Video game investors haven't enjoyed strong returns lately. Most of the industry players are seeing reduced demand right now as consumers prioritize other entertainment options and move away from the free-spending attitudes that characterized earlier phases of the pandemic.

Take-Two Interactive (NASDAQ: TTWO) and Electronic Arts (NASDAQ: EA) are no exception. The two developers recently reduced short-term growth expectations and announced new cost cuts aimed at protecting profitability. These moves should brighten the long-term outlook for these entertainment giants, which still involves strong industry growth and expanding margins.

With that in mind, let's compare the video game stocks to see which one is a better fit for your portfolio.

The growth matchup

At a glance, Take-Two appears to have stronger momentum. Net bookings, a core sales growth metric, were up 60% in the most recent quarter, compared to EA's 1% decline. This comparison has big limitations, though, as both companies' sales results are extremely lumpy.

EA released a hit title in the Battlefield 2042 franchise a year earlier, for example. And Take-Two's sales benefited from the addition of its recently acquired Zynga portfolio.

The bigger takeaway is that both companies are seeing weaker demand in parts of their portfolios. EA called out softness in the Apex franchise starting in late 2022, and Take-Two in early February noted that gamers were moving away from some of its pricier content.

Still, Take-Two's aggressive acquisition strategy has given it a much faster growth profile for 2023, but with key trade-offs around cash and profits.

Cash and profits

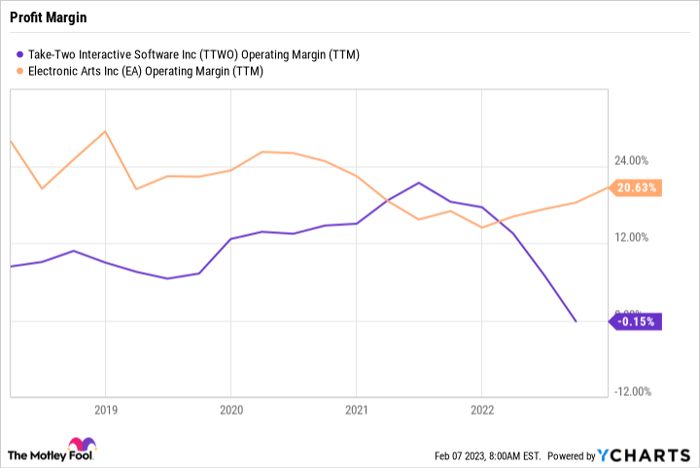

EA easily wins the matchup around its finances. The developer generated $933 million in operating cash flow over the nine months that ended in late December, while Take-Two produced only $36 million.

TTWO Operating Margin (TTM) data by YCharts

Take-Two is also under more profit pressure as it works to integrate the Zynga purchase. Its net loss is expected to reach as high as $4.50 per share in fiscal 2023, while EA is projecting substantial net income between $2.97 and $3.11 per share this year. Based on these metrics, a Take-Two investment seems riskier, especially given the slowdown impacting the industry today.

Valuation

While both video game stocks have become cheaper over the past year, Take-Two's lower valuation reflects the extra risks associated with its losses and weak cash production. There's more uncertainty around how quickly its cost-cutting program can lift margins, while EA has a clearer path toward positive earnings.

You can buy Take-Two stock for about 3.2 times annual sales today, down from a price-to-sales ratio of 6 back in early 2022. EA is trading for 4.3 times sales, also down from 6 a year ago.

Investors willing to take on more risk might prefer Take-Two stock today, but its rebound will depend on cost cuts, the performance of a few big releases this year, and a demand recovery in the mobile and casual gaming niches. EA, in contrast, will likely produce solid earnings in 2023 even as net bookings decline slightly. It also pays a modest dividend, which might help cushion shareholder returns if a recession strikes.

Both companies are likely to be setting sales and earnings records in a few years, but EA offers investors a better balance between risk and reward today.

10 stocks we like better than Electronic Arts

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Electronic Arts wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of January 9, 2023

Demitri Kalogeropoulos has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Take-Two Interactive Software. The Motley Fool recommends Electronic Arts and recommends the following options: long January 2023 $115 calls on Take-Two Interactive Software. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.