Alibaba's BABA recent second-quarter fiscal 2025 results paint a picture of steady growth amid challenging market conditions.

While revenues of $33.7 billion exceeded the Zacks Consensus Estimate by 0.69%, the non-GAAP earnings of $2.15 per ADS fell short of the consensus mark by 4.87%, reflecting increased strategic investments across key business segments.

Core Business Strength and Monetization Progress

The company's domestic e-commerce segment demonstrates robust fundamentals, with Taobao and Tmall reaching new heights in monthly active consumers. The implementation of a 0.6% software service fee and increased adoption of the AI-powered Quanzhantui marketing tool have strengthened monetization capabilities. The successful 11.11 Global Shopping Festival achieved record-high monthly active consumers, indicating strong consumer engagement. The 88VIP membership program's growth to 46 million members suggests improving customer loyalty and potential for sustained revenue growth.

Cloud and AI Innovation Driving Future Growth

Alibaba Cloud's performance stands out as a significant growth driver, with revenues, excluding consolidated subsidiaries, growing 7% quarter over quarter. The cloud segment's strategic focus on AI has yielded impressive results, with AI-related products maintaining triple-digit growth for five consecutive quarters. The company's commitment to investing in AI infrastructure and advanced technology positions it well to capitalize on the growing demand for cloud computing and AI services across industries.

International Expansion and Strategic Investments

The Alibaba International Digital Commerce segment showcased strong momentum with 29% revenue growth, driven by successful expansion in key markets. The AliExpress Choice initiative continues to deliver robust growth while improving unit economics. Strategic investments in European and Gulf region markets, coupled with the launch of AI-powered tools like the B2B search engine, demonstrate the company's commitment to international market penetration and technological innovation.

Price Performance & Valuation

The stock has returned 11.9% year-to-date against the Zacks Internet-Commerce industry, the Zacks Retail-Wholesale sector and the S&P 500’s return of 30%, 23.2% and 24.5%, respectively.

Alibaba’s dominant e-commerce position in China remains threatened by global bigwigs like Amazon AMZN and eBay EBAY. Also, BABA's growth in the global cloud market has been significantly hindered due to rising competition from the leading cloud players, namely Amazon, Microsoft and Alphabet’s GOOGL Google.

Year-to-date Performance

Image Source: Zacks Investment Research

Alibaba is currently trading at a discount with a forward 12-month Price/Earnings of 8.38X compared with the industry’s 24.63X and lower than the median of 15.56X. This valuation metric indicates that Alibaba's stock is significantly undervalued compared to its industry peers, trading at less than half the industry average P/E ratio. The lower-than-median forward P/E suggests an attractive entry point for investors, as the stock appears to be trading below its fair market value despite strong fundamentals. It also has a Value Score of A, which is hard to ignore.

BABA’s P/E F12M Ratio Depicts Discounted Valuation

Image Source: Zacks Investment Research

Investment Outlook

From an investment perspective, several factors make Alibaba an attractive buy at current levels. The company's aggressive share repurchase program, having spent approximately $10 billion in the first half of fiscal 2025, demonstrates confidence in its long-term value proposition. The completion of its primary listing in Hong Kong and inclusion in the Southbound Stock Connect has broadened its investor base, with significant net inflows of HK$46 billion, indicating strong institutional interest.

Despite increased investments impacting short-term profitability, Alibaba's strategic focus on core business growth, AI innovation and international expansion presents compelling long-term value. The company's strong net cash position of US$50.2 billion provides ample flexibility for continued investments in growth initiatives while maintaining financial stability.

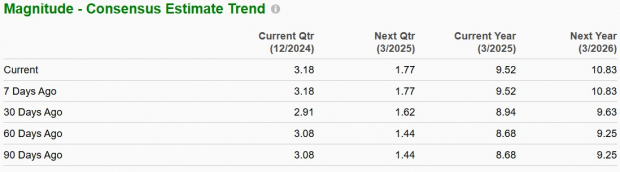

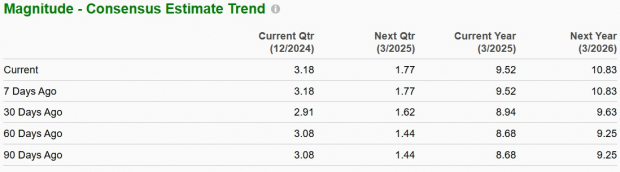

The Zacks Consensus Estimate for fiscal 2025 revenues is pegged at $140.46 billion, indicating 7.63% year-over-year growth. With the Zacks Consensus Estimate for fiscal 2025 earnings indicating an upward revision of 3% over the past 30 days to $8.94 per share, the market appears increasingly confident in Alibaba's growth trajectory.

Image Source: Zacks Investment Research

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

Conclusion

While competitive pressures in the e-commerce sector remain intense, Alibaba's multi-faceted growth strategy, improving operational efficiency in loss-making segments, and leadership in cloud computing and AI technology make it an attractive investment opportunity for investors seeking exposure to China's digital economy transformation. BABA stock currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpAmazon.com, Inc. (AMZN) : Free Stock Analysis Report

eBay Inc. (EBAY) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.