Money Management 101: Your Personal Finance Guide

Disclaimer: Nothing in this article should ever be considered advice, research or an invitation to buy or sell securities. I am not a financial advisor.

Money is one of the most effective tools that can enable us to reach our goals.

There are also a lot of misconceptions and conflicting opinions in regards to a variety of different money-related topics. The end result can be viewing money management as an incredibly complicated subject.

However, that can’t be farther from the truth. The reality is that the majority of our personal financial decisions can be boiled down to some basic math. That is the purpose of this guide.

More specifically, this guide will be covering the five foundational pillars of personal finance and explaining how we can get started today.

With that being said, let’s dive in.

What is Personal Finance?

In a nutshell, personal finance refers to how we save, spend and invest our money.

Managing and optimizing our personal financial decisions can lead to:

- Building wealth and achieving financial independence

- Giving ourselves more options on how to live our lives

- Decreasing our financial anxiety and overall stress levels

- Having peace of mind knowing that we can achieve our goals

From day-to-day decisions such as determining our weekly food budget to more longer-term decisions like purchasing a home, personal finance is engrained in almost every aspect of our lives.

As a result – when making any financial decision – we need to be cognizant of two principles:

- All financial decisions that we make (big and small) are connected

- Our financial decisions compound over time

To showcase these two principles, let’s look at our example from earlier.

The size of our food budget can impact the amount of money that we can save towards a down payment on a house. If we can find ways to decrease our overall food budget (couponing, buying in bulk, etc.), then we can save more money over time for a down payment. However, the reverse is also true. If we consistently spend a lot of money on food, then we will have less money over time for a down payment.

By understanding that everything is connected and that our decisions compound over time, we can better understand how we can optimize our finances in order to meet our different life and financial goals.

With this in mind, let’s jump into the first foundational pillar of personal finance.

1. Setting Short, Medium & Long-Term Financial Goals

The first and most important pillar of personal finance is developing our personal financial roadmap.

This is a critical piece of money management. That is because the purpose of a financial roadmap is defining the short, medium & long-term financial goals that we ultimately want to achieve. With these goals clearly defined, we can then optimize our financial decision-making in support of these goals.

When creating financial goals, they should not be purposefully vague with no clear definition of success.

Instead, we should strive for our financial goals to be SMART (Smart, Measurable, Achievable, Relevant, Time-Bound). Using the SMART Methodology has a lot of great benefits including:

- Breaking down our plans into smaller chunks

- Measuring progress against our goals

- Increasing our confidence in achieving our goals

- Decreasing feelings of unnecessary financial stress

By methodically breaking down our financial goals, we can begin developing a clear path to success.

While everyone has different financial goals, let’s go over a few examples of what some short, medium and long-term SMART financial goals can look like.

Short-Term Financial Goals (< 1 Year)

Short-term financial goals are goals that we can reasonably expect to achieve within a year.

Examples of short-term financial goals can include:

- Making $2,000 in additional payments towards student loans

- Saving $5,000 towards an emergency fund

- Paying off $3,000 in existing credit card balances

Medium-Term Financial Goals (1 - 5 Years)

Medium-term financial goals are goals that we can reasonably expect to achieve within 1 – 5 years.

Examples of medium-term financial goals can include:

- Saving $20,000 for a down payment on a house in the next 5 years

- Increasing our personal income by 20% in the next 3 years

- Having $0 in credit card balances in the next 2 years

Long-Term Financial Goals (5+ Years)

Long-term financial goals are goals that we can reasonably expect to achieve within 5+ years.

Examples of long-term financial goals can include:

- Achieving financial independenceby age 50 with a portfolio of $1,000,000

- Saving $30,000 in a 529 Plan by the time our child turns 18

- Paying off our mortgage in 25 years

2. Creating a Realistic Budget

The second pillar of personal finance is creating a realistic budget.

In a nutshell, our budget represents our overall spending plan based on our income and expenses.

Creating a realistic budget is critical in regards to achieving our short, medium and long-term financial goals. With that being said, let’s go over step-by-step what we can do in order to create a sustainable budget.

Review our Financial Goals

The first pillar of personal finance was creating and establishing short, medium and long-term financial goals using the SMART methodology.

This resulted in knowing the amount of money required in order to meet our goals. At this point, we can begin breaking down these goals even further to determine how much money we need to save per month in order to accomplish each goal.

As an example, one of the short-term goals we defined earlier was saving $5,000 towards our emergency fund in the next year. In order to achieve this, we would have to save $416.67 / month. Furthermore, achieving the medium-term goal of saving $20,000 in 5 years for a down payment on a house would require us to save $333.33 / month.

As a result, we would have to save $750 / month in order to meet both of these goals.

Track and Review our Expenses

Now that we have a baseline savings target, our next step would be to track and review our expenses.

When tracking our expenses, it’s important to do this over a period of several months in order to capture fluctuations in our spending habits. In other words, calculating an average spending rate will capture our everyday expenses (i.e., housing, food costs, etc.) as well as possible one-offs (i.e., vacations, car repairs, etc.)

We can manually track our expenses via a spreadsheet (i.e., Google Sheets, Microsoft Excel, etc.) or automatically in tools such as Mint or Empower.

With that being said, it may be worth manually tracking our expenses in the beginning. This will force us to be fully aware of every expense that we are making. After doing this exercise over the course of 3-6 months, we can then calculate how much we spend per month on average. This will end up being a much more accurate representation of our spending habits.

At this point, we can start comparing our average expenses with our income. This will signal to us whether or not we are able to support the financial goals that we have previously established.

As an example, let’s assume that our take-home pay is $5,000 / month and our average expenses total up to $4,500 / month. This would only leave us with the ability to save $500 / month vs the $750 / month required for us to reach our goals. This represents a $250 / month savings deficit and would mean that we would be unable to achieve both financial goals.

If we find ourselves in a deficit situation, our next steps should be to identify and adjust our budget wherever possible.

Minimize Expenses Wherever Possible

At this point, we have access to a full accounting of several months of expenses.

Using this data, we can begin the process of auditing our expenses. This includes actively reviewing all of our expenses and evaluating them against objective criteria, using questions such as:

- Does spending money on X make me any happier?

- Do I actively use this membership/subscription?

- Is spending money on X more important than reaching my goals?

By conducting an expense audit, we can find opportunities in order to increase our overall savings rate to a point where we can achieve our financial goals.

When choosing which expenses to decrease, it should be noted that the majority of the average Americans’ expenses come from 3 main categories: housing, food & transportation. As a result, saving money via these three categories will produce a greater impact to our savings rate vs cutting ‘fun items’ such as inexpensive hobbies.

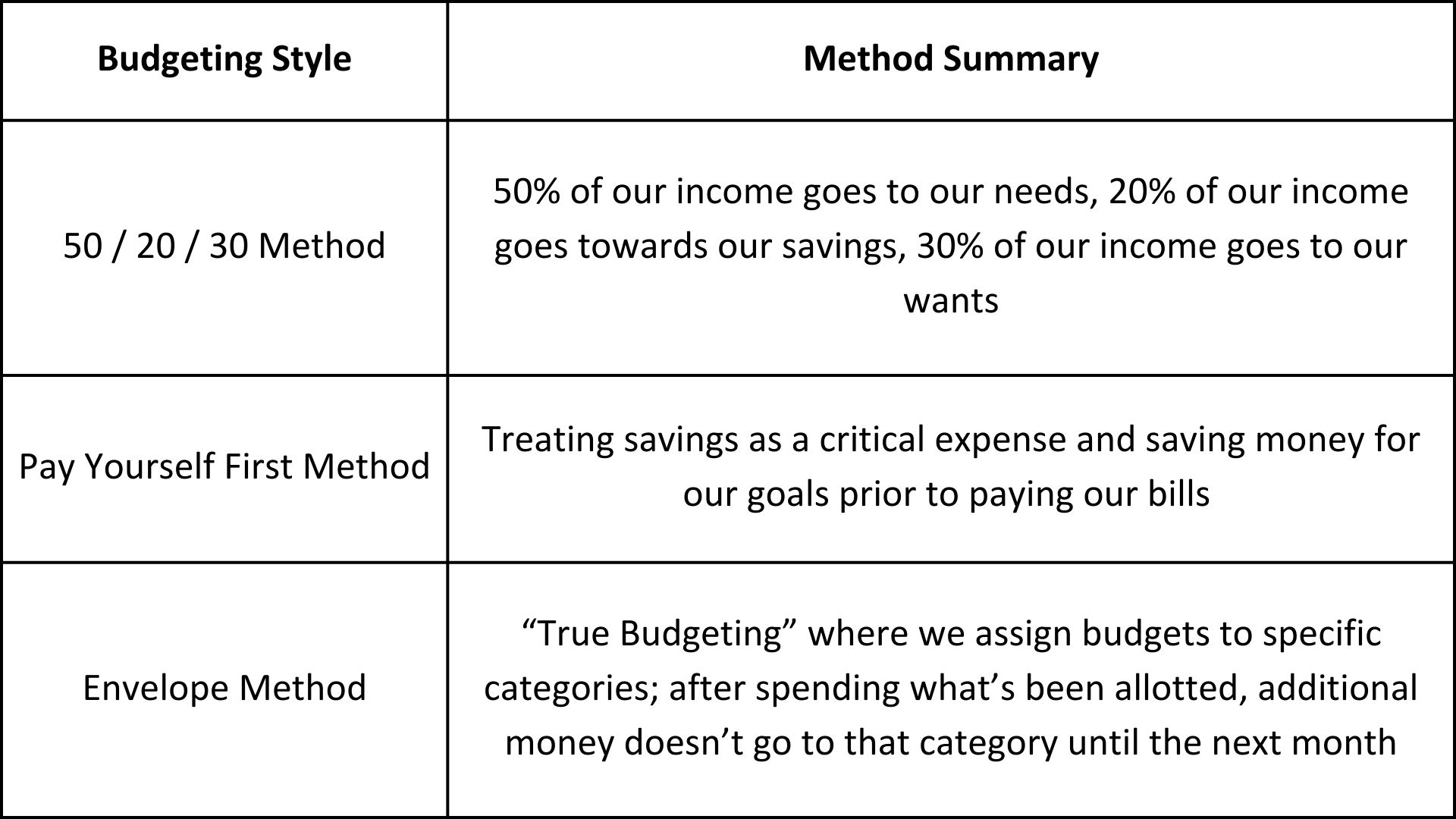

Choosing a Budgeting Style

The final step of creating a realistic budget is choosing a budgeting style that works best for our situation.

There is no right or wrong method to budgeting. At the end of the day, the “best” budgeting method is the one that helps us most effectively maintain the required savings rate in order to meet our goals.

With that being said, there are many popular budgeting styles out there including:

When establishing a budget and budget style, it’s important to keep in mind that it’s best not to treat this as a one and done exercise. We should continually experiment in order to create a fine-tuned method that works best for our specific situation.

And remember… as long as we are meeting our financial goals, that is all that matters!

How to Know We are Budgeting Correctly

There are two main metrics that we can track in order to measure our budgeting effectiveness.

The first metric is our savings rate or the % of money that we are able to save every month.

A functional budget will always result in a positive savings rate every month. In other words, we are not spending more than what we are making in a given month.

With that being said, emergencies do happen. This can potentially result in some months that may have a negative savings rate. Don’t worry – that is 100% OK. At the end of the day, as long as our long-term average savings rate is positive there is nothing to worry about.

The second metric that we can track is our net worth.

Our net worth includes our assets (i.e., cash, investments, property, etc.) minus our liabilities (i.e., loans, etc.).

If we are maintaining a positive savings rate over time, our net worth will naturally increase over time. By the same token, if we spend more than what we make over time (and not accumulating assets), then our net worth will naturally decline over time.

3. Building an Emergency Fund

In the latest ‘Stress in America’ Survey, the American Psychological Association found that 66% of American Adults reported money as a significant source of stress.

The survey went on to note that “of those who said money is a source of stress, most said that stress is about having enough money to pay for basic needs.”

So in the event that a financial emergency inevitably occurs - car breaking down, surprise medical bills, a lapse of employment – this can be particularly burdensome from both a financial and mental health perspective.

That leads us to the third pillar of personal finance: building an emergency fund.

The Importance of an Emergency Fund

An emergency fund is a fund comprised of liquid assets (i.e., cash, certificates of deposit, etc.) that can quickly be converted into cash in the case of an emergency.

There are many reasons why it’s important to prioritize and properly maintain an emergency fund.

First, emergency funds can provide us with a personal financial safety net that can prevent us from being blown too off course with our financial goals. Instead of hassling with adjusting our automated contributions to our retirement accounts or slashing our budgets to get the money required for an emergency, we can easily just withdraw it from our emergency fund.

Second, we are essentially acting as our own bank. With a properly established emergency fund, we are less likely to rely on less-than-ideal financial situations such as credit cards or predatory high interest loans that can have negative long-term financial consequences. At the end of the day, lending money to ourselves is completely free. This means that a $1,000 emergency will only cost us $1,000… not $1,000 with 25% - 30% interest payments attached.

Finally, an emergency fund results in us only having to deal with one problem versus two. That is because when an emergency does happen, our focus should be on resolving the problem at hand as soon as possible and not worrying about where we are going to find the money.

If we are not financially prepared, this can easily multiply the stress that we feel in the moment when something does pop up. As a result, while it may be annoying to lay out the money for an emergency, it’s much better than having to deal with the stress of figuring out where that money is coming from.

How to Build an Emergency Fund

A common baseline emergency fund to strive for is having enough easily accessible cash in order to cover 3-6 months of living expenses.

When building our emergency fund, it’s important to differentiate between our needs and wants and prioritizing being able to cover our basic living expenses (i.e., food, shelter, etc.). With that being said, the size of an individual’s emergency fund ultimately depends on a mixture of factors including:

- Individual risk tolerances

- Personal income situation

- Potential expenses on the horizon

However, where exactly should we be building our emergency fund?

At the end of the day, that is up to our own personal preferences. There is nothing wrong with keeping our emergency fund in a savings account with our current bank.

However, another option would be keeping our emergency fund in a separate online savings account with another bank that has the ability to earn much more interest.

Not only can this better protect our money against inflationary pressures, but this can also come with an additional psychological benefit. By having our emergency fund “walled off” at another bank (but still easily accessible) we may be less likely to dip into our emergency fund for non-emergency expenses.

Regardless of where we save our money, the most important thing to always check for is to make sure that the bank is FDIC insured. This will protect our money (up to $250K) in the event that a bank fails.

4. Paying Down Debt

The fourth pillar of personal finance is paying down debt.

This includes but is not limited to paying down credit cards, HELOCS, Mortgages, personal loans, automobile loans, student loans, etc.

The Math on Paying Down Debt vs Investing

A common question in personal finance is “Should I invest or pay down my debt?”

As with most answers in personal finance, the answer is often “it depends.”

From a mathematical perspective, we should always try to maximize every dollar that we spend/invest.

From an investing perspective, we may or may not earn a return on our money. With low-risk investments such as treasury bonds or savings accounts, we may have a guaranteed but sub-optimal return. On the other hand, investments such as stocks or mutual funds may have greater long-term returns on average, but this historical performance is not a guarantee of future returns.

However, paying down any debt always has a direct return on investment. If a credit card is charging us 20% interest every month, then paying off that debt would result in an instant 20% return on our money.

As a result, according to the time value of money, it may be more prudent to pay off this high interest debt rather than invest in stocks or bonds. That is because the probability of finding an investment that can earn +20% month-over-month is extremely low and likely not worth the effort and/or stress.

With that being said, we should evaluate our specific situations in order to understand what makes most sense in order to maximize our money.

Avalanche Method of Paying Down Debt

The avalanche method is the process of paying down debts with higher interest rates first.

The avalanche method of paying down debt is consistent with the time value of money and is considered the most optimal way in order to pay down debt. This would result in us paying down our most expensive debts first which would result in paying less overall interest in the long-run.

As an example, let’s assume that we have the following 3 loans:

- Loan 1 – 15% Interest, $20,000 Balance

- Loan 2 – 2% Interest, $5,000 Balance

- Loan 3 – 7% Interest, $1,000 Balance

Using the avalanche method, we would pay down these loans in the following order: Loan 1, Loan 3, Loan 2. All else being equal, this would result in paying the least amount of interest over time.

Snowball Method of Paying Down Debt

The snow ball method is the process of paying down debts with the lowest balances first.

While this method is not as mathematically efficient as the avalanche method, the snowball method is often leveraged in order to increase one’s motivation to paying off their debts. Let me explain.

By paying off our smallest debts first, we can get a sense of accomplishment associated with paying off these loans. At that point, we can have renewed sense of motivation as well as more available cash to then allocate towards paying off any additional debts that we may have.

Same as before, let’s assume that we have the following 3 loans:

- Loan 1 – 15% Interest, $20,000 Balance

- Loan 2 – 2% Interest, $5,000 Balance

- Loan 3 – 7% Interest, $1,000 Balance

Using the snowball method, we would pay down these loans in the following order: Loan 3, Loan 2, Loan 1. While this may not be as financially efficient as the avalanche method, it can provide a nice motivation-boost to continue actively working towards becoming debt-free.

5. Start Investing

The fifth and final pillar of personal finance is investing.

In a nutshell, investing is putting our money into different assets so that the money can grow. The primary goal of investing is to maximize returns and minimize friction (i.e., taxes, fees, interest paid, etc.).

Contrary to what we may have heard or read, the truth is that investing does not need to be complicated or overwhelming. By understanding the basics and keeping things simple, we can confidently begin setting ourselves up for success.

With that being said, let’s go over the basics of investing.

Types of Investments

There are many different types of assets that we can invest into.

However, we are going to keep things simple and go over the 4 most common investment classes:

Stocks represent fractional pieces of ownership in a company. Stocks can make money either through capital appreciation (stock price increasing) or the stock paying a dividend. Stocks are also referred to as shares or equities and are typically considered “riskier” assets.

Bonds represent debt issued by either a company or a government entity. Bonds do not represent ownership of an entity, i.e., holding a U.S. treasury bond doesn’t mean we own a piece of the U.S. Treasury.

Exchange Traded Funds & mutual funds are investment funds that represent a basket of investments (that can include stocks and bonds) in order to align with a particular investing strategy. While mutual funds and ETFs are very similar, they differ in some key respects, primarily:

- Mutual funds only trade once a day while ETFs trade throughout the day

- Mutual funds can require investment minimums whereas investing in ETFs only require paying the share price

- Most brokerage accounts don’t allow for automatic ETF investments due to price volatility

What we choose to specifically invest into should be based on our own individual financial goals, timelines and risk tolerances. As a result, what makes sense for one person may not necessarily make sense for another.

If you are not comfortable choosing your specific investments, it may be worthwhile to talk to a Certified Financial Planner to discuss which options make the most sense for your specific financial situation.

Types of Investment Accounts

When it comes to investing, there are many different types of investment accounts that we can leverage in order to minimize friction associated with investing (i.e., fees, taxes, etc.).

As a result, we shouldn’t default to lumping all our money/investments into one account. Instead, we should take advantage of all the available tax breaks that are available to us as investors.

Let’s now go over the three most common types of investment accounts.

Investment Brokerage Accounts are standard investment accounts where we can buy, sell and hold different types of investment assets.

These types of accounts are referred to as taxable or non-retirement brokerage accounts because they don’t have any special tax benefits. With that being said, they have no withdrawal penalties (just paying any applicable taxes and fees), no investment contribution caps & are a great option for short & medium-term investing.

Individual Retirement Accounts (IRAs) are tax-advantaged investment accounts that are specifically designed to save for retirement.

Similar to traditional brokerage accounts, IRAs also allow us to buy, sell and hold a variety of investments… except these accounts come with a nice tax break.

With a Roth IRA, any contributions that we make will grow tax-free and not be taxed upon withdrawal. On the other hand, contributions to a Traditional IRA are considered pre-tax contributions and will lower our taxable income today but will NOT grow tax-free and be taxed upon withdrawal. As a result, the type of IRA that we decide to contribute to depends on when we want to experience the tax benefits.

As of 2023, the total contributions that can be made to either IRA is capped to $6,500 / year or $7,500 / year if we are 50 or older.

Employer-Sponsored Plans are tax-advantaged investment accounts offered by an employer that are also specifically designed to save for retirement. The most common being the 401(k) plan.

Similar to IRAs, there are Roth 401(k)s and Traditional 401(k)s. A pre-tax contribution would lower our income today, but would require us to pay taxes on any investment gains upon withdrawal. A Roth contribution is made with money that has already been taxed, allowing that money and associated gains to grow tax-free.

A major benefit to employer-sponsored plans is when employers offer a contribution match. As an example, an employer may offer to match the first 6% that their employees make to a 401(k). This is one of the very rare opportunities in personal finance to get “free money” because these matches represent direct returns on the money that we contribute.

As of 2023, the total contributions that can be made to either type of 401(k) is capped to $22,500 / year or $30,000 / year if we are 50 or older.

General Investing/Saving Priority

With the recent surges in inflation, it’s more important than ever to optimize every dollar that we save, spend and invest.

As a result, below is a general funding priority guide for how we can stretch our dollars as far as possible:

- Fully fund our emergency fund

- Invest in a company 401(k) (up to the match, but not maxed)

- Pay off high-interest loans

- Continue investing via an IRA and or company 401(k)

- Pay down medium-interest loans

- Continue investing via a taxable brokerage account

- Pay down low-interest debt

For more information on the specific rationale behind this general funding priority guide, check out our post on how to optimize your investing strategy.

Final Thoughts

At first glance, personal finance and money management can appear daunting.

That is because money touches almost every aspect of our lives. As a result, it’s extremely important for us to have the knowledge in order to make the most appropriate financial decisions and maximize our hard-earned dollars.

In this guide, we covered the five foundational pillars of personal finance. If you want to continue your journey of learning more about personal finance and money management, navigate over to Nasdaq’s educational resources on personal finance for more detailed articles on the topics that you want to explore further.

Thank you for reading.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Personal Finance Investing