Adobe (NASDAQ: ADBE) is still benefiting from a stampede toward digital content creation. That was the main takeaway from the software giant's fiscal first-quarter results, which cover the selling period through early March.

Adobe's expansion pace implies another year of sales and earnings gains even following record growth in 2021. Yet those spikes will be weaker than investors have seen in a few years. And Adobe reduced a few of its 2022 targets slightly to account for changes in the geopolitical and economic climates.

Let's dive right in and take a closer look at what was reported.

Image source: Getty Images.

Winning in the cloud

Revenue for the quarter hit a record $4.36 billion, which edged just past the forecast that management issued in mid-December. That translated into 17% growth after adjusting for an extra selling week in the year-ago period. Adobe grew at a 21% rate in the previous quarter, for context.

Each of its three main business lines expanded thanks to high demand for its software-as-a-service products. Adobe's subscription-based revenue grew to $4 billion from $3.6 billion and represents essentially all of its sales today. "Adobe achieved record first-quarter revenue as Creative Cloud, Document Cloud, and Experience Cloud continue to be pivotal in driving the digital economy," CEO Shantanu Narayen said in a press release.

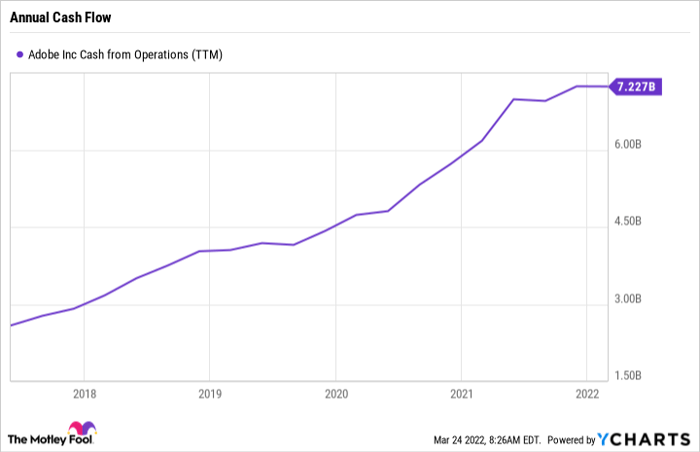

The finances

Adobe's results showcased the financial power of that subscription selling model. Operating margin was a blistering 37% of sales, consistent with the prior year's level. Operating cash flow held steady, too, at a healthy $1.8 billion.

ADBE cash from operations (TTM). Data by YCharts. TTM = trailing 12 months.

Adobe achieved these gains through what management called a "challenging macroeconomic and geopolitical environment." Demand was disrupted in a few markets, especially Russia, Ukraine, and Belarus.

Growth also slowed in other geographies compared to booming results a year ago. However, management is confident that the long-term trends are positive. "We are witnessing the digitization of everything, and Adobe's products offer customers access to a digital future underpinning how they live and work," executives said.

Looking ahead

Executives said geopolitical disruptions will pressure sales by about $75 million this fiscal year. Their broader outlook was consistent with management's recent comments yet reflects slowing growth ahead. Its three divisions will grow by between 14% and 18% in the second quarter, for example, while each segment expanded at an over 20% pace in the first quarter and throughout fiscal 2021.

Investors shouldn't see that slowdown as a surprise or a sign of weaker demand. On the contrary, Adobe has a good shot at expanding its customer base and building average contract spending. Fiscal 2022 will be another busy year for additions to its platform and new product launches, which have been proven to boost sales and profitability.

Looking further out, Adobe is targeting a big piece of a massive digitization market that will allow it to potentially reach $20 billion in annual sales. Fiscal 2022 will likely represent a smaller step toward that figure than shareholders saw last year. But Adobe is still in an ideal position to capitalize on the digital transformation trend over the next decade.

10 stocks we like better than Adobe Inc.

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Adobe Inc. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of March 3, 2022

Demitri Kalogeropoulos has no position in any of the stocks mentioned. The Motley Fool recommends Adobe Inc. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.