Boosting shareholders’ wealth, CBRE Group’s CBRE board of directors approved an additional $5 billion increase in the company’s stock repurchase authorization.

This approved expanded authorization supplements CBRE’s existing $4 billion stock repurchase authorization, which had approximately $1.4 billion remaining as of Sept. 30, 2024. Since 2021, CBRE has repurchased 36 million shares at an estimated cost of $3 billion, with a weighted average price of approximately $83.50 per share.

The expanded authorization comes at a crucial time, as the company believes that the current valuation of its shares does not represent its long-term growth potential.

CBRE Group is focused on maintaining a strong financial position. It ended the third quarter of 2024 with more than $4 billion of liquidity. Management expects its free cash flow to be on track to exceed $1 billion this year.

Is it Prudent to Invest in CBRE Stock Now?

CBRE Group is well-positioned to sustain robust earnings and free cash flow growth in the future, supported by its highly resilient and diversified business model. Its initiatives to increase shareholder value reflect the company's strong financial position. The outsourcing business remains healthy, and its pipeline is likely to remain elevated, offering it scope for growth. Strategic buyouts and technology investments are expected to drive its performance.

Analysts seem bullish on this company, with the Zacks Consensus Estimate for its 2024 earnings per share being revised 2.7% upward over the past month to $4.93.

Considering the growth scope, we conclude that the stock indicates a good investment opportunity for investors. Its Zacks Rank #2 (Buy) supports our thesis.

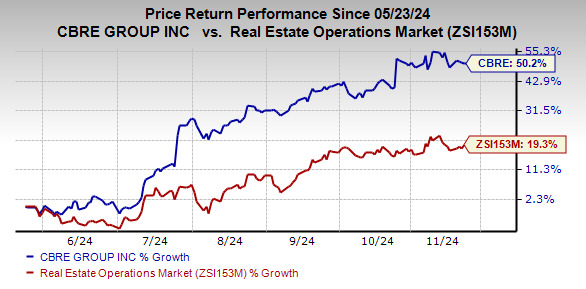

Over the past six months, shares of the company have rallied 50.2% compared with the industry’s upside of 19.3%.

Image Source: Zacks Investment Research

Other Stocks to Consider

Some other top-ranked stocks from the operations real estate industry are Jones Lang JLL and Zillow Group Class C Z, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for JLL’s 2024 earnings per share is pinned at $13.17, suggesting year-over-year growth of 78%.

The Zacks Consensus Estimate for Z’s ongoing year’s earnings per share stands at $1.44, indicating a 14.3% increase from the year-ago reported figure.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpJones Lang LaSalle Incorporated (JLL) : Free Stock Analysis Report

Zillow Group, Inc. (Z) : Free Stock Analysis Report

CBRE Group, Inc. (CBRE) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.