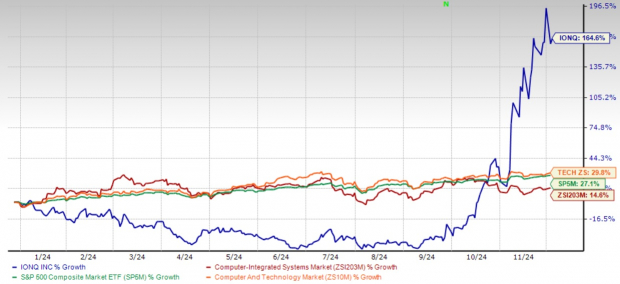

Despite IonQ's IONQ impressive 164.6% year-to-date rally, outperforming the Zacks Computer and Technology sector’s return of 29.8%, mounting concerns about the quantum computing company's financial sustainability and valuation suggest investors should consider taking profits. While the company's recent third-quarter results showed promising revenue growth, reaching $12.4 million and exceeding guidance, deeper analysis reveals concerning fundamentals that could spell trouble ahead. The company's net loss widened to $52.5 million in third-quarter 2024 compared with a loss of $44.8 million in the prior-year period, highlighting persistent profitability challenges.

Year-to-date Performance

Image Source: Zacks Investment Research

Escalating Operational Costs Raise Red Flags

While management celebrates booking $63.5 million in new contracts, including a significant $54.5 million deal with the U.S. Air Force Research Lab, the mounting operational expenses raise red flags. Operating costs surged 36% year over year to $65.5 million, with research and development expenses alone jumping 35% to $33.2 million. Despite holding $382.8 million in cash and investments, the adjusted EBITDA loss of $23.7 million for the quarter suggests a concerning cash burn rate that could pressure future operations.

Ambitious Expansion Plans vs. Financial Reality

IonQ's recent moves into quantum networking through the planned acquisition of Qubitekk and partnerships with companies like AstraZeneca and Ansys appear promising on the surface. However, these initiatives require substantial capital investment at a time when the company is already burning through cash. The company's aggressive expansion strategy, including new partnerships with NKT Photonics and imec for developing next-generation laser systems and photonic integrated circuits, adds to the financial burden. While these investments might pay off in the long term, they represent significant near-term risks in an industry that's still largely experimental.

IONQ's Intensifying Competitive Threats

Despite IonQ's trapped-ion technology claims, the company faces daunting competition from deep-pocketed tech giants like International Business Machines IBM, Alphabet GOOGL-owned Google and Microsoft MSFT, who are pouring billions into quantum computing development. While the Qubitekk acquisition may strengthen its networking position, IonQ's relatively limited resources compared to competitors could hinder its ability to maintain technological leadership. The emergence of well-funded Chinese players like Baidu and increasing investments from Amazon and Rigetti Computing further threaten IonQ's market position, potentially squeezing its growth prospects in this rapidly evolving industry.

Valuation Concerns and Dilution Risks

Adding to the concerns, IonQ's stock valuation appears stretched given its current financial metrics. The stock's current price-to-sales (P/S) ratio is significantly higher than the industry average, indicating a stretched valuation. This leaves little room for error and makes the stock particularly vulnerable to any negative developments or earnings misses. IONQ stock is trading at a one-year premium with a forward 12-month price/sales of 92.06 compared with the Zacks Computer - Integrated Systems industry’s 3.23.

IONQ’s P/S F12M Ratio Depicts Stretched Valuation

Image Source: Zacks Investment Research

While the company projects full-year 2024 revenues between $38.5 million and $42.5 million, this guidance pales in comparison to its market capitalization. The substantial increase in stock-based compensation, which rose to $24.6 million in the third quarter from $17 million in the prior year, raises questions about shareholder dilution. This growing expense, combined with the company's ambitious growth plans and persistent losses, could put additional pressure on the stock price.

Uncertain Commercialization Timeline

The quantum computing industry remains in its infancy and commercialization timelines could be longer than expected. Despite management's confidence in their bookings target of $75-$95 million for 2024, the "lumpiness" in bookings acknowledged by CFO Thomas Kramer adds uncertainty to future revenue recognition.

The Zacks Consensus Estimate for 2024 is pegged at $40.5 million, indicating year-over-year growth of 83.74%. The consensus mark for 2024 earnings is pegged at a loss of 86 cents per share. The earnings estimates have moved wider by 2 cents per share over the past 30 days, indicating caution.

Image Source: Zacks Investment Research

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

Investment Conclusion

For investors sitting on substantial gains from IonQ's remarkable year-to-date rally, the combination of widening losses, aggressive spending, rich valuation and industry uncertainty suggests now might be an opportune time to take profits. While quantum computing holds enormous potential, the path to profitability remains unclear, and the stock's current valuation leaves little margin of safety for investors. Given these factors, prudent investors might consider reducing their exposure to IONQ and waiting for more concrete signs of sustainable profitability and clearer commercialization timelines before re-entering positions at potentially more attractive valuations. IONQ stock currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is among the most innovative financial firms. With a fast-growing customer base (already 50+ million) and a diverse set of cutting edge solutions, this stock is poised for big gains. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpMicrosoft Corporation (MSFT) : Free Stock Analysis Report

International Business Machines Corporation (IBM) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

IonQ, Inc. (IONQ) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.