Dillard's Inc. DDS posted third-quarter fiscal 2024 results, wherein the top and bottom lines surpassed the Zacks Consensus Estimate. Meanwhile, the company’s sales and earnings declined year over year. A tough consumer landscape adversely impacted sales and comparable store sales (comps). However, DDS maintained a strong gross margin rate and delivered lower operating expenses, driven by stringent expense-control initiatives.

Earnings per share of $7.73 surpassed the Zacks Consensus Estimate of $6.47. However, the bottom line declined 16.9% from adjusted earnings of $9.30 in the year-ago quarter.

Find the latest EPS estimates and surprises on Zacks Earnings Calendar.

Net sales of $1.427 billion fell 3.3% from the prior-year quarter but beat the Zacks Consensus Estimate of $1.420 billion. Including service charges and other income, the company reported sales of $1.451 million, down 3.5% year over year.

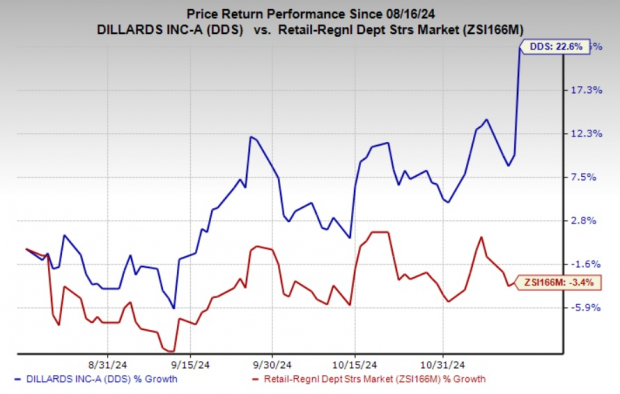

Dillard’s shares rallied 11.5% on Nov. 14, 2024, following the better-than-expected third-quarter fiscal 2024 results and optimism around lower operating expenses on disciplined expense control. Shares of the Zacks Rank #3 (Hold) company have advanced 22.6% in the past three months against the industry's 3.4% decline.

Dillard's, Inc. Price, Consensus and EPS Surprise

Dillard's, Inc. price-consensus-eps-surprise-chart | Dillard's, Inc. Quote

Detailed Analysis of DDS’s Q3 Performance

Total retail sales (excluding CDI Contractors, LLC) dropped 3.8% year over year to $1.356 billion. Comps declined 4% year over year. Retail sales were affected by the challenging sales environment. Our model had predicted a comps decline of 2.4% for the fiscal third quarter.

The company witnessed robust sales in the cosmetics category. On the flip side, men’s apparel and accessories, and juniors’ and children’s apparel were the weakest categories.

Image Source: Zacks Investment Research

The consolidated gross margin contracted 90 basis points (bps) year over year to 42.6%. The retail gross margin of 44.5% reflected a year-over-year decrease of 80 bps due to moderate gross margin declines in shoes, juniors’ and children’s apparel, home and furniture, and ladies’ apparel. The metric fell slightly in cosmetics and juniors’ and children’s apparel. However, this was partly negated by gross margin growth in ladies’ accessories and lingerie categories, with flat margins in men’s apparel and accessories, and cosmetics.

Dillard's consolidated SG&A expenses (as a percentage of sales) expanded 80 bps to 29.4% from the prior-year quarter. In dollar terms, SG&A expenses (operating expenses) declined 0.7% year over year to $418.9 million. The decrease in operating expenses is mainly attributed to stringent expense control measures, which resulted in flat payroll expenses. However, the company experienced an increase in insurance benefit expenses in the fiscal third quarter.

Our model had predicted SG&A expense growth (as a percentage of sales) to be 240 bps. In dollar terms, we expected SG&A expenses to rise 5.3% year over year to $444.3 million.

Dillard’s Other Financial Details

DDS ended the fiscal third quarter with cash and cash equivalents of $980.4 million, a long-term debt of $321.6 million, and a total shareholders' equity of $1.963 billion. The company provided $349.4 million of net cash from operating activities as of Nov. 2, 2024. Ending inventory increased 3% year over year as of Nov. 2, 2024.

In third-quarter fiscal 2024, the company repurchased 294,000 shares for $107 million, reflecting an average price of $364.43 per share. As of Nov. 2, 2024, the company had $287 million remaining under its current share repurchase authorization announced in May 2023.

The company expects capital expenditure of $110 million for fiscal 2024 compared with the $120 million mentioned earlier. The anticipated figure suggests a decline from the $133 million reported in fiscal 2023.

As of Nov. 2, 2024, DDS operated 273 Dillard’s stores, including 28 clearance stores across 30 states, and an online store at dillards.com.

What Dillard’s Expects for FY24?

For fiscal 2024, Dillard’s expects depreciation and amortization expenses of $180 million, flat with that reported in fiscal 2023. The company projects net interest and debt income expenses of $13 million against an income of $5 million in fiscal 2023. It anticipates rentals of $22 million, in line with the fiscal 2023 reported figure.

Key Picks

We have highlighted three better-ranked stocks, including Deckers Outdoor DECK, Abercrombie & Fitch ANF and The Gap Inc. GAP.

Deckers is a leading designer, producer and brand manager of innovative, niche footwear and accessories developed for outdoor sports and other lifestyle-related activities. DECK currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for DECK’s current financial-year sales and earnings per share implies growth of 13.6% and 12.6%, respectively, from the year-ago reported figures. The company has a trailing four-quarter earnings surprise of 41.1%, on average.

Abercrombie operates as a specialty retailer of premium, high-quality casual apparel for men, women, and kids. ANF currently carries a Zacks Rank #2 (Buy).

The consensus estimate for Abercrombie’s current financial-year sales and earnings indicates growth of 13.2% and 64.2%, respectively, from the year-ago reported figures. ANF delivered an average earnings surprise of 28% in the trailing four quarters.

Gap is a premier international specialty retailer offering a diverse range of clothing, accessories and personal care products. GAP currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for GAP’s current financial-year sales and earnings indicates growth of 0.5% and 31.5%, respectively, from the year-ago reported figures. The company delivered an average earnings surprise of 142.8% in the trailing four quarters.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpDillard's, Inc. (DDS) : Free Stock Analysis Report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Deckers Outdoor Corporation (DECK) : Free Stock Analysis Report

The Gap, Inc. (GAP) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.