Zscaler, Inc. ZS is seeing strong traction from its Z-Flex program, and this offering could become an important driver of future growth. Z-Flex allows customers to commit to a spending level upfront while keeping flexibility to add or swap modules later. This model reduces procurement delays and helps the company win larger multi-year deals.

Introduced in the third quarter of fiscal 2025, Z-Flex already delivered more than $175 million in total contract value bookings in the first quarter of fiscal 2026, a 70% sequential increase. This sharp increase signals rising customer interest in flexible licensing rather than traditional product-by-product purchases. As Z-Flex agreements often run for longer periods, they also improve revenue visibility.

The program is helping Zscaler expand relationships with existing clients. Some large enterprises increased annual spending significantly after adopting multiple modules under Z-Flex. This cross-selling effect is important because the company’s strategy depends on platform adoption across zero trust, data security and AI security offerings.

Z-Flex may also support deal size growth. Customers are more willing to commit to broader deployments when they know they can adjust product choices later. That reduces hesitation during negotiations and can speed up sales cycles. For example, a large aerospace company added nine new modules in a multi-year, eight-figure deal in the first quarter of fiscal 2026. The deal increases Zscaler’s annual recurring revenues (ARR) with the company by more than 40%.

Z-Flex program’s early traction suggests it is strengthening Zscaler’s enterprise expansion story. If adoption translates into higher recurring revenue and retention, Z-Flex could become a durable growth engine for the company. The Zacks Consensus Estimate for Zscaler’s fiscal 2026 and 2027 revenues indicates year-over-year growth of 23.2% and 19.8%, respectively.

Zscaler’s Rivals With Similar Bundled Offerings

Zscaler faces intense competition from Palo Alto Networks, Inc. PANW and CrowdStrike Holdings, Inc. CRWD, which have similar platform-driven growth strategies. Both companies are using flexible bundles and integrated platforms to expand customer spending.

Palo Alto Networks focuses on subscription pricing and bundled offerings that combine firewalls, cloud security and XDR tools into integrated suites. These bundles can deliver 10–15% savings versus buying products separately, which encourages customers to adopt Palo Alto Networks’ broader platform packages rather than single solutions.

CrowdStrike Holdings uses a similar expansion strategy through its Falcon platform bundles and the Falcon Flex licensing model. These models allow customers to add modules without new procurement cycles. In the third quarter of fiscal 2026, ARR from CrowdStrike Holdings’ Falcon Flex customers reached $1.35 billion, growing more than 200% year over year.

Zscaler’s Price Performance, Valuation and Estimates

Shares of Zscaler have plunged 14.8% over the past year compared with the Zacks Security industry’s decline of 15.6%.

Zscaler One-Year Price Return Performance

Image Source: Zacks Investment Research

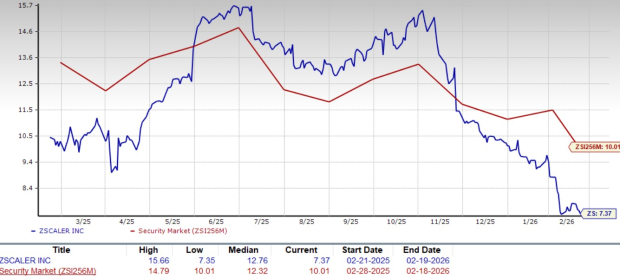

From a valuation standpoint, ZS trades at a forward price-to-sales ratio of 7.37, significantly below the industry’s average of 10.01.

Zscaler Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

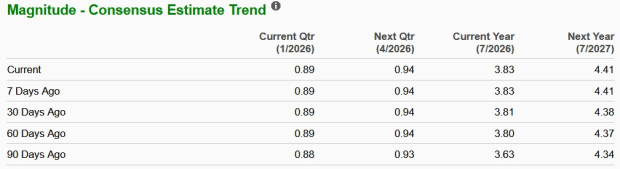

The Zacks Consensus Estimate for Zscaler’s fiscal 2026 and 2027 earnings implies a year-over-year increase of 16.8% and 15.3%, respectively. Estimates for fiscal 2026 and 2027 have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Zscaler currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Palo Alto Networks, Inc. (PANW) : Free Stock Analysis Report

Zscaler, Inc. (ZS) : Free Stock Analysis Report

CrowdStrike (CRWD) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.