Central Garden & Pet Company CENT has not been performing well for a while now, due to several headwinds including a tough operating backdrop. Macroeconomic factors such as cost inflation, evolving consumer behavior and unfavorable retailer inventory dynamics have been further concerns for the company.

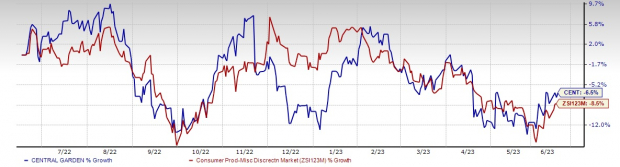

Shares of this producer and distributor of lawn and garden products, and pet supplier have lost 6.5% in the past year, compared with the industry’s 8.5% decline. For fiscal 2023, the Zacks Consensus Estimate for Central Garden & Pet’s sales and earnings per share (EPS) is currently pegged at $3.31 billion and $2.35, respectively. These estimates show corresponding declines of 0.9% and 16.1% from the year-ago period’s figures.

Let’s Delve Deeper

We note that the company has been witnessing sluggishness in its Garden segment for a while now. Gardening is generally limited to the period between spring to summer, which makes the garden business highly seasonal in nature. Failure to perform during the season is likely to have a significant impact on the company’s yearly financials.

The Garden segment’s net sales decreased 5% year over year to $434 million during second-quarter fiscal 2023. This is driven by lower sales in Grass Seed, Controls & Fertilizer and Live Goods, partly offset by strength in Wild Bird and Packet Seed.

Unfavorable spring weather and changes in retailer buying patterns hurt net sales. This followed a decline of 6% in the preceding quarter. The segment’s operating income came in at $50 million, down from the $71 million reported in the prior-year quarter, while the operating margin contracted 400 basis points to 11.4%. Soft sales, input cost inflation and initial start-up costs associated with the recently acquired live goods facility hurt margins.

Image Source: Zacks Investment Research

Also, the company’s Pet segment has been soft for a while now. The segment’s sales came in at $475 million, down 5% from the year-ago period. This followed a decline of an equivalent percentage in the preceding quarter. The metric declined due to the muted demand for durable pet products, the decision to discontinue certain low-profit private-label pet bed product lines and lower sales in Outdoor Cushions. The segment’s operating income came in at $55 million, down from the $61 million reported in the prior-year quarter. Meanwhile, the operating margin shrunk 60 basis points to 11.6%. The decline was mainly driven by lower sales.

Central Garden & Pet has been witnessing weak margins, and higher selling, general and administrative (SG&A) costs. During the second quarter of fiscal 2023, gross profit decreased 9.5% to $259.6 million. Also, the gross margin shrunk 150 basis points to 28.6%, following a contraction of 260 basis points in the preceding quarter. The decline was driven by the Garden segment due to unfavorable overhead absorption in key garden businesses and input cost pressures. As a percentage of net sales, SG&A expenses increased 110 basis points to 20%. As a result, the operating margin shriveled 260 basis points to 8.6%.

Central Garden & Pet operates in highly-competitive markets and hence faces intense competition from regional and national firms on grounds of price, product quality, number of products offered, brand awareness and customer service.

Conclusion

All the aforesaid negatives make Central Garden & Pet a current Zacks Rank #5 (Strong Sell) stock now. A VGM Score of D further adds to the weakness.

On the positive front, Central Garden & Pet is strengthening its position as one of the leading companies in the U.S. pet supplies and lawn and garden supplies space. Unique packaging, point-of-sale displays, logistic capabilities and a high level of customer service are some of the positives. The company is also making smooth progress on its Central-to-Home strategy. On its lastearnings call management had projected growth in the operating income and EPS during the second half of fiscal 2023.

However, we remain cautious about the stock in the near term given the aforesaid weaknesses.

Eye These Solid Picks

Some better-ranked companies are Royal Caribbean RCL, Crocs CROX and lululemon athletica LULU.

Royal Caribbean sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

RCL has a trailing four-quarter earnings surprise of 26.4%, on average. The Zacks Consensus Estimate for RCL’s 2023 sales and EPS indicates increases of 47.9% and 158.3%, respectively, from the year-ago period’s reported levels.

Crocs, which offers casual lifestyle footwear and accessories, presently carries a Zacks Rank #2 (Buy). The expected EPS growth rate for three to five years is 15%.

The Zacks Consensus Estimate for Crocs’ current financial-year sales and EPS suggests growth of 13.1% and 2.8% from the year-ago period’s reported figure. CROX has a trailing four-quarter earnings surprise of 21.8%, on average.

lululemon athletica is a yoga-inspired athletic apparel company. LULU carries a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for lululemon athletica’s current financial-year sales and EPS suggests growth of 16.7% and 18%, respectively, from the year-ago corresponding figures. LULU has a trailing four-quarter earnings surprise of 9.9%, on average.

Zacks Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

It’s a little-known chemical company that’s up 65% over last year, yet still dirt cheap. With unrelenting demand, soaring 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail investors could jump in at any time.

This company could rival or surpass other recent Zacks’ Stocks Set to Double like Boston Beer Company which shot up +143.0% in little more than 9 months and NVIDIA which boomed +175.9% in one year.

Free: See Our Top Stock and 4 Runners Up >>Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Central Garden & Pet Company (CENT) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.