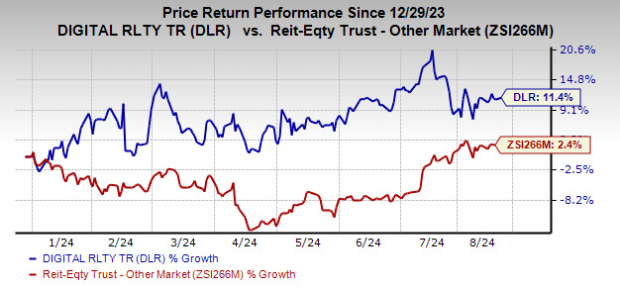

Shares of Digital Realty DLR have soared 11.4% in the year-to-date period compared with the industry’s growth of 2.4%.

The rising demand for high-performing data centers amid enterprises’ growing reliance on technology and acceleration in digital transformation strategies has been one of the key forces driving the performance of data center real estate investment trusts (REITs) like Digital Realty.

A solid tenant base assures stable revenues. It also carries out various development and redevelopment activities, which is encouraging.

Last month, the company, carrying a Zacks Rank #3 (Hold) at present, reported better-than-expected second-quarter 2024 results. It reported core funds from operations (FFO) per share of $1.65, outpacing the Zacks Consensus Estimate of $1.63. Results reflected healthy leasing activity and an increase in rental rates.

Image Source: Zacks Investment Research

Let us decipher the factors behind the surge in the stock price.

High growth in cloud computing, the Internet of Things and Big Data and the increasing number of companies opting for third-party IT infrastructure are spurring the demand for data center infrastructure. Growth in the artificial intelligence, autonomous vehicles and virtual/augmented reality markets is anticipated to be robust in the upcoming years.

Demand is strong in top-tier data center markets and despite enjoying high occupancy, the top-tier markets are absorbing new construction at a faster pace.

DLR has a high-quality, diversified customer base comprising tenants from cloud, content, information technology, network, and other enterprise and financial industries. It has a global presence, with 310 data centers in more than 50 metros with decent occupancy. The company is poised for growth with more than 5,000 global customers and growing.

Its tenant roster includes several behemoths and investment grade, and numerous customers use multiple locations across the portfolio. This assures stable revenue generation for the company. For 2024, management expects total revenues to grow 2% and adjusted EBITDA to grow 4% at the midpoint of their guidance ranges.

Also, DLR has a robust development pipeline, which seems encouraging. As of Jun 30, 2024, it had 8.5 million square feet of space under active development and 5.1 million square feet of space held for future development. Further, in recent years, Digital Realty has expanded in the Americas by adding capacity in New York, Northern Virginia and Toronto. For 2024, the company expects to incur capital expenditures for its development activities in the range of $2.0-$2.5 billion.

Its capital-recycling efforts aimed at bolstering balance sheet strength and driving long-term growth are encouraging. For 2024, it expects to carry out dispositions/joint venture capital in the range of $1.0-$1.5 billion.

Digital Realty has a solid balance sheet with ample liquidity and diversified sources of capital. The company exited the second quarter of 2024 with cash and cash equivalents of $2.28 billion. Its debt maturity schedule is well-laddered, with a weighted average maturity of 4.1 years and a 2.8% weighted average coupon as of Jun 30, 2024.

Solid dividend payouts are the biggest enticements for REIT shareholders, and Digital Realty remains committed to the same. The company has increased its dividend three times in the last five years, and the five-year annualized dividend growth rate is 2.84%. Given its solid operating platform and balance-sheet management efforts, the company remains well-poised to sustain the dividend payment.

However, given the industry's strong growth potential, intense competition from existing and new players could prompt competitors to resort to aggressive pricing policies, making DLR vulnerable to pricing pressure. Also, high interest rates pose a concern for the company.

Stocks to Consider

Some better-ranked stocks from the broader REIT sector are Four Corners Property Trust FCPT and Cousins Properties CUZ, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Four Corners’ 2024 FFO per share stands at $1.72, indicating an increase of 3% from the year-ago reported figure.

The Zacks Consensus Estimate for Cousins Properties’ 2024 FFO per share is pinned at $2.66, suggesting year-over-year growth of 1.5%.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 228 positions with double- and triple-digit gains in 2023 alone.

See Stocks Now >>Cousins Properties Incorporated (CUZ) : Free Stock Analysis Report

Digital Realty Trust, Inc. (DLR) : Free Stock Analysis Report

Four Corners Property Trust, Inc. (FCPT) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.