Russell Rhoads, PhD, CFA

Associate Clinical Professor of Financial Management at the Kelley School of Business at Indiana University

This Wednesday brings us the first FOMC meeting with Kevin Warsh at the helm. It is likely markets will be braced for the outcome and statement. Traders will likely lean more toward the statement as the current derivative market odds show a 3.7% chance of a hike.

Our focus is the option market pricing before and after the announcement using 1-day options expiring on the close on FOMC day. The table below is a summary of Nasdaq-100 (NDX) index and at-the-money (ATM) option price behavior around the last twelve FOMC announcements.

Data Sources: Bloomberg and Author Calculations

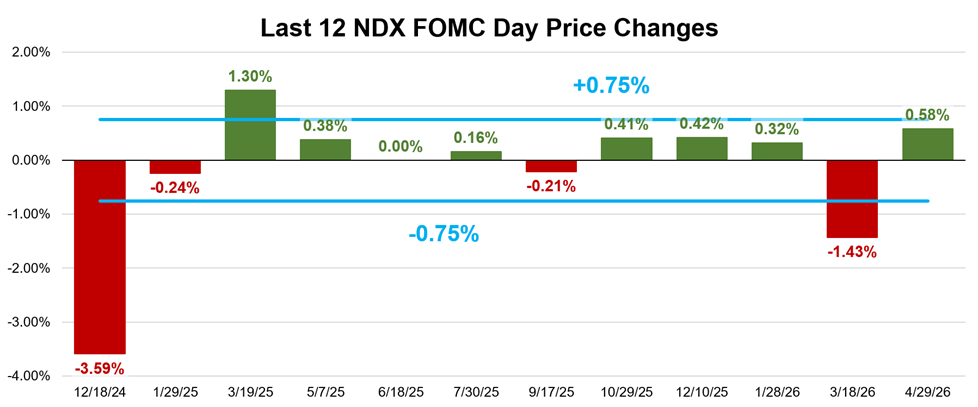

The average price change over the past twelve FOMC announcements is +/-0.75%. This figure has been trending lower. For example, the average reaction was closer to +/-1.00% in late 2025. Also, this figure is lower than the average NDX price change over all 1-day periods during the same period of +/-0.97%.

This less than average price change on FOMC days has resulted in the ATM straddle overpricing the last ten of twelve announcements. Finally, a consistent seller of the 1-day NDX ATM straddle would have a net profit of 450.04 points.

The chart below describes the last twelve NDX price changes on FOMC day. Note the most dramatic change is the one in the most distant past with NDX dropping 3.59% on December 18, 2024. A more recent downside outlier was in March 2026 with NDX losing 1.43%. Finally, the only upside outlier was in March 2025, with NDX gaining 1.30%.

Data Sources: Bloomberg and Author Calculations

A final look at FOMC history appears below with a depiction of the 1-day NDX ATM straddles the day before and at settlement on FOMC day. The December 2024 result is a large outlier below with the straddle priced at 187.40 the day before and settling at 790.69. That represents a loss of just over 600 points and serves as a warning that just because selling straddles has worked well lately, there is still danger of a large account depleting move accompanying FOMC day.

Data Sources: Bloomberg and Author Calculations

The other loss for ATM straddles occurred with the 1.43% loss for NDX on March 18, 2026, with the straddle underpricing that move by about 137 points. Recall, on the price change chart there were three outlier moves relative to the average move. The upside outlier, in March 2025 with NDX up by 1.30%, was still a small winner for a short ATM straddle by just under 15.00 points.

While recent history suggests that implied volatility has tended to overstate realized volatility on FOMC days, traders should remain mindful that infrequent but extreme market reactions can quickly offset a long string of profitable outcomes. The findings underscore the importance of disciplined risk management when employing short-volatility strategies around major economic events like FOMC announcements.

Russell Rhoads, PhD, CFA

Associate Clinical Professor of Financial Management at the Kelley School of Business at Indiana University

Latest articles

This data feed is not available at this time.

Data is currently not available