shares are at record levels, the actual short interest ratio is down, and for large-cap stocks, it remains near decade lows.

Market Makers Newsletter

Sign up for our newsletter to get the latest on the transformative forces shaping the global economy, delivered every Thursday.

Latest articles

This data feed is not available at this time.

Data is currently not available