JD.com, Inc. JD is slated to report third-quarter 2024 results on Nov. 14.

For the third quarter, the Zacks Consensus Estimate for revenues is pegged at $36.54 billion, indicating growth of 7.64% from the year-ago quarter’s reported figure.

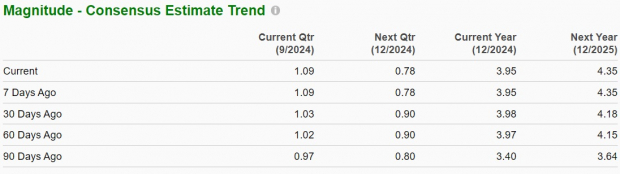

The consensus mark for earnings is pinned at $1.09 per share, suggesting 18.48% growth from the prior-year quarter’s reported number. The figure has been revised 5.8% upward over the past 30 days.

Image Source: Zacks Investment Research

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

JD.com has an impressive earnings surprise history. In the last reported quarter, the company delivered an earnings surprise of 50%. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 24.04%.

JD.com, Inc. Price and EPS Surprise

JD.com, Inc. price-eps-surprise | JD.com, Inc. Quote

Earnings Whispers

Our proven model does not conclusively predict an earnings beat for JD.com this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

JD has an Earnings ESP of 0.00% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping Upcoming Results

JD.com's third-quarter results are anticipated to be driven primarily by robust performance in its core JD Retail segment, underpinned by diverse product offerings across electronics, home appliances and general merchandise.

The company's strategic expansion of third-party merchant relationships, particularly in premium international brands, is expected to have enhanced marketplace engagement. Notable among these partnerships is the collaboration with French luxury fashion group SMCP, whose brands SANDRO, MAJE, and CLAUDIE PIERLOT have established flagship stores on the platform, potentially strengthening the luxury retail segment.

The company's omnichannel strategy appears to be gaining traction, supported by its partnership with Dada, which provides access to major chain retailers and FMCG brands. This is complemented by growing momentum in physical retail through 7FRESH and JD MALL, while the JD Procurement and Sales Manager Livestreaming initiative is likely to have contributed to enhanced customer engagement. Additionally, JD Health's digital capabilities, including 24/7 free online medical consultations and pharmacy services, are expected to have positively impacted the quarter's performance.

JD Logistics continues to be a key growth driver, leveraging an expanding network of domestic and overseas warehouses. The company's focus on quick delivery services and strengthened logistics infrastructure in lower-tier cities might have helped penetrate these markets more effectively.

However, these positive factors are likely to be partially offset by challenges in the new business segment and increased fulfillment expenses, including procurement, warehousing, delivery, customer service and payment processing costs, which might have weighed on margins in the third quarter.

Price Performance & Valuation

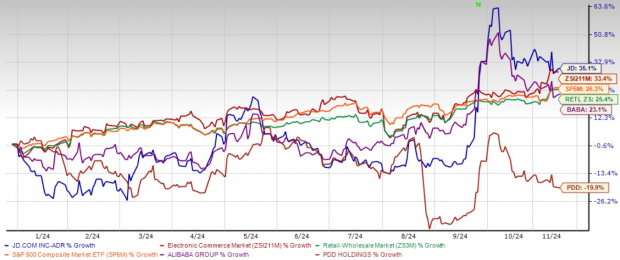

JD.com shares have returned 35.1% on a year-to-date basis against the industry, the Zacks Retail-Wholesale sector and the S&P 500 index’s return of 33.4%, 35.4% and 26.3%, respectively.

JD has also outperformed its peers — Alibaba BABA and PDD Holdings PDD. While BABA has gained 23.1%, PDD has lost 19.9% year to date.

YTD chart

Image Source: Zacks Investment Research

Now, let us look at the value that JD.com offers to its investors at current levels.

Currently, JD is trading at a discount with a forward 12-month P/E of 9.09X compared with the industry’s 25.36X, reflecting a good investment opportunity.

JD’s P/E F12M Ratio Depicts Discounted Valuation

Image Source: Zacks Investment Research

Investment Thesis

JD.com approaches third-quarter 2024 earnings with mixed indicators across its business segments. The company's core retail division demonstrates resilience through its diversified product categories and strategic partnerships, particularly in luxury retail with SMCP brands. Its logistics network expansion and healthcare services evolution signal continued operational development, while investments in lower-tier city infrastructure could unlock new growth opportunities. However, these expansion efforts, coupled with rising fulfillment expenses and challenges in new business segments, present a balanced equation of growth potential and cost pressures. The company's performance will likely reflect both these opportunities and operational challenges in an evolving Chinese e-commerce landscape.

Conclusion

Given the combination of risks and rewards, existing shareholders are advised to hold their positions, whereas prospective investors should closely monitor the company’s key developments instead of rushing in to buy the stock.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2024. While not all picks can be winners, previous recommendations have soared +143.0%, +175.9%, +498.3% and +673.0%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>JD.com, Inc. (JD) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

PDD Holdings Inc. Sponsored ADR (PDD) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.