Affirm Holdings, Inc. AFRM is scheduled to release first-quarter fiscal 2025 results on Nov. 7, after the closing bell. The Zacks Consensus Estimate for the bottom line is pegged at a loss of 36 cents per share, suggesting a narrower figure than the prior-year quarter’s loss of 57 cents. Its quarterly performance is expected to have been driven by increased merchant network revenues, higher interest income and continued transaction growth undertaken through AFRM’s platform.

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

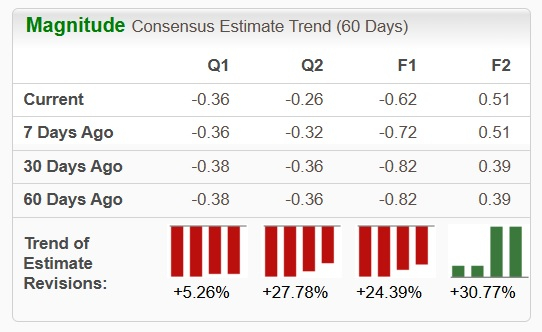

The first-quarter earnings estimate has witnessed two upward estimate revisions over the past 30 days. Meanwhile, the Zacks Consensus Estimate for revenues is $661 million, indicating 33% growth from the year-ago quarter’s figure. Management expects revenues of $640-$670 million.

Image Source: Zacks Investment Research

Earnings Surprise History of AFRM

Affirm’s bottom line beat the consensus estimate in two of the trailing four quarters and missed the mark twice, the average negative surprise being 10.64%. This is depicted in the figure below:

Affirm Holdings, Inc. Price and EPS Surprise

Affirm Holdings, Inc. price-eps-surprise | Affirm Holdings, Inc. Quote

What Our Quantitative Model Unveils for Affirm

Our proven model predicts an earnings beat for Affirm this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here.

Earnings ESP: Affirm has an Earnings ESP of +10.11% because the Most Accurate Estimate of a loss of 32 cents per share is narrower than the Zacks Consensus Estimate of a loss of 36 cents. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

Zacks Rank: AFRM currently sports a Zacks Rank of 1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Key Factors Likely to Influence AFRM’s Q1 Results

Merchant network revenues are likely to have benefited on the back of an expanding Gross Merchandise Volume (GMV), which in turn, is expected to have received an impetus from strength in general merchandise and travel and ticketing categories. The Zacks Consensus Estimate for merchant network revenues is pegged at $194.2 million, indicating a 33% rise from the prior-year quarter’s figure.

The consensus mark for GMV is pegged at $7.3 billion, which implies nearly 30% growth from the prior-year quarter’s number. Management anticipates the metric to be in the range of $7.1-$7.4 billion.

An increase in the number of transactions conducted through the Affirm platform is likely to have boosted active merchants and consumers. The Zacks Consensus Estimate for active consumers indicates 13.5% year-over-year growth.

Increase in usage of Affirm’s virtual cards is expected to have driven card network revenues. The consensus mark for card network revenues is pegged at $42.9 million, indicating 28.2% improvement from the prior-year quarter’s number.

Meanwhile, interest income is likely to have received an impetus from the pricing initiatives undertaken by the company and increase in loans held for investment. The Zacks Consensus Estimate for interest income is $348 million, which implies a 32.5% year-over-year rise. A growing figure of loans sold is likely to have contributed to servicing income.

The consensus mark for servicing income is pegged at $29.3 million, which indicates a 45.4% surge from the prior-year quarter.

However, the quarterly results are likely to have witnessed higher transaction costs. The company expects transaction costs to be in the range of $375-$390 million, which remain higher than the year-ago level of $284 million. In addition to this, operating expenses are likely to have witnessed an increase due to higher processing and servicing and funding costs, along with an increase in the provision for credit losses. This, in turn, is expected to have inflicted pressure on margins.

AFRM Stock’s Price Performance & Valuation

Affirm’s shares have lost 11.1% year to date against the industry’s 13.7% growth. It has also underperformed the broader Zacks Business Services sector’s 14.3% rise and the S&P 500 index’s 20.1% increase in the said time frame. In comparison with AFRM, two of its industry peers, Mastercard Incorporated MA and Visa Inc. V have gained 18.6% and 12.1%, respectively, in the same timeframe.

Year-to-Date Price Performance

Image Source: Zacks Investment Research

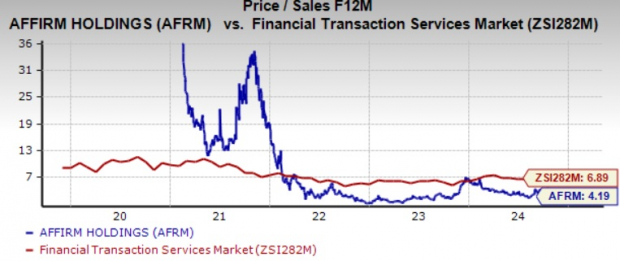

Now, let’s look at the value Affirm offers investors at current levels.

The company is cheaply priced compared with the industry average. Currently, AFRM is trading at 4.19X forward 12-months sales, below the industry’s average of 6.89X.

Image Source: Zacks Investment Research

Assessing Affirm’s Prospects

Affirm’s robust revenue growth is driven by an expanding merchant network, increased card adoption and strong GMV, which is projected to surpass $33.5 billion in fiscal 2025. Partnerships with brands like Apple Pay, Hotels.com and Peloton have broadened its reach across sectors. Product innovations, including Pay in 2 and Pay in 30, diversify its payment options, while international expansion plans into the U.K. aim to drive growth.

However, escalating funding costs, provision for credit losses, and processing and servicing expenses will keep margins under pressure. High leverage also remains a concern.

Conclusion

Although Affirm faces challenges such as an elevated operating expense level, a growing active merchant network and expanding GMV make it an appealing investment option at present. AFRM’s relatively lower valuation compared with the industry further enhances its attractiveness as a buy.

Though the company’s price performance has been under pressure year to date, improved interest income and continued spending in travel and ticketing categories are likely to provide some respite to investors. Therefore, with another expected earnings beat around the corner, it remains a solid long-term investment pick.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 228 positions with double- and triple-digit gains in 2023 alone.

See Stocks Now >>Mastercard Incorporated (MA) : Free Stock Analysis Report

Visa Inc. (V) : Free Stock Analysis Report

Affirm Holdings, Inc. (AFRM) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.