Copper prices stayed elevated in Q2 as new factors further impacted already strained supply/demand.

Copper supply has been affected by disruptions at major mine sites, smelter and refiner concentrate shortages and the US-led war against Iran, which has led to the closure of major shipping lanes in the Middle East.

Against that backdrop, demand has continued to increase as artificial intelligence (AI) data center development continues, spurring downstream needs for electricity generation. These developments come on top of base-level growth from urbanization, the energy transition and upward mobility in the Global South.

What happened to the copper price in Q2?

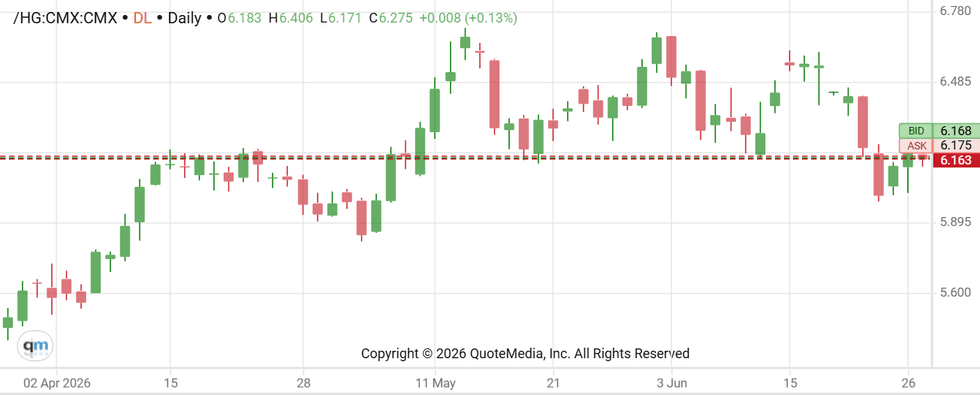

Copper prices opened Q2 near year-to-date lows, with the continuous contract reaching US$5.64 per pound on the Comex and three month contracts hitting US$12,434.50 per metric ton on the London Metal Exchange (LME).

Prices for copper on both exchanges posted consistent gains throughout the month of April, with the Comex price reaching US$6.12 and the LME price climbing to US$13,433 on April 22.

Chart via the Investing News Network.

Copper price, April 2 to June 29, 2026.

Prices fell slightly through the end of April, but regained momentum at the start of May. From there, copper continued its upward trajectory, setting a new all-time high on the Comex of US$6.72 on May 13.

It was a similar story on the LME, where copper reached US$14,196.50 during intraday trading.

Since that time, prices for the red metal have retreated somewhat, but have continued to trade close to yearly highs, coming in at US$6.13 on the Comex and US$13,371 on the LME on June 23.

Copper supply remains strained

Copper supply has been constrained since 2025 after significant shutdowns at Freeport-McMoRan's (NYSE:FCX) Grasberg mine in Indonesia and at Kamoa-Kakula, a joint venture between Ivanhoe Mines (TSX:IVN,OTCQX:IVPAF) and Zijin Mining (HKEX:2899,SHA:601899,OTCPL:ZIJMF) in the Democratic Republic of Congo (DRC).

Although operations have restarted at both mines, they haven't yet returned to full capacity.

In an email to the Investing News Network, Ruilin Wang, associate director, copper-zinc, at S&P Global Energy, said Grasberg is targeting 60 percent of capacity by the end of the year and has pushed its timeline for full production back to 2028 due to wet ore complications. For its part, Kamoa-Kakula has revised its guidance downward by 22.5 percent, to 290,000 to 330,000 metric tons, as recovery efforts have been slower than anticipated.

Adding to the woes of beleaguered mine supply are disruptions in Chile, the world’s top copper producer, where production forecasts have shifted from projected production growth of 3.7 percent to a 2 percent decline.

The slowdown has been significant, with Q1 data showing a 9 percent decline versus the same period last year.

Wang attributes the slowdown to ongoing challenges faced by Chile's Codelco; these difficulties stem from aging mines and recovery efforts at El Teniente, the world’s largest underground copper mine.

Significant portions of the mine collapsed in August 2025 following an earthquake at the site, killing six workers.

In a Reuters report on February 10, Codelco executives set production expectations at 301,000 metric tons in 2026, but said they don’t expect the operation to ramp back to full capacity for another five years.

Hormuz closure disrupts key shipping lanes

However, it’s not just lower mine output that's impacting copper supply.

“Supply chain obstacles have now layered on top. The Strait of Hormuz closure following the US-Israel war with Iran that began on February 28 has introduced a new and compounding set of supply-side risks,” Wang said.

The most significant concern for the market is disrupted supply of sulfuric acid, which is used in the solvent extraction and electrowinning processes in Chile and the DRC. As traffic has been unable to transit the strait, sulfuric acid prices have skyrocketed, climbing to all-time highs in key regions, with prices in the Middle East at US$820 per metric ton and even higher in import regions like Brazil, at US$1,200 per metric ton.

High sulfur prices and closure of shipping lanes have sent ripples through base metals markets and have led China to halt all exports of sulfur in May to prioritize domestic use in fertilizer production.

Additionally, the war has led to severe disruptions in energy shipments and destabilized production in key areas, including Qatar’s Ras Laffan liquefied natural gas (LNG) plant, which supplies close to one-fifth of the world’s LNG.

Attacks on the plant have caused tremendous damage, and QatarEnergy, which owns the plant, doesn’t expect output to return to normal for three to five years. This could have lasting effects on the copper market and prices, as more than 10,000 metric tons of sulfur are produced at the Ras Laffan common sulfur plant every day.

When a memorandum of understanding was signed between the US and Iran on June 17, there appeared to be hope that the conflict was over and the strait would reopen as the two sides worked on a permanent deal.

However, by June 19, more attacks had been launched by Iran on targets in Israel and Gulf states, including the Ras Laffan plant. While the attacks only lasted for a couple of days, they highlighted the fragility of the peace process and the concerns around a mid to long-term closure of the Strait of Hormuz.

“The closure’s impact is broad, affecting not just Asian producers, but also South and North America, Africa,” Wang said. She added that Chile was already facing supply gaps for sulfuric acid in H2 2026. Meanwhile, Asian wire and cable producers have already experienced output declines due to bottlenecks in natural gas and insulators.

Copper demand outlook gains clarity

The key elements fueling copper demand at the start of the year remain, though they have softened somewhat.

Growth in AI continues, demanding copper inputs for data center construction and for the energy grid.

“The market’s demand forecasts for copper — driven by electrification, AI infrastructure and grid expansion — are now more balanced. While estimates may have been overly optimistic in the previous years, current forecasts reflect a more rational view of medium-term demand growth into 2027 and beyond,” Wang said.

China has long been the largest consumer of copper, much of it destined for the construction sector, but demand there has lessened in recent years as the real estate sector hasn’t recovered from its 2020 collapse.

However, at the start of the year, the slow growth in China was offset by an increase in demand from grid expansion, electric vehicle (EV) production and exports. According to data supplied to the Investing News Network by JPMorgan Chase & Co. (NYSE:JPM), Chinese apparent consumption has remained strong, registering a 9 percent year-on-year increase in April as warehouse inventories were destocked throughout the supply chain.

Outside China, the firm suggests that energy disruptions due to the Middle East conflict may actually help copper demand, as high energy costs will lead more consumers to turn to oil and gas alternatives.

JPMorgan also notes in its report that China has been a leader in EV production, photovoltaics and grid expansion, while the rest of the world has lost momentum in those areas. However, a shift is likely to come as greater focus on petrol costs and availability will drive a structural boost outside of China.

Evidence of that may already be emerging, with Chinese exports of EVs and hybrids jumping 140 percent in March to 350,000 units, and battery shipments up 16 percent above the Q4 2025 average.

Likewise, searches for EVs in March rose by 25 percent.

Copper price forecast for 2026

There are a few factors for copper investors to keep an eye on as the year continues.

Perhaps the most important is what happens with the US-Iran conflict. If shipping routes out of the Persian Gulf remain closed, then supply deficits could worsen and the market could be knocked out of balance.

Even if the strait fully reopens, it will take time for shipping, and by extension production, to return to normal.

Another point to be aware of is that US Secretary of Commerce Howard Lutnick is expected to deliver a review of Section 232 copper tariffs on June 30. It will determine if any modifications to current rates are necessary.

JPMorgan said it expects the Trump administration to implement the escalating 15 percent tariffs laid out in the original executive order, effective from July 2025.

By doing this, the US will ensure that all imports remain in the US, and that excess copper in US warehouses will serve as a critical reserve, rather than implementing a policy that may incentivize rapid destocking.

For her part, Wang projects that the average LME copper price for 2026 will be US$12,600, a 26 percent increase over the 2025 average.

Don’t forget to follow us @INN_Resource for real-time news updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.