Credit: Shutterstock photo

Credit: Shutterstock photoBy Lincoln Li :

When the environment changes, even the best functioning system may need to be abandoned.

Executive Summary

Hong Kong (( HK )) adopted the Linked Exchange Rate system in 1983, and it has been operating successfully for more than three decades. However, the maintenance costs of the system have become huge and they might outpace the exit costs, especially under the combined influence of a slowdown of the Chinese economy and an interest rate hike in the U.S. Compared with the Asian Financial Crisis in 1997, the HK government owns much larger foreign reserves at present than it did then. The HK government is also facing a much more severe populist political environment and the anger of low-income residents towards wealth inequality. The anger of low-income residents could be "the last straw that breaks the camel's back" in terms of the HK government maintaining the Currency Board System. At present, the cost of exiting the Linked Exchange Rate system is small, thanks to capital inflows from Mainland China. However, the time horizon for the existence of such a good exit opportunity is short. There are two ways in which investors can speculate on an exit from the Currency Board System, but political reasons weigh the most heavily. If investors speculate on a de-pegging strategy at present and bet on a strengthening HKD, their actions are "politically correct," and they might receive less hostility or even acquiescence from the HK government. Consequently, investors have a much greater chance of success compared to adopting a "double down" strategy to capitalize on the HKD depreciating when the Chinese economy experiences a hard landing.

Background to Hong Kong Adopting the Current Linked Exchange Rate System

Hong Kong adopted its current Linked Exchange Rate system in 1983 after an "unfavorable" discussion between Margaret Thatcher and Deng Xiaoping concerning the proposal that the British government continue to manage HK after 1997. The concern over the ruling on the part of the Chinese Communist Party drove capital out of HK and the Chinese government's threat to take over HK before 1997 exacerbated the trend. Prior to 1983, the HK government adopted a floating exchange rate system, and as it lacked a central bank, the HKD depreciated quickly against the USD and inflation skyrocketed. In order to control inflation and restore discipline in the financial system within a short period of time, the HK government adopted the Linked Exchange Rate system. In essence, this is a Currency Board System, [1] and at the same time, the HK government announced it had pegged the HKD to the USD at 7.80. At the time, there were few alternative options and there was an urgent time frame. [2]

The system operated successfully for 30 years and it was resilient to several financial crises including the Asian Financial Crisis in 1997 and the more recent global financial crisis in 2008. The HK government claims its currency arrangements are the cornerstone of HK's prosperous economy and it argues that as a small open economy, the Currency Board System is the best choice for Hong Kong. Although the Currency Board System has contributed greatly to the prosperity of HK's economy in the past, precisely as has been claimed, when the environment changes, even the best functioning system may reveal weaknesses and the system may face the fate of abandonment. This is highly likely to apply to HK's Currency Board System. In the next section, the arguments why the Hong Kong Monetary Authority (HKMA) should maintain the current system are examined and an assessment is made as to whether these arguments are still valid.

The HKMA claim that"the Linked Exchange Rate (LER) remains the best monetary option for Hong Kong and no other monetary policy would provide the stability and confidence necessary for an extremely open and externally oriented economy like Hong Kong."[3]

In its introductory document to the existing currency system, the HKMA acknowledges the weakness of the LER, but argues that the LER is still the best choice for HK after comparing it to alternative options including dollarization, free float, link to a basket of currencies, link to another currency, and link to the U.S. dollar, but at another rate. [4] Although the HKMA's argument has some merit, it does not discuss the option of adopting the monitoring band mechanism which has been adopted by Singapore, another highly successfully small and open economy in Asia. It is relevant that there are several research papers which show that adopting a monitoring band system would be an even better option for HK.

Professors Rajan and Siregar argue that Singapore's monitoring band system is more flexible and that it has "outperformed" HK's Currency Board System overall. The advantage of Singapore's system was more obvious in the 1990s when a series of external shocks hit the region and impacted both economies. They point out that when an economy is faced with a sharp external shock, it may require some degree of discretion to mitigate the effects of these shocks. The required internal adjustments are extremely costly and therefore they are not always forthcoming. The Currency Board System is a severe liability to HK because a failure to undertake the necessary adjustments will lead to loss of price competitiveness in international markets and a build-up of imbalances. This also encourages markets to test the durability of the peg which only exacerbates the problems. On the other hand, if the monetary authority adopts discretionary monetary policy, it would undermine the credibility and concomitant benefits of the hard peg. Hong Kong pursued such a discretionary policy in the 1990s, resulting in a sustained attack on the Hong Kong dollar in the midst of the crisis. [5]

Professors Tse and Yip's research on interest rate behavior in two economies also shows that the monitoring band system in Singapore not only allows a greater flexibility in the choice of the exchange rate, but also a greater autonomy in the choice of interest rates to mitigate a crisis, recession or overheating. The loopholes and de-pegging risks of the currency board might imply a substantial exchange-rate risk for banks when conducting uncovered interest arbitrage. As a result, during the previous crisis period, banks refrained from performing arbitrage, despite the emergence of a huge interest rate differential between HK and the U.S. during the crisis period. [6]

HKMA also claimed "structure of Hong Kong economy is flexible and responsive. Markets such as the labor market, property and retail markets respond quickly to changing circumstances: this flexibility facilitates adjustments in internal prices and costs, which in turn bring about adjustments to external competitiveness without the necessity of moving the exchange rate."[7]

However, such assumption might also not be true. Professor Yip suggests that, in fact, HK's (export) price was far more sluggish than that presumed by the proponents of HK's Currency Board System. Through research, he found that the long-perceived high flexibility in HK was in fact due to a high adjustment speed in quantity, not price. The adjustment in quantity implies a large adjustment cost in maintaining the peg in HK. This also explained why the volatility of HK's quantity (such as real GDP or export-volume) was unusually large by international standards. Yip found that prior to the 1997 Asian Financial Crisis, HK had experienced years of inflation and the fixed exchange rate had pushed its prices and wages to extremely high levels. Therefore, even HK experienced more than five years of deflation, although the accumulated fall in prices and wages during the post-crisis recession is still small when compared with the accumulated rise during the 7-8 years of asset inflation before late-1997. Yip's research suggests that the accumulated rise in HK's Consumer Price Index (( CPI )) between January 1990 and December 2003 is still substantially higher than that of the U.S. and indicated that there could still be plenty of downside for HK's prices and wages. [8]

The sluggishness associated with adjusting wages and prices might be even worse at present compared to the last decade. The gap between the rich and poor of HK is among the widest in the world, and the problem is only getting worse. Monthly median earnings have only increased by 30% over the last 10 years while Hong Kong's GDP has jumped 60%. [9] Low-income residents are becoming angrier about the growing inequality of wealth and populist political sentiment makes it harder to make necessary wage and price adjustments. A good example is that HK dock workers organized a strike against Hutchison Whampoa Group (HUWHY) and asked for a 23% pay increase which finally ended up being a 9.8% pay rise backdated to 2013. [10] It is unimaginable that low-income workers will accept pay cuts or high unemployment when another crisis breaks out. It is this social and political pressure that could be "the last straw that breaks the camel's back" in terms of the HK government maintaining the Currency Board System. However, if the HK government can come to terms with such a bad outcome and decide to act prior to the worst finally happening, such factors could, in essence, become the biggest drivers for the HK government changing the system promptly in order to make HK the force it once used to be.

The Worst Scenario

As monetary policies among the major central banks diverge and the Chinese economy is slowing down, the HKMA recently conducted research on the "worst case" scenario and it has been endeavoring to determine the combined impact.

As Hong Kong has adopted the Currency Board System, U.S. monetary policy mainly affects interest rate-sensitive sectors. Quantitative easing (QE) by the European Central Bank (ECB) and the Bank of Japan (BoJ) reinforces appreciation pressures on the HKD. On the other hand, it also somewhat neutralizes capital outflows caused by a tightening in U.S. monetary policy. The divergence of major central bank policies has caused the growth in real GDP to slow down and the unemployment rate to go up. However, real variables such as real GDP growth and the unemployment rate are more sensitive to the economic slowdown in Mainland China. With shocks emanating from the slowdown in the Mainland, the growth in real GDP falls further and unemployment rises by more. [11] Although the HKMA's research suggests that the current financial system can again sustain such shocks, it would be the social and political pressures that lead to the exit from the Currency Board System.

Exit Timing

Just as Professors Rajan and Siregar point out, the orchestration of an exit from the Currency Board System is a difficult maneuver which could be destabilizing, especially considering that HK authorities have invested a great deal of resources in rebuilding confidence in the currency board arrangements following the regional financial crisis. Although the maintenance costs might outpace the exit costs, one cannot be sure if the end game is necessarily worth it. [12]

Professor Yip suggests that although the exit cost is unknown, a stronger currency can mitigate the cost. He argues that if the U.S. dollar enters a period of substantial depreciation and if the HK dollar is unpegged at this point, then the exit costs will be very small (or even negative) with the dollar up against USD-related currencies and relatively stable against other currencies. [13]

At present although the timing of an exit from the currency peg is not at its best, it is also not at its worst. Thanks to capital flows from Mainland China, the HK dollar is currently in a stronger zone.

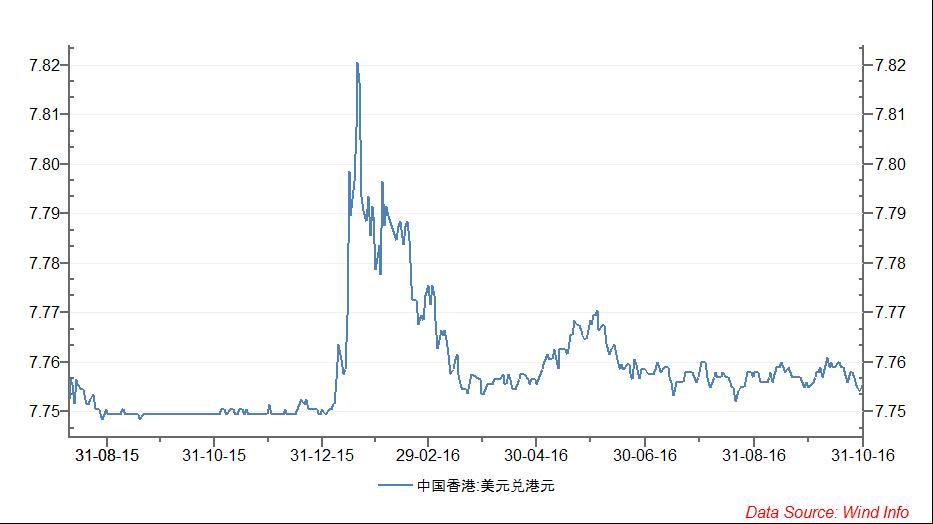

( U.S. Dollar (( USD )) to Hong Kong Dollar (HKD) )

In its half-year monetary and financial stability report, the HKMA suggests that after the PBOC depreciated the RMB against the USD last August, investors converted their offshore RMB into HKD. Consequently, strong-side Convertibility Undertakings [14] were being triggered repeatedly between 1 September and 30 October 2015. The strong inflow totaled HK$155.7 billion. [15]

[16]

Two Ways of Speculating on an Exit from the Currency Board System

1.Betting HKD to Depreciate

This strategy can be applied in the case where the HK government fails to de-peg the HKD when the currency is still strong, the economy slows down in China and there is an interest rate hike in the U.S. which finally pushes HK into recession and causes a huge drop in GDP and massive unemployment which triggers social unrest and attracts global investors' speculation as to an exit from the Currency Board System and a depreciation of the HKD.

Attached is the illustration of how investors applied a "double down" strategy back in 1997

Step 1: Preparation

Speculators borrowed substantial amounts of medium-term (6-12 months) HK dollars through the swap market or bought HK dollars forward in the forward market. In the stock futures market, they built up large short positions.

Step 2: Formal attack

Speculators sold their pre-funded HK dollars in the spot market. In order to maximize the impact of their attack, they sold the HK dollars in the relatively thin offshore markets. When the HKMA attempted to support the HK dollar through purchasing the HK dollar, interbank liquidity was squeezed which, in turn, caused a surge in the interbank rate. In addition, speculators also sold large amounts of HK dollars in the forward market. As banks usually did arbitrage between the swap market and the interbank market, the forward selling of HK dollars would also bid up HK's interbank rate and this would create a sentiment that the HK dollar was under attack, therefore attracting more speculators to follow.

Step 3: Profit taking

After bidding up the interbank rate and pushing down the spot and futures stock indices, speculators took their profits by closing the short positions in the stock futures market. They also bought back the shares and returned them to the custodian. In the foreign exchange market, they closed their short positions in forward HK dollars and lent out any surplus HK dollars (at a shorter maturity), previously borrowed from the swap market. [17]

However, this strategy might not be as effective now as at the time. During the attack in 1997, the HK government was predisposed to "positive non-interventionism" and it was not until the limit of tolerance had been breached that the government chose to fight back. Even so the HK government's intervention in the stock market still shocked and dismayed many observers on the grounds of principle. [18] After the financial crisis, the HK government implemented seven technical improvements to the system. The HKMA has already undertaken full preparation for a similar attack, and according to its report:

Betting on the HKD at the weak side has its pros and cons. One advantage is that the HK exchange rate can only move in one direction. The best strategy for the HK government might be to maintain the exchange rate at its legitimate weakest level at 7.85. The conclusion is that investors face literally no risks in betting in the wrong direction.

However, there are also several weaknesses of this strategy.

First, investors have to face the fact that the HK government owns huge foreign reserves, totaling HK$3,085.3 billion, which are also backed by the potential support of the Chinese government. The time horizon for the HK government to maintain the currency board might be much longer than investors expect.

Second, not to mention economic costs, it is politically unacceptable for the Chinese central government and the HK government to choose to exit the Currency Board System when the HKD is under depreciation attack. This is especially in view of the HK government having successfully weathered the Asian Financial Crisis in 1997 when the Chinese government had just taken over HK and had not implemented its policies.

Third, the HK economy will certainly suffer as the Chinese economy slows down, but such pain might be borne more in the long term. In the short term, the hit might not be as severe as investors have imagined. Commentators in the media always argue that the influence of Mainland China on the HK economy has become dominant, especially over the past decade, as trade and financial linkages have become increasingly tighter. The headline trade figures suggest that the share of Hong Kong's merchandise and services exports to the Mainland increased to 51% in 2012 while the U.S. share declined to 21% compared to a much larger share from a decade ago. However, He, Liao, and Wu suggest that the headline figures are only informative about export destinations, rather than the origin of final demand for exports. Their research shows that the share of merchandise exports to the Mainland in value-added terms was about 22% in 2012. The U.S. share, though having declined from a decade ago, was still around 25% in 2012.

It is interesting that in contrast to the general misconception that the demand for financial services in HK is largely Mainland-driven, within the category of HK's exported financial services, U.S. demand accounted for 33% of the total in 2012, whereas the Mainland's share was merely 4%. They suggest that the U.S. transitory shocks have remained a dominant force in driving HK's business cycle fluctuations, and that transitory shocks from Mainland China have played a less important role. However, when it comes to permanent shocks, the picture is the opposite: permanent shocks from the Mainland have a greater impact on the volatility of HK's trend output than those from the U.S. [20] At the same time, investors are concerned about the quality of HK's banking assets and their exposure to the Mainland. However, the HKMA's report suggests that HK banking has limited direct Mainland exposure. During the last six months, the classified loan ratio of Mainland-related lending rose to 0.94% from 0.78%. [21] As a result, it might take a relatively long period of time to see the impact of the economic slowdown in China transmit to Hong Kong and drive up local non-performing loans (NPLs).

In summary, it is not easy to replicate a double-down strategy and gamble on the HKD depreciating. Gambling on a weaker HKD would not only attract the HK and Chinese government's intervention, but speculators also have to face the fact that HK might be able to withstand the economic slowdown in China for a much longer period of time than investors expect. At the same time, if investors' gamble on such a strategy, there exists the possibility they will not earn profits and it is also possible that it will cause pain to the HK government which is a lose-lose result for both parties. On the other hand, there is no need for investors to confront the HK government. If investors speculate in the right direction, they might be able to earn profits and reach a win-win result with the government.

2.Betting on the HKD to strengthen

As the slowing Chinese economy puts the RMB under pressure, investors are transferring their wealth into HK to hedge the depreciating RMB. In the near term, there is an opportunity for investors to speculate on the HKD strengthening and thus the HKMA can take advantage of this opportunity and exit the Currency Board System.

Like with betting on the HKD depreciating, there are also several pros and cons in making such a bet. The biggest advantage is that it is "politically correct". The HK government used to be much more tolerant when the HKD was in its stronger zone which indicates a well-performed economy. It was not until 2005 that the HKMA implemented the Convertibility Undertaking ((CU)) and formally made it clear that a strong HKD would not breach the Currency Board System. If the HK government expects that there is a strong possibility of massive unemployment due to the economic slowdown in China and an interest rate hike in the U.S., and decides to exit the Currency Board System before the worst time and when the HKD is still in its stronger zone, this can offer enough time for local businesses to adjust their operations and apply correlated capital structures to hedge FX risks and mitigate costs. [22]

Therefore when the crisis does eventually come, the HKMA can leverage the more flexible FX arrangements to reduce the negative impact. At present the HK government needs a good excuse to exit the Currency Board System. Investors are pushing up the HKD and combined with the chaotic global economic and political environment there appears to be a reasonable political excuse. The Chinese government also has to consider the possibility that the Chinese economy might experience a hard landing and its own huge foreign reserves might not be large enough to withstand the impact, not to mention supporting HK whose economic importance is continuing to decline. In addition, if the HK government chooses to exit the currency right now and make the HKD stay strong for a period of time, it seems such a decision is totally based on the HK government's own will and the exit is not so politically embarrassing. As a result, by speculating on a stronger HKD, investors are in essence helping the HKMA and they could encounter much less resistance or even acquiescence from both the HK government and the Chinese Central Government, which could, in turn, mean there is a much greater chance of success.

Weakness:

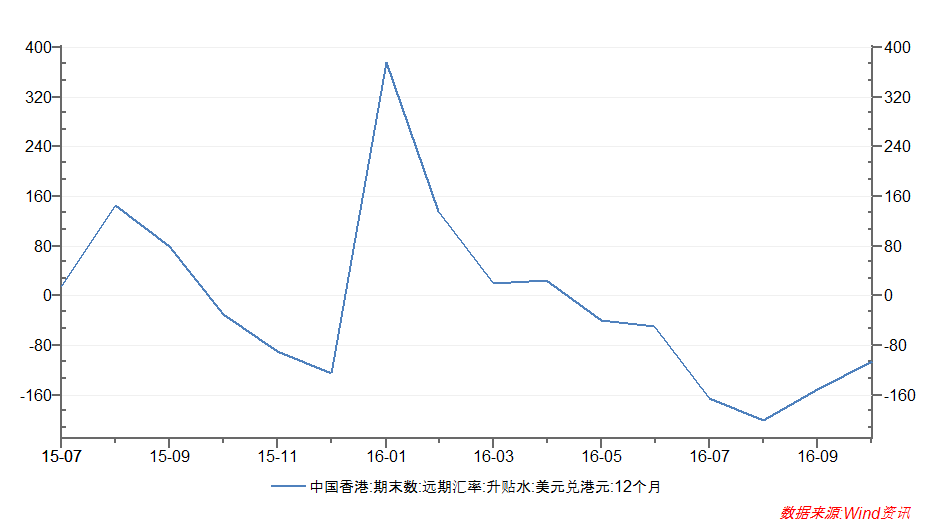

First, it's very possible that the Chinese government will fail to control housing prices and experience a sudden hard landing when the housing market collapses. Although previous research suggests that HK's economy would not suffer severely in the short term, the majority of investors might still adopt a double-down strategy and push the HKD into its weaker zone, just like what happened in January. However, at present such a risk does not appear to be high. The forward price and volatility of the HKD suggests that investors are still betting on the HKD to stay strong. However, this indicator could be misleading when betting on the HKD to continue to be strong after HK exits the Currency Board System. If the HKD is no longer pegged to the USD, HK might also suffer from capital outflows and the attitude of investors towards the HKD might change overnight.

Second, even though it is the best time for the HK government to exit the Currency Board System, it is still out of their comfort zone. The government might act too slowly and miss a good opportunity.

Third, betting on a stronger HKD needs a large number of investors to work together and their concerns over the Chinese economy might mean there are not enough participants to make the HK government feel comfortable with exiting the Currency Board System.

( Hong Kong Dollar 12 months Forward Discount. Source: Wind Info )

However, just as Professor Mishkin suggests:

The HK government is regarded as the best-functioning government in the world, even though it might act too slowly and miss this good opportunity. The exit decision is too complex and this report only tackles the question from one perspective. There are several other elements investors have to consider including the current political environment, the impact on different sectors and their political influences, the impact on the financial industry, the change of capital flows into Hong Kong, and especially how the HK government monitors these capital flows. Although the HKMA has revealed that it is monitoring several indicators, including spot exchange rates, aggregate balances, net spot foreign currency positions, and BOP and market survey data, its detailed models are still not clear. [24] Selerity would conduct further research into these topics in following reports.

Conclusion

The report suggests that the maintenance cost of the Currency Board System in HK has become too large and the government should exit the system and adopt Singapore's monitoring band currency system in preparation for a possible economic slowdown in China and an interest rate hike in the U.S. The growing number of angry low-income residents and the populist political environment might be the "the last straw that breaks the camel's back" to end the currency system. Compared to adopting a double-down strategy when the HKD is weak, investors could bet on a stronger HKD at present and speculate that the HK government will exit the system in the near future to mitigate the cost as capital flows from the Mainland can support the HKD. Such a strategy is "politically correct" and might have a greater chance of success.

[1]. Prof. Steve Hanke argues that the Hong Kong Government has "deviated from orthodoxy (Currency Board System) because they wanted the monetary authority to take on the features of a typical central bank." On Dollarization and Currency Boards: Error and Deception, Steve Hanke, Policy Reform, 2002, Vol. 5(4), pp. 203-222

[2]. Hong Kong's Money The History, Logic and operation of the Currency Peg, Tony Latter, Hong Kong University Press, pp.55

[3].HKMA Background Brief No.1 Hong Kong's Linked Exchange Rate System

[4]. Ibid.

[5].Choice of Exchange Rate Regime: Currency Board (Hong Kong) or Monitoring Band (Singapore)?, Ramkishen Rajan and Reza Siregar, IPS Working Papers

[6].Exchange-Rate Systems and Interest-Rate Behavior: The Experience of Hong Kong and Singapore, Y k Tse and Paul S l Yip, SMU Economics & Statistics Working Paper Series

[7].HKMA Background Brief No. 1 Hong Kong's Linked Exchange Rate System

[8].On the Maintenance Costs and Exit Costs of the Peg in Hong Kong, S. L. YIP, Economic Growth Centre Working Paper Series

[9].Hong Kong's growing wealth gap fuels protests, CNN

[10].Hong Kong dock workers end strike after pay deal, Financial Times

[11].The Impact Of U.S Monetary Policy And Other External Shocks On The Hong Kong Economy : A Factor-Augmented Var Approach, Hongyi Chen and Andrew Tsang, HKIMR Working Paper No.09/2016

[12].Choice of Exchange Rate Regime: Currency Board (Hong Kong) or Monitoring Band (Singapore)?, Ramkishen Rajan and Reza Siregar, IPS Working Papers

[13].On the Maintenance Costs and Exit Costs of the Peg in Hong Kong, S. L. YIP, Economic Growth Centre Working Paper Series

[15].Half-Yearly Monetary And Financial Stability Report March 2016

[17].The Impacts of Hong Kong's Currency Board Reforms on the Interbank MarketY.K. Tse Paul S.L. Yip Journal of Banking & Finance

Volume 27, Issue 12, December 2003, Pages 2273-2296

[18]. Hong Kong's Link to the U.S. dollar-Origin and Evolution, John Greenwood, Hong Kong University Press, pp. 279-280

[19].Half-Yearly Monetary And Financial Stability Report March 2016

[20].Hong Kong's Growth Synchronization with China and the U.S.: A Trend and Cycle Analysis, Dong He, Wei Liao, Tommy Wu, HKIMR Working Paper No.15/2014

[21].Developments in the Banking Sector, Hong Kong Monetary Authority Quarterly Bulletin June 2016

[22]. The Volatility Machine, Michael Pettis, Oxford Press, pp. 113-117

[23]. Monetary Policy Strategy, Frederic Mishkin, The MIT Press, pp. 456

See also Just Not Buying It on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}