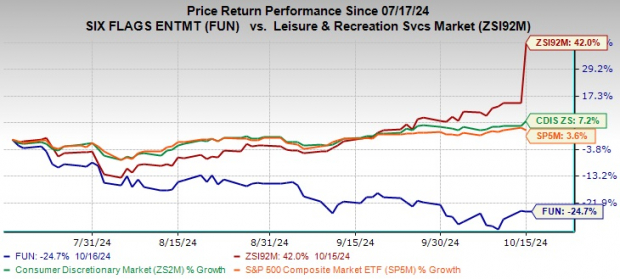

Six Flags Entertainment Corporation FUN has lost 24.7% in the past three months against the Zacks Leisure and Recreation Services industry’s 42% growth. The stock also underperformed the Zacks Consumer Discretionary sector and the S&P 500, which gained 7.2% and 3.6%, respectively, during the said time frame.

Image Source: Zacks Investment Research

The company’s growth trend is hurt by increased costs and expenses, along with a slowdown in consumer spending. The ongoing macro uncertainties and lingering inflationary risks are causing the downtrend.

The Zacks Consensus Estimate of the company’s 2024 earnings has trended downward in the past 30 days to $2.08 per share from $2.25. The estimated figure indicates a decline of 27% from the figure reported a year ago. The consensus estimate for the third quarter also moved south to $3.07 per share from $3.22 during the same time frame, indicating a 27.1% year-over-year decline.

Let us discuss why investors must stay away from the Zacks Rank #5 (Strong Sell) stock for now.

Factors Hurting FUN Stock

Soft Demand Patterns: Given the industry Six Flags operates in, it is subject to fluctuations in discretionary spending. The spending patterns vary between consumers based on several factors including income, macro trends and other related factors.

In the current economic scenario, the company is facing a slowdown in spending because consumers are moving toward non-discretionary spending and savings. Furthermore, the expectations regarding interest rate cuts contrast with reality, thus further subduing the consumers’ sentiments about their discretionary spending patterns. Considering the ongoing market challenges and lingering inflation, the company is expected to face a demand slowdown for some time.

Reduced Attendance: Dismal attendance is hurting the company’s performance. Six Flags saw a 2% drop in attendance during the second quarter of 2024 compared with the same period last year, which hurt overall revenues. This was attributed to fewer operating days in the second quarter and the earlier timing of the Easter holiday, which affected the number of visitors during peak periods. During the five weeks ended Aug. 4, 2024, attendance was 10.9 million, combining the entire company portfolio. This indicates a growth decline of 3% from the year-ago period.

High Costs & Expenses: Six Flags has been witnessing inflated costs and expenses for some time now, which have been hurting its bottom line and margins to some extent. One of the primary reasons for the increase in the company’s cost and expense structure is attributable to the $21.3 million of costs associated with the merger (between former Six Flags Entertainment and Cedar Fair, L.P.) that closed on July 1, 2024.

In the first six months of 2024, the company’s operating costs and expenses increased 11.1% year over year due to a $40.9 million increase in selling, general and administrative (SG&A) expenses, a $13.3 million increase in operating expenses and a $5.9 million increase in the cost of goods sold. The SG&A expenses increased due to costs associated with the merger, an increase in equity-based compensation plan expenses and the impact of the additional calendar week in the current period.

Key Picks

Here are some better-ranked stocks from the same sector space.

Atour Lifestyle Holdings Limited ATAT currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

ATAT has a trailing four-quarter earnings surprise of 9.1%, on average. The stock has gained 41.4% in the past year. The Zacks Consensus Estimate for ATAT’s 2024 sales and earnings per share (EPS) indicates growth of 49.5% and 32.6%, respectively, from the year-ago levels.

Norwegian Cruise Line Holdings Ltd. NCLH presently sports a Zacks Rank of 1. NCLH has a trailing four-quarter earnings surprise of 5.7%, on average. The stock has risen 60.5% in the past year.

The Zacks Consensus Estimate for NCLH’s 2024 sales and EPS indicates an increase of 9.9% and 127.1%, respectively, from the year-ago levels.

Flexsteel Industries, Inc. FLXS currently sports a Zacks Rank of 1. FLXS has a trailing four-quarter negative earnings surprise of 2.5%, on average. The stock has surged 110.5% in the past year.

The Zacks Consensus Estimate for FLXS’ fiscal 2025 sales and EPS indicates an increase of 3.6% and 42.2%, respectively, from the year-ago levels.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>Flexsteel Industries, Inc. (FLXS) : Free Stock Analysis Report

Six Flags Entertainment Corporation (FUN) : Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH) : Free Stock Analysis Report

Atour Lifestyle Holdings Limited Sponsored ADR (ATAT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.