JPMorgan JPM is in discussions with Apple Inc. AAPL regarding a credit card partnership to replace Goldman Sachs GS. This was first reported by Wall Street Journal, citing a source familiar with the matter.

What Led to JPM’s Negotiations?

In 2019, Goldman partnered with Apple as it entered into the credit card space to issue Apple credit cards. However, it began pulling back last year due to significant losses in its consumer division.

In early 2023, GS informed Apple of its intention to offload the partnership due to financial strains and in November, Apple reportedly proposed an exit from its credit card contract within the next 12 to 15 months. This paved the way for potential new partners to take over the Apple credit card program.

In December 2023, JPM was reportedly being considered a natural successor to take over the Apple credit card program given the existing relationship between the two entities. The two entities already had ties via Apple Pay, and JPMorgan was one of the largest partners for transactions at Apple retail outlets.

Earlier this year, AAPL and JPMorgan initiated discussions to consider the possibility of the bank becoming the new issuer of the Apple Card.

JPMorgan’s Current Status in Negotiations

As reported by Wall Street Journal, the discussions have advanced in recent weeks, However, there’s no certainty that an agreement will be formed.

JPM is negotiating for better terms, as it seeks to pay less than the full value for roughly $17 billion outstanding balances in the Apple Card program due to higher losses on the cards. Sources close to Goldman contended that higher-than-average delinquencies and defaults on the Apple Card portfolio were majorly owed to the new user accounts.

Apple and Goldman offered cards to customers with weak credit scores in an attempt to boost their revenues, which resulted in increased subprime exposure and terms that could be costly for any issuer. This has further complicated the negotiations.

Also, JPM is in talks regarding amendments to some parts of the program, which includes Apple’s calendar-based billing feature, which means that cardholders receive statements at the beginning of the month instead of staggered ones dispersed across the period. This feature, while appealing to customers, leads to a huge number of calls for the service personnel at the same time each month.

These efforts align with JPM’s aim to grow its presence in diverse sectors and strengthen its market share. Last week, it was reported that the company seeks to increase its corporate banking presence in the Swiss markets by utilizing its blockchain technology. It is currently in discussions with potential clients in Switzerland as the bank projects significant growth in its Swiss corporate banking division over the next three to five years. Similarly, earlier this month, JPM set up a private banking team in Dubai to offer wealth management services. This July, the company stated that it aims to capture 15% of the nation’s consumer deposits.

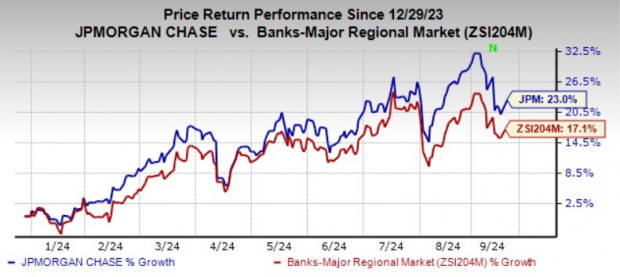

JPM’s Zacks Rank & Price Performance

Year to date, shares of JPMorgan have gained 23% compared with the industry’s 17.1% growth.

Image Source: Zacks Investment Research

Currently, JPM carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>The Goldman Sachs Group, Inc. (GS) : Free Stock Analysis Report

JPMorgan Chase & Co. (JPM) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.