Credit: Shutterstock photo

Credit: Shutterstock photoMichael Johnston submits:

Master Limited Partnerships (MLPs) are entities that generally own infrastructure, such as pipelines that transport natural gas and crude oil. In order to qualify as an MLP, a firm must generate at least 90% of its income from what what the IRS deems to be "qualifying" sources, including the transport or processing of certain energy commodities. MLPs must make quarterly required distributions, which means that they are generally a source of stable and predictable cash flows to investors. And because MLPs are partnerships, they come with certain tax advantages-specifically, the avoidance of a corporate income tax.

MLP ETFs Booming

In early 2009 JPMorgan introduced the first exchange-traded product to offer exposure to MLPs, and in the two years since a number of new products targeting this asset class have popped up. There are now six ETPs in the MLPs ETFdb Category , as well as inverse and leveraged options for exposure to this sector. Until recently, all of the ETPs offering exposure to MLPs were structured as exchange-traded notes, as this method was believed to be the most efficient means of accessing a basket of MLP securities. In order to be classified as a Registered Investment Company under the 1940 Act, a fund can have no more than 25% of its portfolio in MLPs. Because ETNs are debt securities, they allow investors to enjoy the diversification benefits inherent in ETFs without adding another layer of taxes.

Among those six ETPs is the Alerian MLP ETF ( AMLP ), which ALPS launched in August. AMLP is the only MLP product structured as a true ETF. Unlike most ETFs, AMLP is structured as a C-corporation in order to be allowed to invest exclusively in MLPs. That election also adds some complexity to the tax picture, the ramifications of which have been the subject of significant debate and tremendous confusion in recent months [read MLP ETFs Fact And Fiction ].

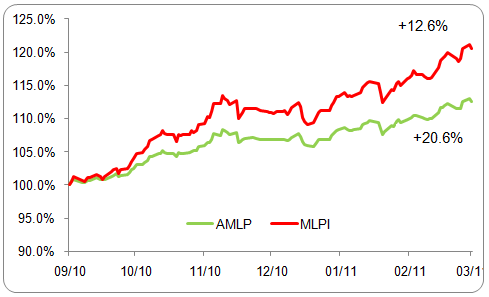

AMLP's success-it has accumulated nearly $800 million in assets in just a few months-indicates an abundance of investor interest in accessing MLPs through the ETF structure. But the introduction of AMLP has also sparked some debate among investors, with some declaring it to be a flawed product destined to lag behind similar ETNs. Since its inception, AMLP has trailed the UBS E-TRACS Alerian MLP Infrastructure Index ETN ( MLPI ), which is linked to the same index, by a fairly wide margin:

While this difference in performance is due primarily to the tax characteristics of these two securities, investors shouldn't draw conclusions on the universal superiority of one vehicle or another based on the above. In reality, there are tax pros and cons to both the ETF and ETN vehicles, and the relative performance of AMLP and MLPI will depend on a number of factors. To understand how the selection of a vehicle can impact the bottom line returns realized by investors, we take a deeper dive and consider the performance that can be expected under various scenarios.

Variables

When determining the performance that can be expected from each type of vehicle, there are several variables that will impact bottom line gains or losses:

- Individual Income Tax Rate: For investors in an MLP ETN, distributions will be taxed at the individual income rate. As such, the higher the individual income tax rate, the lower the total returns for an MLP ETN (meaning that the extension of the 35% maximum individual rate under the Bush tax cuts was good news for investors in MLP ETNs).

- Corporate Tax Rate: For investors in an MLP ETF, a portion of the distributions will often be taxed as a return of capital and a portion will be subject to corporate income taxes (according to Wells Fargo, return of capital has historically comprised about 80% of total distribution). As such, the higher the corporate tax rate, the higher the potential tax liability for an MLP ETF.

- Return Of Capital: Distributions treated as return of capital are taxed at more favorable rates than regular distributions-so the greater this percentage, the more advantageous the ETF structure will be when it comes to distributions (as mentioned above, historically return of capital has comprised about 80% of total MLP distributions).

- Source Of Return: In general, the ETN is more efficient when it comes to returns generated through capital appreciation while the ETF can be more efficient when it comes to returns generated through distributions. As such, the mix between these two sources of return will have an impact on the ultimate, bottom line, after tax returns generated.

- Tax Status: This is perhaps the most important variable in this entire equation, and unfortunately the variable whose impact is the most challenging to quantify. The ability to defer taxes for extended periods of time (or even indefinitely) may make achieving MLP exposure through an ETF more appealing, as we discuss in a bit more detail below.

To illustrate more explicitly how each of these variables translates into bottom line returns-and to dispel some of the myths about inherent advantages and disadvantages of various structures-we outline below three different scenarios. Making some assumptions, each scenario considers a different value for the capital appreciation portion of total return.

Assumptions:

- For the ETF, 80% of distributions are treated as return of capital (assuming 90% would enhance returns to ETF, while assuming 70% would lead to less favorable results for the ETF).

- Distribution yield is 6.2%, approximating the current annual yield on the Alerian MLP Infrastructure Index.

- Beginning NAV for both securities of $100

- Individual income tax rate and corporate tax rate are 35%, consistent with current legislation

- Qualified dividend tax rate and long-term capital gains rate are 15%, consistent with current legislation

After Tax Distribution

The first component of total return that must be considered is the after-tax distribution. For the ETN, this calculation is pretty straightforward: the distribution is taxed at the individual income tax rate. Assuming a distribution of $6.20 and a 35% rate, the after-tax distribution is $4.03.

For the ETF, computing the after tax distribution is a bit more complicated. If 80% of the distribution is treated as return of capital-meaning that it is tax deferred-the remaining 20% will be taxed at the corporate rate. In this example, that works out to a corporate tax of $0.43 and an after-corporate tax distribution of $5.77:

Here's where things get a bit more complex. ETF investors will be forced to reduce the cost basis for tax accounting purposes to the extent that they receive tax-deferred distributions. In this example, that's the 80% of distribution treated as return of capital, or $4.96. The difference between the after-corporate tax distribution ($5.77) and the investor level cost basis reduction ($4.96) would be taxed at the qualified dividend rate of 15%, adding another $0.12 to the ETF tax bill:

The treatment of the tax obligation associated with tax deferred distributions and tax deferred capital gains is a tricky issue. Though these obligations are incurred as distributions are made and the underlying securities appreciate or depreciate, they will not need to be paid until the investment is liquidated. Many investors have the ability to delay the payment of these obligations indefinitely, but this example includes these costs at the time they are incurred. This obviously ignores the time value of money. For certain investors, the benefit associated with being able to delay the tax obligations may be material in nature, and could dramatically shift the calculation of returns derived from each security.

The above calculations highlight the primary advantage of the ETF vehicle as a means of accessing the MLP sector: after the consideration of all taxes, the after-tax distribution from the ETF will be greater than the return a comparable ETN will generate. With a distribution yield north of 6%, the difference can be significant-$5.65 versus $4.03 in this case.

Deferred Tax Liabilities / Assets

The second piece of the puzzle that must be considered is the creation of deferred tax assets and liabilities, as well as deferred capital gains or losses at the investor level. For the ETN, calculating the deferred tax liability or asset is pretty simple-there isn't one.

For the ETF, there would be two components of the deferred tax liability/asset: distribution and change in price. Multiplying the tax-deferred portion of the distribution (the $4.96 in this example) by the corporate tax rate of 35% yields a deferred tax liability related to the distribution of $1.74.

In addition, the MLP ETF would accrue a deferred tax liability or asset equal to the appreciation in the underlying securities multiplied by the corporate tax rate. This can obviously be a positive or negative-in bear markets it will soften the blow while in bull markets it will eat into returns.

The final element is the investor level deferred capital gain or loss, a calculation that brings in the cost basis reduction required when tax deferred distributions are received. For the ETF, this figure is calculated as ((Ending NAV - (Starting NAV - Cost Basis Reduction) x Capital Gains Tax Rate)). As such, the amount of both the deferred tax asset/liability related to the change in value of the securities and the deferred capital gain/loss depend on the performance of the underlying MLPs:

For the ETN, computing the deferred capital gain or loss uses the same formula, but because there is no cost basis reduction required it is a more straightforward calculation: Change in NAV x Capital Gains Tax Rate.

Putting it all together, the total return picture looks something like this:

It's worth repeating that while this example may seem complex, it is simplified in a few important ways. Most importantly, the above table doesn't take into account the value investors in the ETF would derive from being able to defer taxes; our example assumes that the position is liquidated at the end of the period. Since many investors have the ability to defer taxes indefinitely-or at least over a very long time period-this benefit can be material. Taking into account the time value of money would reduce the present value of deferred tax liabilities related to the tax deferred distributions paid by the ETF, thereby improving the bottom line for that type of vehicle.

The analysis also assumes that the ETF is able to make distributions equal to the distributions of the ETN. Because the ETF will have to pay some taxes on the distributions it receives from the underlying MLPs, it is possible that it would be required to either make smaller distributions of sell some of the underlying holdings to make equivalent distributions.

Hopefully the above helps to prove that when it comes to MLP exposure, there are potential return benefits to both ETFs and ETNs (and, of course, to simply buying up individual MLPs and steering clear of all the tax-related complications). Having noted these limitations in the above analysis, some conclusions can be drawn on the relative merits of the ETF and ETN structures:

- An MLP ETN will generally be more volatile than an otherwise similar ETF-on both the upside and the downside-because the ETF will accrue a deferred tax liability/asset

- The ETF structure may be preferable for investors who prefer tax-deferred distributions

The lesson here is not to read too much into the hype surrounding various securities, and to do your homework on the potential advantages and disadvantages yourself.

Disclosure: No positions at time of writing.

Disclaimer: ETF Database is not an investment advisor, and any content published by ETF Database does not constitute individual investment advice. The opinions offered herein are not personalized recommendations to buy, sell or hold securities. From time to time, issuers of exchange-traded products mentioned herein may place paid advertisements with ETF Database. All content on ETF Database is produced independently of any advertising relationships.

See also Thursday ETF Roundup: UNG Tumbles on Storage Report, EWZ Rises on Commodity Strength on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}