Just Graduated? Time to Plan for Retirement

It’s never too early to start saving for retirement. Now that you're getting paychecks from your brand-new job, this is a prime time to start saving, because once those paychecks stop rolling in, you’re still going to need money to live comfortably and do the things that you love.

But how do you begin to save for retirement? What is a 401(k), anyway? And how do I know I'm picking the right plan? Before we answer those questions, it's important to note one thing: the sooner you start saving for retirement, the better. When you're starting out and money is tight, it can be tempting to hold off on contributing to retirement when every penny counts, and you need cash for bills, groceries, and other essentials. After all, that's real money that you can put to use right now, right?

But here's the thing -- you could be costing yourself significant sums of money down the line, due to what's known as compound interest. It is absolutely worth finding a way to save money for retirement; your older self will thank you. If you want more information on why compound interest is so powerful, check out this short video by TD Ameritrade.

Ok, now we've gotten that out of the way, let's get into how you can save for retirement.

Where to Start

One of the first things to think about is opening a savings account specifically for your retirement savings. As we mentioned in our article, Checking and Savings Account: How to Open a Bank Account, college graduates will vastly benefit by possessing a savings account. Contributing extra cash or portions of your income to a savings account will only help you down the line.

Types of Retirement Plans

Depending on where you’re employed, different retirement plans may be accessible to you. We’ll break down some of the most common retirement plans, but keep in mind that you may have access to plans more suitable for your personal circumstances.

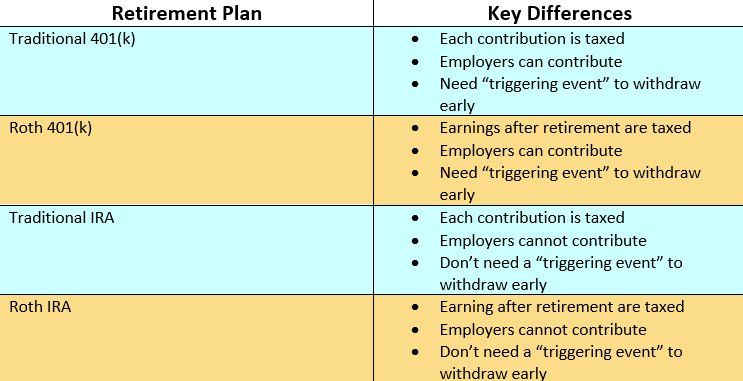

What Is a 401(K)?

The 401k plan is considered to be the most popular employer-sponsored retirement plan in the U.S.. Essentially, employers offer this type of retirement plan so that portions of your paycheck will go directly into your retirement account. In a traditional 401(k), a percentage of each contribution you make will be taxed.

A Roth 401(k) will instead offer you the option to pay taxes on your account savings after you retire and allow your earnings to grow over the course of your career tax free. You must hold the IRA account for at least 5 years before you can make tax-free withdrawals. If you start saving now, this won’t be an issue.

The money that is being deposited into your 401(k) will be invested into mutual funds, which invest in a variety of securities like stocks and bonds. Earlier in your career, those 401(ks) will be invested in riskier investments like stocks, and later in your career your investments will divert to more passive investments like bonds.

Target-Date Funds (TDFs) are the most common types of 401(k)s. TDFs essentially invest your money up until a specific year, which is the year you plan on retiring. Your investments will adjust over the course of your career based on how close you are to retiring. A key characteristic of TDFs is their transition from investing your funds from risky investments like stocks, into more stable investments like bonds, the closer you get to retirement.

Once you’ve registered for a 401(k) plan with your employer, ask them if they match your contributions. Employers will usually match your contributions based on a percentage of your salary up to a certain limit. Think of this like a free raise -- if you contribute 6% of your paycheck to a 401(k) and they match up to 3%, for example, that is essentially free money for you.

You should note that by withdrawing money before you’re 59.5 years old, you’ll be charged an additional 10% more in income tax. There are exceptions to this called “triggering events.” Retirement, death of the participant (in which case, beneficiaries can withdraw), disability, experiencing certain hardships, or termination of the plan are valid reasons to withdraw money early.

401(k)s come with other perks as well. For starters, contributing to a 401(k) plan grants you eligibility for tax benefits. You can also take out loans from your 401(k) if needed, and interest is normally less expensive than if you chose to take out a loan with a bank.

Once you turn 72, the Internal Revenue Service (IRS) will require you to make “required minimum distributions,” or RMDs. This is a preventative measure that the IRS takes in case anyone tries to avoid paying taxes by leaving their money in their account.

What Is an IRA?

Individual Retirement Accounts are separate from employer contribution plans. You can withdraw funds from your IRA without penalty, or without the need for a “triggering event” to occur, which is useful in the event of an emergency; however, these withdrawals will be taxed and may even face another 10% tax if you haven’t yet reached 59 ½ years of age. Keep in mind that this account is meant to help you during retirement, so you should still try to refrain from using this money.

Unlike a typical IRA, a Roth IRA lets you grow your earnings tax-free over the course of your career, but you’ll have to pay taxes on these earnings after you officially retire. You will also be able to make any withdrawal without them being taxed after the age of 59 ½.

There are two key differences between a traditional 401(k) and a traditional IRA. Employers cannot contribute to an IRA. You will still be able to contribute portions of your income towards your retirement. Also note that an IRA does not tax your withdrawals once you retire. Although you will still have to make RMDs if you are still employed at age 72 and beyond.

Many people have a 401(k) and an IRA — you’re accumulating more savings over time this way. Lots of people choose to transfer their 401(k) balance over into their IRA so that their money continues to be invested.

Other Plans

If you employer doesn’t offer any retirements plans, suggest creating a plan for you and your organization. Some employers offer a variety of different retirement plans. Some common retirement plans include:

- Traditional pensions

- 403(b)

- Employee Stock Ownership Plans (ESOPs)

- Profit sharing

- 457 Plans

- Money Purchase Plans

- And more

For any retirement plan you decide to participate in, set up an automated payment so that you don’t have to think twice about how much you contribute to your plan.

Social Security

Over the course of your career, you are also paying taxes for Social Security. Social Security is meant to supplement your retirement savings by replacing a percentage of your pre-retirement income. This percentage is then calculated based on your highest 35 years of earnings to then act as a steady flow of income upon retirement. You have access to these benefits starting at age 62, but the longer you wait, the higher percentage you’ll receive in Social Security. The more you’ve managed to save in your retirement accounts will benefit you will the amount of income in Social Security you will receive.

Key Takeaways

The bottom line is that it’s vital to have a retirement plan and to enroll in one as soon as possible. The sooner you start saving, the better you are setting yourself up for financial stability in the long term. Remember to talk to your employer about getting a full employer match, set up automatic payments, and consider which plan will work best for you and your needs.

This is part of a bigger series that was designed to guide recent college graduates towards reaching their professional goals and benefiting from their studies. Check out our guide to post-graduate life to learn how to leverage your degree financially.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Retirement 401k Saving Money Personal Finance

Kristin Lasker

Kristin is a Digital Intern for the Summer of 2022. She's working on a series to help guide recent college graduates to financial success and independence, while working with Nasdaq's marketing team.

Read Kristin's Bio