Equities Mixed as Retailers Lead Declines

- NASDAQ Composite +0.25% Dow -0.39% S&P 500 +0.02% Russell 2000 +0.12%

- NASDAQ Advancers: 1267 Decliners: 1008

- Today’s Volume (vs. Monday) +10.22%

- Crude -2.58% , Gold -0.03%

Market Movers

- October US Housing Starts 1.314M vs. consensus 1.320M

- October Building Permits 1.461M vs. consensus 1.385M

- In a meeting with Fed Chairman Jerome Powell, President Trump “protested” that interest rates were too high relative to other developed countries

Charlie’s Commentary

Stocks traded in a cautiously positive direction for most of the day yesterday after reversing from the morning's negative sentiment due to China’s pessimism over the US backing off on rolling back tariffs. What turned the tides was word that the White House would extend a license to allow US companies to do business with Chinese telecom company Huawei. The S&P 500 rose +0.05% while the Dow climbed +0.1%, and Nasdaq finished +0.1% all eking out incremental gains to close at record highs. The Russell 2000 closed slightly negative by -0.3%

Retail news is front and center this morning with somewhat of a mixed bag of results. Home Depot and Kohl’s both missed and guided lower while TJX beat and raised guidance but put forth a conservative view of the all important holiday quarter. Today the muted retail outlook is the primary force behind the markets current negative / mixed sentiment however there are other positive factors at work attempting to mitigate the selling. Part of it appears to be company specific as in general earnings have surpassed expectations albeit on reduced expectations. 466 of the S&P 500 have reported so far with 79% having a positive earnings surprise.

Boeing announced today that it received 50 new orders at the Dubai Air Show for the 737 Max. Part of it appears to be continued optimism over the progress of trade deal with China. Former White House Economic Adviser Gary Cohen was quoted yesterday saying that he was optimistic a Phase 1 deal would be completed but that if it wasn’t by December 15th he believed additional tariffs would go into effect. Part of it also appears to be the “fear of missing out” as some investors cautiously dip a toe into the equity waters.

On the today, we have news out of the housing sector. According to the Commerce Department, October housing starts rose 3.8% to a 1.31 million annualized rate in line with estimates as single family home starts registered their strongest pace all year. Single family home starts increased 2% in October to 936,000 while permits for new construction of those starts climbed 3.2% to 909,000, the fastest pace since August 2007. Overall residential permits, which represents a signal for future construction, rose by 5% to a 1.46 million pace. That was the most since May of 2007. Data for September was revised to show home building declining to a pace of 1.266 million units, instead of decreasing to a rate of 1.256 million units as previously reported. Bottom line is lower mortgage rates are enticing buyers who may have been wavering boosting optimism within the industry ultimately contributing to more construction.

Oil continues to be leveraged to the trade talks as a recent mix of positive / negative rhetoric and concern over rising domestic inventories has hindered the commodity’s recent ascent. In fact today Brent has broken below $62 a barrel while WTI fell below $56. Gold is selling off a bit today as yesterday’s narrative that a temporary reprieve from Washington for China’s Huawei rekindled optimism for a trade deal between the countries boosting risk sentiment.

Sector strength is evident in Healthcare (+0.52%), Financials (+0.20%) and Technology (+0.15%). Lagging the market are Consumer Discretionary (-1.05%), Energy (-1.04%) and Utilities (-0.35%).

Sector Recap

Brian’s Technical Take

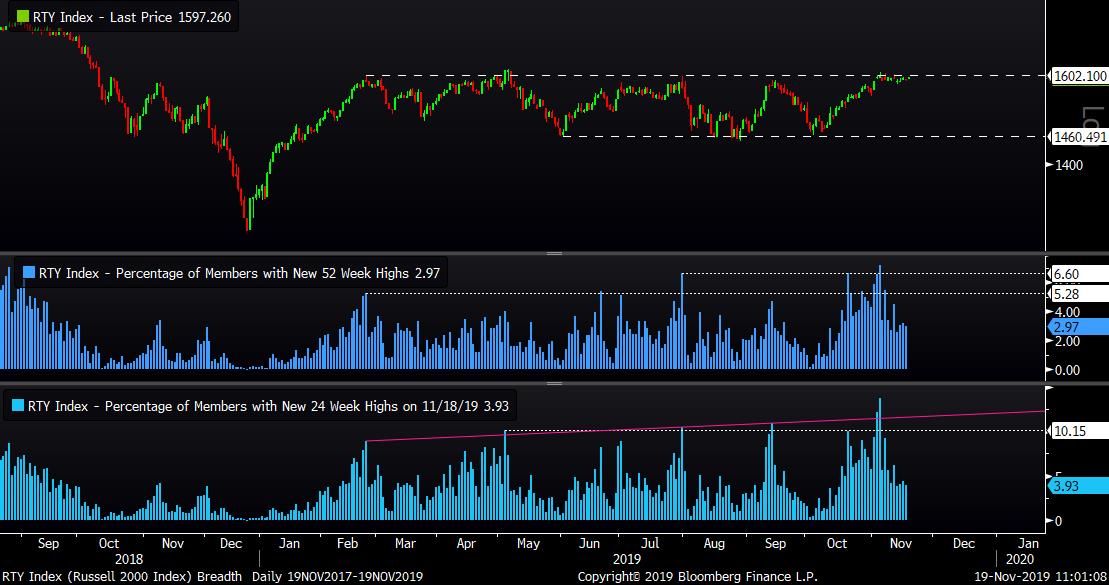

Now could be the time for small caps. The Russell 2000 index essentially made its 2019 high at the ~1,600 level all the way back in February and has since been consolidating in a sideways range. Price has retested this resistance level on three of four occasions since, but sellers quickly stepped up and drove it down ~8% to the 1,460 support.

Something changed on the most recent test of the 1,600 level earlier this month. Instead of reversing sharply lower as we saw in May, August, and October, buyers are holding their ground. Price is now in its third week of coiling like a spring, in a narrow range, along clearly defined resistance.

Throughout this range bound price action, breadth has been improving. Looking underneath the hood of the index we see there is an increasing number of companies making both new 24-week (lower panel) and 52-week highs (middle panel). This is noteworthy as breadth can often lead price. Not shown below but the weekly RSI, now 58, is also bumping up against its 2019 highs. From here it would not take much for a breakout in this momentum indicator.

While the large cap benchmarks have seen a nice run-up from their August lows, up until now the little guys have been held in check. However the technicals suggest bulls have laid their stake and could be on the cusp of taking new ground. Sellers beware.

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen-based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen-based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq, Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Stocks

The Market Intelligence Desk Team

Nasdaq

Nasdaq’s Market Intelligence Desk (MID) is designed to provide critical touch-points for timely trading analysis and market information.

MarketInsite

Nasdaq

Nasdaq’s Marketinsite offers actionable insights on a variety of market-moving topics. Learn from our thought leaders who are driving the capital markets of tomorrow.

Read MarketInsite's Bio