If you asked the professional analyst community about ride-sharing company Lyft (NASDAQ: LYFT), they'd collectively tell you that the stock has strong upside potential. As of this writing, the average price target from analysts is $18.69 per share, according to the 32 analysts tracked by TipRanks. That points to nearly 40% upside from where it trades, as of this writing.

That said, the analyst community is often wrong. And I believe that it's wrong again when it comes to its price target for Lyft. But I don't mean that in the way that you might think.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

I don't believe that analysts are overestimating the potential of a Lyft investment today. To the contrary, I believe it has much higher upside potential than what it gets credit for, and I consequently believe that Lyft stock is a buy today.

The business trends

There's no denying that Uber Technologies (NYSE: UBER) is the 800-pound gorilla in the ride-sharing space. But Lyft is solidly in second place in the U.S., benefiting from ongoing adoption trends. The ride-sharing space continues to gain ground, generally speaking. And this industry growth helped Lyft set a record for active riders in the third quarter of 2024.

In Q3, Lyft had 24.4 million active riders, up 9% year over year. The company also set a record for rides during the quarter. There were 217 million rides in Q3, up 16%. Therefore, these metrics clearly demonstrate two things: Lyft is attracting more users, and these users are riding with Lyft more frequently.

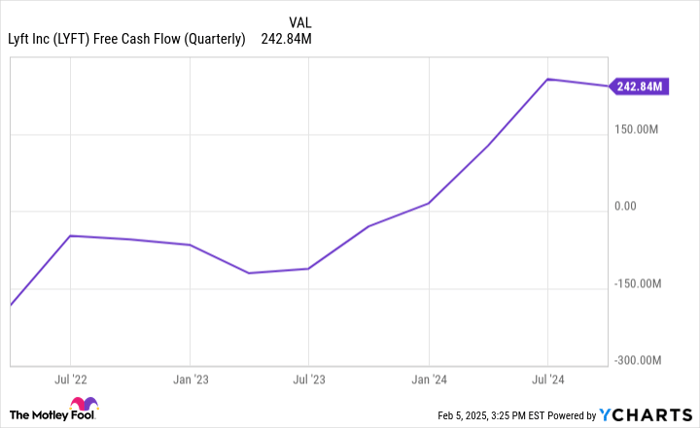

Those are good underlying business trends. But Lyft's financials are also trending in a positive direction. CEO David Risher took over in April 2023. The chart clearly shows that something happened around that time.

LYFT Free Cash Flow (Quarterly) data by YCharts

As is evident from the chart, Lyft's new CEO was serious about free cash flow, and the company quickly improved. Today, it's free cash flow positive for the first time in its history.

To recap, adoption levels for Lyft's business are encouraging, it's growing, and it's now also profitable under new management. These things provide a good start for a solid investment thesis.

Valuation

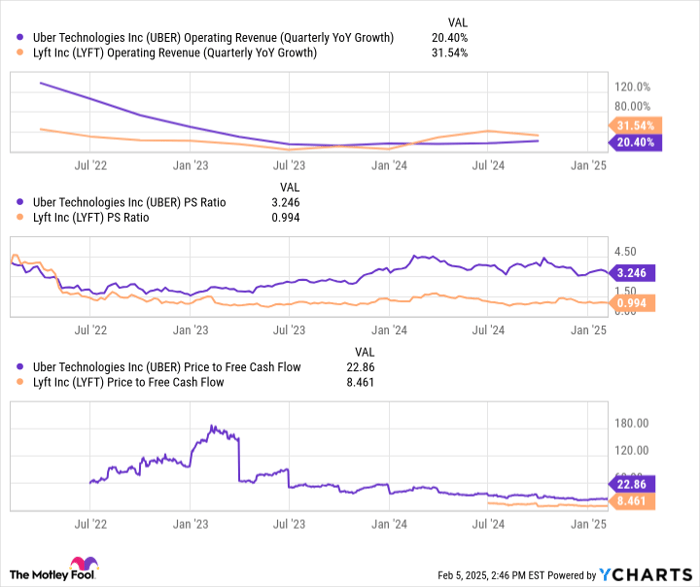

When it comes to valuation, Lyft looks like a screaming bargain. Compared to Uber, Lyft stock is valued more than 60% cheaper. This is true when measuring the price-to-sales (P/S) valuation as well as measuring the price-to-free cash flow valuation.

The kicker here is that Lyft's revenue is currently growing faster than Uber's revenue. Usually, the higher-growth business has the higher valuation. But as the chart shows, Lyft is both higher-growth and cheaper, which is a rare combination.

UBER Operating Revenue (Quarterly YoY Growth) data by YCharts

Consider this: If Lyft stock jumped 40% today -- in-line with price targets from analysts -- then it would still trade at a substantial discount to Uber stock. Therefore, one could make the case that Lyft is worth significantly more today, just based on its trailing financial results. But things get truly interesting for investors when looking ahead to what's possible in the next few years.

The potential business improvement ahead

Lyft is looking to do several things over the next few years. But the one I want to mention is digital advertising. It's only just getting started now, but the company believes this could be a $400 million business in 2027. And this isn't outrageous, in my opinion. Consider that Uber hit a $1 billion run rate for digital advertising less than two years after launching.

Granted, Uber is much larger than Lyft, so it's unreasonable to expect Lyft to scale that big, that fast. But I believe that it can indeed scale to $400 million over a three-year period. For perspective, this advertising revenue target works out to about $4 quarterly per active rider -- it's not a guaranteed outcome, but it's certainly attainable.

The point is that digital advertising could be a huge growth driver for Lyft in the coming years, and this revenue stream is high margin. This could lift Lyft's free cash flow even higher. And in fact, management is targeting free cash flow of $900 million in 2027, which is 40% higher than its trailing-12-month free cash flow as of Q3.

Compared to Uber, Lyft is significantly undervalued today based on its trailing numbers. But over the next few years, management is eyeing meaningful growth, meaning the stock is even more attractive on a forward basis. Therefore, I believe Lyft stock is a resounding buy today.

Should you invest $1,000 in Lyft right now?

Before you buy stock in Lyft, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Lyft wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $788,619!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 7, 2025

Jon Quast has positions in Lyft. The Motley Fool has positions in and recommends Uber Technologies. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.