Debit and Credit Cards: How and Why to Use Them

It’s important to know how to take advantage of credit and debit cards and using them correctly is particularly important for college grads. Building credit will allow you to make bigger purchases, rent an apartment, take out loans, and more. Debit cards are helpful for grads on-the-go who may need some quick cash in an instant.

What Is a Debit Card and How Do You Use It?

A debit card is a payment card that lets you easily withdraw money directly from your bank account. Typically, your debit card is linked to your checking account, which is where you store your money for spending.

How to Use It

You can use your debit card for most transactions you want to make. Whether you want to buy something at a store, order something online, or use an ATM to take out some extra cash, this card comes in handy. Once you swipe your debit card, the money is taken directly from the balance you have in your checking or savings account, so be careful not to spend more than you have – you’ll likely be charged an overdraft fee.

Note that many banks limit the amount of money that you can spend in a day. If you’re doing some Christmas shopping and your cashier discreetly tells you that your card declined, don’t panic! You may have just gone over your limit for the day. Most banks are looking out for card fraud too, making sure that no one stole your card and is trying to take all your money.

There are instances where financial experts would recommend not using your debit card. From a safety standpoint, avoid using your debit card at gas stations, online, or suspicious ATMs; scammers have found ways to get your card information this way. In terms of personal finance, using a debit card can put you at risk of over-drafting when shopping. You also lose out on leveraging your credit card bonuses such as cash back rewards, so think twice about using your debit card. For more information on where to avoid using a debit card, check out this brief article by Business Insider.

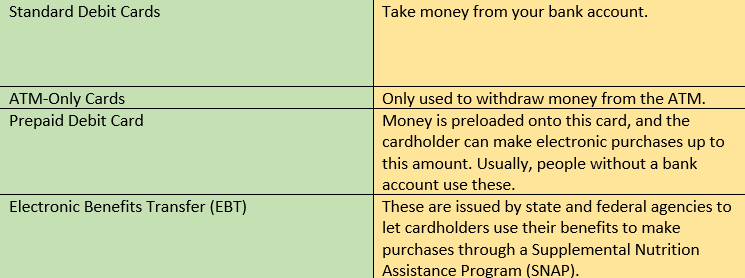

Types of Debit Cards

Selecting the best debit card for you can be intimidating. Luckily, countless sites offer in-depth suggestions. For example, check out NerdWallet’s recommendations to learn more about debit cards with rewards.

How to Set up Your Debit Card

1. Set up a checking account

Once your account is set up at your bank, you’ll receive a debit card in the mail in a couple of business days. Learn how to set up a checking account here.

2. Activate your debit card

Call the number on your debit card to set up your PIN, your Personal Identification Number. You’ll enter your PIN when completing an in-store purchase, or withdrawing money from an ATM. You can activate your card by inserting it into your bank’s ATM.

What Is a Credit Card and How Do You Use It?

A credit card allows you make payments by borrowing money from your bank. Unlike debit cards, credit cards do not withdraw funds directly from your account – you are instead using loaned money, or a line of credit, to make payments.

Why would so many people opt for a credit card when a debit card lets you spend the money from your account? The answer is simple: to build credit. A good credit score can help you take out loans, get approval to rent an apartment, have access to better insurance rates, and more.

How to Use It

When you pay the money back to your bank, you’ll be paying it back with interest, or the money you’re charged for borrowing the bank’s money. It’s best to pay off your balance as soon as you can to avoid having to pay more money – the more you owe, the more interest you accumulate.

Banks typically require that you pay a minimum amount of your balance each month, not necessarily your whole bill. But be careful, if you only pay the minimum, the interest will increase the extra amount of money you have to pay, and the amount of money you'll owe can rapidly accumulate.

However, most banks offer what's known as "grace periods," which is a set time you have to pay off your balance before the bank charges interest. Interest is typically not charged until the day after your bill is due, so if you pay off in full before that date, you won't owe any interest.

Two other things to consider: Depending on the kind of card you get, you might need to pay an annual fee for using it. The other thing to consider is finding a card that offers rewards, such as a percentage of cash back for every purchase. You can get a card that waives the annual fee, but they usually offer less features than rewards cards. And if you do have a cash back card, it can be a way to save a little extra money (especially if you're paying off your balance in full before interest kicks in).

The potential to accumulate debt is riskier with a credit card, so if you don’t think you can pay back your bill, a debit card might be a better fit.

Your bank will only allow you to borrow up to a certain amount. The better your credit score, the more your bank will loan to you - yet another reason to maintain a healthy credit score. A good credit score is generally in the 660 to 780 region but varies depending on who you ask.

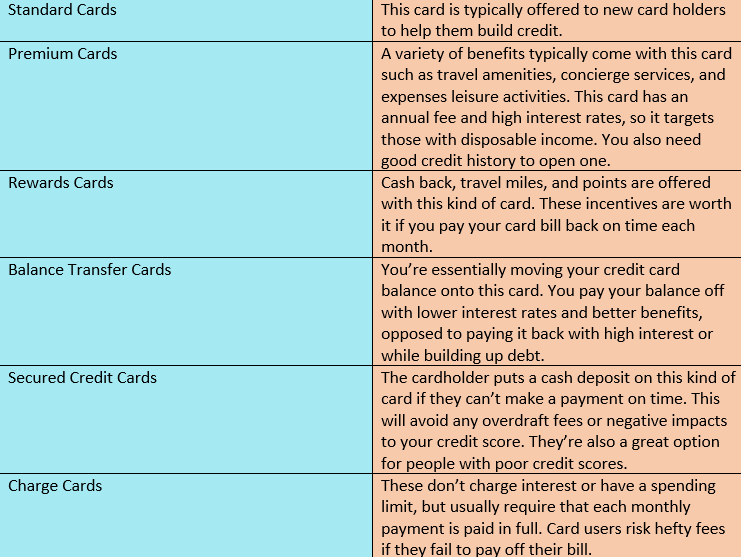

There Are Different Types of Credit Cards. Here Are a Few:

If you’ve managed to skate through college without a credit card, try starting with a standard card to build up a good credit score. Although if you’ve been building credit, look into a rewards card to start profiting from your financial responsibility. Now that you’ve graduated, you deserve to reap the benefits. Check out NerdWallet’s suggestions for the Best Credit Cards for Recent College Graduates in June 2022.

How to Set up Your Credit Card

1. Check your credit score

Certain credit cards require a certain credit score for you to be allowed to open one. If this is your first credit card, look into standard cards that will allow you to open a card without credit history.

2. Choose how you want to apply

You can apply online, in your bank, by phone, or by mail. It’s easy to fill out an application online, but keep in mind that bank employees may be able to answer your questions quicker if you go into your bank to fill one out.

3. Fill out application

You’ll likely be asked to provide your Social Security Number and annual income, as well as if you have a balance on other accounts that you may already have. On top of generic questions about your contact information, you’ll be asked to acknowledge the terms and conditions of the credit card before you submit your application.

4. Activate your card

You can call the number on the credit card to activate your card, similar to how you would activate a debit card.

Structurally, debit and credit cards look very similar even though they work in different ways. You’ll be asked to enter your card number, expiration date, and CVV code when making an online purchase, so it’s important to know where to find them. Also note that many, but not all, cards have a chip in them; when making in-store purchases, this is the end of the card you’ll enter into the PIN pad, or tap the pad, by the cash register.

You should also sign the back of your card. Cashiers are supposed to check that your signature on the card matches the signature on the sales receipt – this is meant to avoid debit/credit card fraud.

If someone steals your card, your card information, or if you lose it, call your bank right away. They’ll be able to cancel the card and send you a new one. And as long as you’re timely, you will likely be reimbursed with any money stolen from your account.

It’s important that you are always monitoring your bank statements so that you can catch any theft. Note that credit cards have better protection against fraud because the bank is responsible for the fraudulent charges, not the cardholder.

This is part of a bigger series that was designed to guide recent college graduates towards reaching their professional goals and benefiting from their studies. Check out our guide to post-graduate life to learn how to leverage your degree financially.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Personal Finance Saving Money

Kristin Lasker

Kristin is a Digital Intern for the Summer of 2022. She's working on a series to help guide recent college graduates to financial success and independence, while working with Nasdaq's marketing team.

Read Kristin's Bio