Malibu Boats MBUU, a leading designer and manufacturer of sport boats, is bumping into some considerable slowdowns in top and bottom-line expectations, giving it a Zacks Rank #5 (Strong Sell) rating.

The bout of consumer exuberance which followed the Covid-19 lockdown pulled forward considerable buying of large-ticket items like boats. Because of this, sales at Malibu Boats jumped well above trend and while it was welcome at the time, is limiting sales estimates over the next year or two.

As buying a boat is not something that is done regularly, the company is likely to see a slowdown in growth moving forward and should be avoided for now.

Malibu Boats stock has put up a very poor performance thus far in 2024, and it looks like the stock may have further to fall before expectations improve.

Image Source: Zacks Investment Research

Earnings Estimates Continue to Trend Lower for Malibu Boats

The dynamic troubling Malibu Boats has not been missed by analysts, as they have lowered earnings estimates for the company. The earnings revision trend has clearly been trending lower for the last few years, and in just the last week, analysts have again lowered estimates.

Next quarter earnings estimates have been revised lower by 24% and are expected to show a 58% YoY decline.

FY25 earnings estimates have fallen by 8.6% in the last week but are expected to rebound 61% higher by that time.

Current year sales are forecast to fall 40% YoY to $827 million, while current year earnings are projected to crater 77.7%.

Image Source: Zacks Investment Research

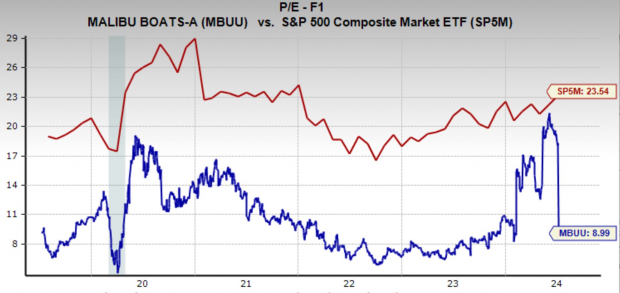

MBUU Valuation Still within Historical Averages

Currently, Malibu Boats is trading at a one year forward earnings multiple of 9x. We can see the earnings multiple plummeted recently from a high of 21x. However, even at this depressed level the stock is still trading around its five-year median of 9.9x.

While Malibu Boats (MBUU) trades at its historical average valuation, the ongoing decline in fundamentals outweighs any potential value proposition. Boat manufacturers typically don't command premium valuations, making MBUU unattractive at this time.

Perhaps at a further discount in the valuation, or a reversal in the earnings revision trend would makes this stock appealing again.

Image Source: Zacks Investment Research

Malibu Boats Stock Price Makes New Lows

We can see that MBUU has been trading in a clear downtrend since its 2021 highs. The price has followed this bearish channel lower over the last three and a half years.

Just this week, Malibu Boats stock flushed to another new low of the year, and four-year low. I would not be surprised to see the price test the lower bound of the channel around $28.

Image Source: TradingView

Bottom Line

Malibu Boats MBUU faces continued headwinds due to a post-pandemic slowdown in demand for its high-ticket boats. This, coupled with declining earnings estimates and a weak stock price performance, makes MBUU a clear avoid for investors at this time.

While the valuation has compressed to historical averages, the ongoing deterioration in fundamentals outweighs any potential value proposition. Investors should consider waiting for a turnaround in the earnings revision trend or a more attractive entry point before considering MBUU.

Infrastructure Stock Boom to Sweep America

A massive push to rebuild the crumbling U.S. infrastructure will soon be underway. It’s bipartisan, urgent, and inevitable. Trillions will be spent. Fortunes will be made.

The only question is “Will you get into the right stocks early when their growth potential is greatest?”

Zacks has released a Special Report to help you do just that, and today it’s free. Discover 5 special companies that look to gain the most from construction and repair to roads, bridges, and buildings, plus cargo hauling and energy transformation on an almost unimaginable scale.

Download FREE: How To Profit From Trillions On Spending For Infrastructure >>Malibu Boats, Inc. (MBUU) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.