Affirm Holdings, Inc. AFRM reported first-quarter fiscal 2025 results last week, wherein its earnings beat estimates. Results were aided by improved card network revenues and servicing income, along with growing repeat customers. However, the upside was partly offset by an escalating expense level from a significant increase in provision for credit losses.

Now the question arises whether investors should consider buying the stake or hold tight to their current investments. Let us answer that question by assessing AFRM’s latest quarterly results and long-term growth prospects.

AFRM’s Q1 Results in Brief

Affirm incurred a fiscal first-quarter loss of 31 cents per share, which was narrower than the Zacks Consensus Estimate of a loss of 36 cents. The metric was flat year over year. Total net revenues amounted to $698.5 million, which rose 40.7% year over year. The top line surpassed the consensus mark by 5.6%.

Active merchants of AFRM increased 21.4% year over year to 323,000 as of Sept. 30, 2024. Total transactions of 27.2 million soared 45% year over year on the back of a significant rise in repeat customer transactions. Servicing income improved 28.9% year over year to $26 million. Interest income of $377.1 million grew 44% year over year.

For a detailed analysis, please read our blog on fiscal first-quarter earnings: Affirm Holdings Q1 Loss Narrower-Than-Expected, 2025 GMV View Up

Affirm Benefits From Higher GMV

An expanding Gross Merchandise Volume (GMV) continues to benefit merchant network revenues, which remain one of the most significant contributors to Affirm’s top line. Merchant network revenues mainly comprise merchant fees, which are charged to merchant partners (or integrated merchants) based on the GMV processed through the Affirm platform.

Merchant network revenues advanced 26.3% year over year in the fiscal first quarter. Meanwhile, GMV of $7.6 billion increased 35.7% year over year, attributed to strength in general merchandise and travel and ticketing categories. Management anticipates a GMV of more than $34 billion in fiscal 2025, which denotes an increase from the fiscal 2024 reported figure. Therefore, rising GMV is likely to benefit AFRM’s revenues in the days ahead.

AFRM’s Long-term Growth Prospects

Affirm's unique technology and data-driven approach provides it with an edge in accurately pricing and underwriting credits at the point of sale. This capability allows it to craft tailored products such as interest-bearing installment loans that attract a diverse consumer demographic, thereby significantly boosting its GMV. In fiscal 2024, Affirm facilitated $26.6 billion in GMV.

The company's business structure fosters robust network effects that grow stronger with each merchant added to its platform. As Affirm attracts more users, merchants are drawn to adopt its payment solutions to access this expanding consumer pool. This not only bolsters merchant relationships but also increases their customer acquisition rates and the average value of orders. Lowered operational costs and enhanced accuracy in credit decisions due to repeat consumer interactions also contribute to improved efficiency.

Alliances with industry giants such as Amazon and Apple Pay serve as key growth drivers for Affirm. These collaborations grant access to vast consumer markets and help diversify revenues across different sectors. This expanded reach supports Affirm's plans for international growth, particularly its expected entry into the U.K. market in 2025, further boosting long-term prospects.

The burgeoning buy now, pay later (BNPL) sector presents a lucrative opportunity for AFRM to leverage its extensive array of payment solutions. The popularity of installment payments is on the rise as they alleviate the financial burden of lump-sum payments.

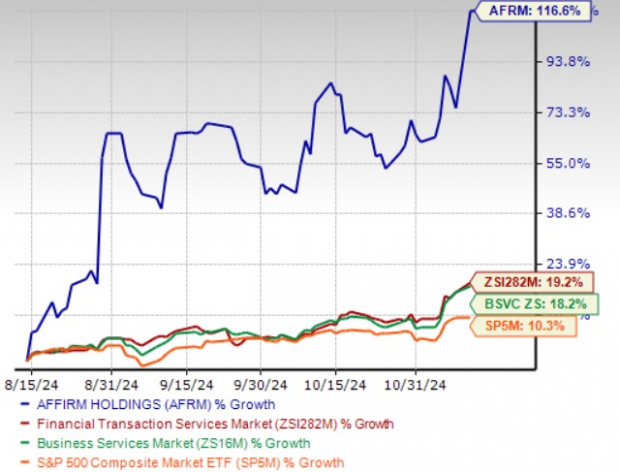

AFRM Stock’s Price Performance

Affirm’s shares have gained 116.6% in the past three months compared with the industry’s 19.2% growth. It has also outperformed the broader Zacks Business Services sector’s 18.2% rise and the S&P 500’s 10.3% rally in the said time frame. In comparison with AFRM, two of its industry peers, Mastercard Incorporated MA and Visa Inc. V have gained 13.3% and 18.4%, respectively, in the same time frame.

Three-Month Price Performance

Image Source: Zacks Investment Research

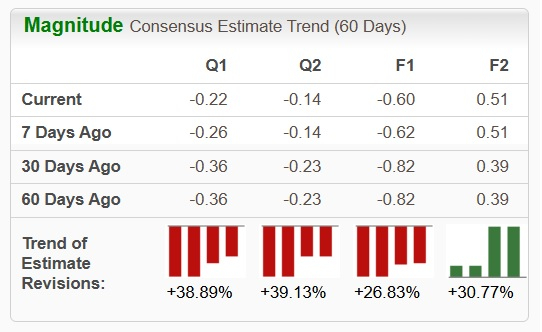

Estimate Revisions Favor Affirm

Earnings estimates for AFRM have moved up over the past 30 days, reflecting analysts’ optimism. The Zacks Consensus Estimate for 2025 and 2026 earnings has been revised upward over the same time frame.

The consensus estimate for fiscal 2025 earnings indicates a 64.1% year-over-year improvement, while the estimate for fiscal 2026 earnings implies an increase of 186.3%. The consensus mark for fiscal 2025 and 2026 revenues suggests 33.5% and 23.9% year-over-year growth, respectively.

Image Source: Zacks Investment Research

AFRM’s Valuation

The company is cheaply priced compared with the industry average. Currently, AFRM is trading at 5.5X forward 12-months sales, below the industry’s average of 7.44X.

Image Source: Zacks Investment Research

Conclusion

Affirm’s fiscal first-quarter results highlight both its strengths and obstacles for investors to consider. Its focus on proprietary technology and data-driven risk models sets it apart in the highly competitive BNPL market. With strong GMV growth, strategic partnerships and international expansion plans, particularly in the U.K., the company is well-positioned for long-term growth.

AFRM’s relatively lower valuation compared with the industry and improved profit estimates further enhance the attractiveness of the stock. This presents a lucrative opportunity for investors to add the stock to their portfolio.

AFRM currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Mastercard Incorporated (MA) : Free Stock Analysis Report

Visa Inc. (V) : Free Stock Analysis Report

Affirm Holdings, Inc. (AFRM) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.