David Tsoi, CFA, CAIA, FRM, CESGA, CAMS, Lead Index Research Strategist

- Among Nasdaq-100 firms that have reported Q3 results, 81% topped analysts’ earnings estimates by index weight. Recent tech earnings underscore AI’s structural growth, as leading players signaled a sharp rise in capital expenditures (capex) amid broad-based demand for AI and its infrastructure. Accelerating cloud revenue across major platforms further strengthens confidence in AI’s monetization prospects. While the current AI investment surge is notable, its scale relative to GDP remains below that of the late-1990s tech boom and the 19th-century railroad expansion.

Source: Bloomberg.

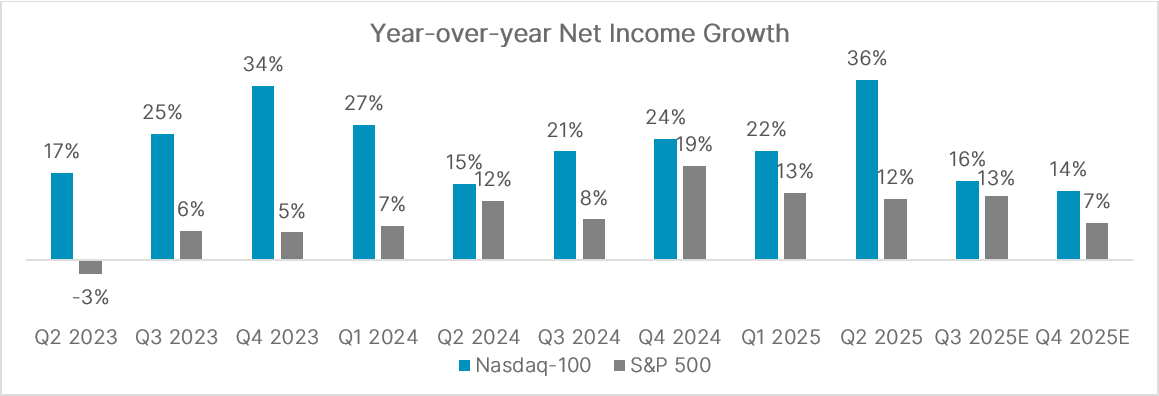

- Nasdaq-100 net income is on track for approximately 16% year-over-year growth in the third quarter, marking the tenth straight quarter of expansion above 15% and outperforming the S&P 500. Notably, the technology sector is projected to lead with 20% growth, the highest among all ICB industries within the Nasdaq-100, reinforcing its leadership role in driving overall performance.

Source: FactSet. Data as of November 7, 2025.

Q3 Earnings Update for Major Nasdaq-100 Constituents

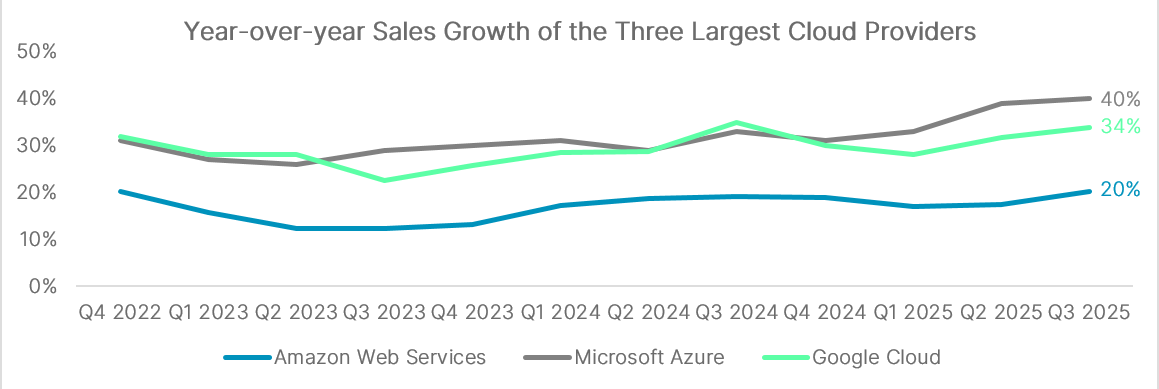

- Microsoft’s quarterly revenue climbed 18% to US$77.7 billion, topping consensus estimates. Azure and other cloud services delivered 40% year-over-year sales growth, beating Wall Street expectations. Demand continued to outpace supply across workloads despite increased capacity during the quarter. The company now counts 900 million monthly active users of AI features across its products. Fueled by accelerating demand for its cloud and AI offerings, Microsoft invested US$34.9 billion in capex, including leases, in Q3.

- Apple’s Q3 revenue rose 8% to US$102.5 billion, modestly ahead of consensus. iPhone sales gained 6% to US$49.0 billion, slightly below analyst projections. The quarter featured roughly two weeks of iPhone 17 availability, with initial demand signaling robust consumer interest. Supply constraints weighed on Greater China, where revenue declined 4% to US$14.5 billion. Management anticipates a sharp rebound this quarter, with China returning to growth and total sales rising 10% to 12%, pointing to the strongest holiday season in years. Services remain a key growth driver, with revenue up 15% to US$28.8 billion. Tariff-related costs totaled US$1.1 billion in Q3, in line with Apple’s expectations.

- Amazon’s quarterly revenue and profit rose 13% and 38%, respectively, both surpassing consensus estimates. Amazon Web Services (AWS) delivered a 20% sales increase to US$33 billion, its strongest year-over-year growth since the launch of ChatGPT in late 2022, despite lagging Microsoft Azure and Google Cloud in growth rate. The upside beat underscores AWS’s resilience, further reinforced by a US$38 billion, seven-year agreement to supply OpenAI with Nvidia GPUs, highlighting its capability to scale massive data center networks. Core retail operations remained solid, with online store sales up 10% to US$67.4 billion and third-party seller services advancing 12% to US$42.5 billion. Management projects full-year capex to reach approximately US$125 billion in 2025.

- Meta’s Q3 revenue jumped 26% to US$51.2 billion, beating analyst expectations and underscoring the strength of its core advertising business, which accounts for 98% of total revenue. The average price per ad rose 10% year-over-year, supported by stronger advertiser demand largely driven by improved ad performance. Meta’s family of apps reached an average of 3.54 billion daily active users in September 2025, up 8% from a year ago. The company raised the lower end of its 2025 capex forecast by US$4 billion, setting a range of US$70 billion to US$72 billion. Meta also recorded a one-time, non-cash income tax charge of US$15.9 billion in Q3 related to the implementation of the One Big Beautiful Bill Act. Additionally, it completed a US$30 billion bond sale, the largest high-grade U.S. note issuance since 2023.

- Alphabet, Google’s parent company, posted strong Q3 results with revenue up 16% year-over-year to US$102.3 billion. Cloud sales surged 34% to US$15.2 billion, reinforcing its position as Alphabet’s fastest-growing segment and a clear beneficiary of the AI boom. Cloud backlog climbed 46% quarter-over-quarter to US$155 billion, providing solid visibility into future demand. Google Search, the engine behind Alphabet’s advertising dominance, delivered 15% growth, successfully fending off rising competition from AI chatbots. Investments in new AI features, such as AI Overviews and AI Mode, continue to boost overall queries. The company processed over 1.3 quadrillion tokens in October, marking more than 20-fold growth year over year. Capex are now projected at US$91 billion to US$93 billion for the year, up from the prior estimate of US$85 billion.

- Tesla’s Q3 adjusted net income fell 29% year-over-year to US$1.8 billion, coming in below expectations. Operating expenses surged 50% to US$3.4 billion, with tariff costs exceeding US$400 million. The company delivered a record 497,099 vehicles globally during the quarter as buyers rushed to take advantage of a US$7,500 U.S. electric vehicle tax credit that expired on September 30. Tesla expects its robotaxi business, launched in Austin, Texas in June, to expand to as many as 10 metropolitan areas by year-end, subject to regulatory approvals.

Name of Company | Revenue Growth (yoy) | Profit Growth (yoy) | Q3 Revenue | Q3 EPS |

|---|---|---|---|---|

| Microsoft | 18% | 25% | 3% | 12% |

| Apple | 8% | 10% | 0.2% | 3% |

| Amazon | 13% | 38% | 1% | 24% |

| Alphabet | 16% | 22% | 2% | 24% |

| Meta | 26% | 5% | 4% | -6% |

| Tesla | 12% | -29% | 3% | -12% |

Source: Nasdaq Global Indexes, FactSet, company filings.

Note: Figures are on non-GAAP basis. Excluding the one-time tax charge, Meta’s Q3 net income would have risen to US$18.64 billion.

- As of November 7, 82 companies in the Nasdaq-100 (75% by weight) have reported Q3 earnings. On average, these firms beat their revenue and earnings estimates for the quarter by 2.4% and 4.9%, respectively, with 57 companies (59% by weight) exceeding both top-line and bottom-line expectations.

- Index-weighted top- and bottom-line beats have softened compared to last quarter. By constituent count, revenue beat rates are in line with prior-quarter levels, while earnings beat rates remain lower.

| Beats | Misses | ||

|---|---|---|---|---|

No. of firms / | Average | No. of firms / Index weight | Average | |

| Q3 25 Revenues | 72 / 72.4% | 2.8% | 10 / 3.1% | -1.0% |

| Q3 25 Earnings | 64 / 61.2% | 9.0% | 18 / 14.2% | -8.7% |

Source: Nasdaq Global Indexes, FactSet. Data as of November 7, 2025.

Disclaimer:

Nasdaq®, Nasdaq-100® and Nasdaq-100 Index® are registered trademarks of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.

© 2025. Nasdaq, Inc. All Rights Reserved.

Latest articles

This data feed is not available at this time.

Data is currently not available