The largest American lender, JPMorgan JPM, announced third-quarter results on Oct. 11, before the opening bell. The company’s top and bottom lines handily surpassed the Zacks Consensus Estimate.

Robust capital markets performance and a rise in net interest income or NII (driven by high interest rates, modest consumer spending and decent growth in loan balance) supported JPM’s quarterly performance. On the other hand, higher non-interest expenses and provisions and subdued mortgage banking performance were the headwinds.

Since the results were announced, shares of JPMorgan have gained more than 5%.

A Quick Glance at JPM’s Q3 Performance

Net Interest Income (NII): Despite the 50-basis point interest rate cut by the Federal Reserve in September, the current relatively high interest rates are not conducive to a strong NII performance because of higher deposit/funding costs. Yet, JPM’s third-quarter NII numbers reveal a different picture. The metric grew 3% year over year to $23.41 billion. Further, management expects NII to be almost $22.9 billion in the fourth quarter and $92.5 billion in 2024.

Investment Banking (IB) Fees: In the third quarter, industry-wide IB business witnessed a solid trend reversal, and JPMorgan performed extremely well, continuing to lead on the global IB fees front. The company’s total IB fees (in its Commercial & Investment Banking or CIB division) were up 31% from the prior-year quarter to $2.27 billion. Specifically, equity underwriting fees jumped 26% and debt underwriting fees grew 56%. Further, advisory fees rose 10%. Management remains cautiously optimistic about the performance of the IB business going forward.

Markets Revenues: As trading volume and market volatility rose during the third quarter, JPMorgan benefited from the same. The company’s markets grew 8% to $7.2 billion. Specifically, fixed-income markets revenues were stable at $4.5 billion, while equity trading numbers jumped 27% to $2.6 billion. Though the trading business will likely normalize over time, the company is expected to keep performing well, driven by its scale and size.

Asset Quality: As the relatively high interest rates put pressure on consumer spending and macroeconomic factors weigh on borrowers, JPMorgan reported a significant surge in provision for credit losses for the third quarter to $3.11 billion. The company remains vigilant about the effects of continuous high rates and quantitative tightening on its loan portfolio.

Evaluating JPMorgan’s Investment Potential

Opportunistic Acquisitions: JPMorgan has been growing through on-bolt acquisitions, both domestic and global. In 2023, the company increased its stake in Brazil's C6 Bank to 46% from 40%, formed an alliance with Cleareye.ai (a financial technology firm focused on trade finance) and acquired Aumni.

Also, the company acquired the failed First Republic Bank. The deal continues to benefit JPM’s financials immensely and even helped it reach record profits last year. Additionally, in 2022, it acquired Renovite and a 49% stake in Greece-based Viva Wallet and Global Shares. These deals, along with several others, are expected to support the bank's plan to diversify revenues and expand the fee income product suite and consumer bank digitally.

Other Expansion Efforts: In February, the company announced plans to open more than 500 branches and renovate roughly 1,700 locations by 2027. As of Sept. 30, 2024, it had more than 4,900 branches across all 48 states in the United States. In contrast, its peers Wells Fargo WFC, Bank of America BAC and Citigroup C had 4,196, 3,741 and 641 branches, respectively, at the end of the third quarter.

JPMorgan actively seeks to expand its digital retail bank – Chase – across the European Union countries after launching it in the U.K. in 2021. The company is focused on bolstering its IB and asset management businesses in China.

Revival of Global Deal-Making Activities: JPMorgan continued to rank #1 for global IB fees despite industry-wide weakness in the business. Though the company’s total IB fees (in the CIB segment) plunged 59% in 2022 and 5% in 2023, the trend is reversing of late. In the first nine months of 2024, the company’s IB fees jumped 34% year over year, with a wallet share of 9.1%. The company is likely to witness growth in IB fees, driven by a healthy IB pipeline and active merger & acquisition market, and leverage its top position to gain further from the changed scenario.

Fortress Balance Sheet and Solid Liquidity: As of Sept. 30, 2024, JPM had a total debt worth $850.1 billion. The company's cash and due from banks and deposits with banks were $434.3 billion on the same date. The company maintains long-term issuer ratings A-/AA-/A1 ratings from Standard and Poor’s, Fitch Ratings and Moody’s Investors Service, respectively.

Hence, JPM continues to reward shareholders handsomely. After clearing the 2024 stress test, the company increased its quarterly dividend by 8.7% to $1.25 per share in September. In February, the company announced a 9.5% hike in quarterly dividends, which followed a 5% increase last year. In the last five years, it hiked dividends four times, with an annualized growth rate of 5.09%. Currently, the company's payout ratio is 26% of earnings.

Dividend Yield

Image Source: Zacks Investment Research

The company also authorized a new share repurchase program, effective July 1. Management expects the pace of share buybacks to be modest in 2024 after having repurchased shares worth almost $9.9 billion in 2023.

Interest Rate Cuts: A Short-Term Bane for JPMorgan

During the Sept. 17-18 FOMC meeting, the central bank indicated two more rate cuts this year and four in 2025. This is expected to bring the rates down to 3.4% by the end of next year.

While lower rates would lessen deposit repricing pressure, it would also mean lower interest income. This is expected to hurt JPM’s NII.

On the third quarter conference call, Jeremy Barnum, the company’s chief financial officer, noted that NII-excluding Markets is expected to witness sequential declines and reach a trough by mid-2025. Thereafter, the metric is likely to grow sequentially and reach almost $87 billion by the end of next year.

Nonetheless, JPMorgan’s long-term NII growth prospects remain intact.

What Should Investors Do With JPM Stock?

Shares of JPMorgan have been performing remarkably. So far this year, the stock has surged 31.7%, handily outperforming the industry and the S&P 500 Index. Further, the stock has outperformed its peers – BAC, C and WFC – in the same time frame.

Year-to-Date Price Performance

Image Source: Zacks Investment Research

Given the rally in JPM shares this year, the company is currently trading at a premium with forward 12-month earnings multiple of 13.24X compared with the industry’s 11.94X, indicating a stretched valuation.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for JPM’s 2024 earnings implies an 8% growth year over year, while 2025 earnings indicate a 4.2% fall because of weakness in NII performance and higher non-interest expense. Management anticipates adjusted non-interest expenses to rise to more than $94 billion next year. In 2024, the metric is expected to be approximately $91.5 billion.

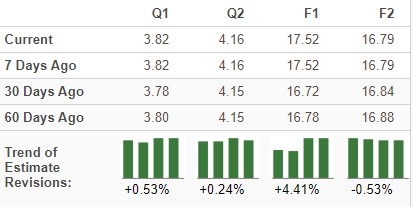

Earnings Estimates

Image Source: Zacks Investment Research

Find the latest earnings estimates and surprises on Zacks Earnings Calendar

JPMorgan’s leadership position in several businesses and strategic plan to expand its footprint globally gives it an edge over its peers. Its focus on building a solid deposit franchise and bolstering its loan book positions it well for future growth.

Yet, investors must take into consideration JPM stock’s high valuation and bearish analyst stance for 2025. They must watch for the NII trajectory and how future interest rate cuts impact the metric.

So, investors should consider these factors carefully and evaluate their risk tolerance before buying the JPM stock. Those who already own the stock can hold on to it because it is less likely to disappoint over the long term.

JPM currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is among the most innovative financial firms. With a fast-growing customer base (already 50+ million) and a diverse set of cutting edge solutions, this stock is poised for big gains. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpBank of America Corporation (BAC) : Free Stock Analysis Report

Wells Fargo & Company (WFC) : Free Stock Analysis Report

JPMorgan Chase & Co. (JPM) : Free Stock Analysis Report

Citigroup Inc. (C) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.