Snap-on Incorporated SNA is making solid progress on its strategic priorities. SNA’s strengths are rooted in its powerful brand, differentiated business model and strong customer relationships. The company benefits from a well-established franchise network that enables direct, frequent engagement with repair professionals, allowing it to closely align product development with customer needs.

SNA has been enhancing the franchise network, improving relationships with repair shop owners and managers, and expanding into critical industries in emerging markets. Management’s emphasis on the RCI process has been on track. The RCI process is designed to enhance organizational effectiveness and minimize costs, along with helping Snap-on to boost sales and margins and generate savings. Savings from the RCI initiative reflect gains from the continuous productivity and process improvement plans.

Snap-on is witnessing robust business trends, supported by the increasing complexity of modern vehicles. New models entering the market feature advanced drivetrains, evolving motor configurations and sophisticated electrical architectures that integrate a neural network of sensors, enabling driver-assisted autonomy. It remains focused on strengthening customer connections and driving innovation. Management continues to expect a resilient vehicle repair market, as the growing technological complexity of vehicles sustains demand for specialized tools, diagnostics and repair solutions.

Snap-on is well-positioned, supported by its innovative hardware offerings, particularly its proprietary and comprehensive database. The company’s specialty torque business within the Commercial & Industrial Group continues to progress steadily. It is also benefiting from a robust pipeline of new products, including its heavy-duty cordless torque multiplier, the CTM 800, which delivers torque starting at 160 foot-pounds expands its capabilities across higher torque applications.

Management expects SNA’s markets and operations to have considerable resilience against the uncertainties of the operating landscape. It anticipates continued progress by leveraging capabilities in the automotive repair arena, as well as expanding its customer base in automotive repair and across geographies, including critical industries. Such strengths are likely to bolster sales and profits.

SNA’s Price Performance, Valuation and Estimates

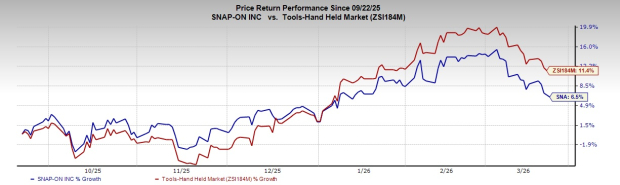

Shares of Snap-on have gained 6.5% in the past six months compared with the industry’s growth of 11.4%.

Image Source: Zacks Investment Research

From a valuation standpoint, SNA trades at a forward price-to-earnings ratio of 17.93X compared with the industry’s average of 18.54X.

Image Source: Zacks Investment Research

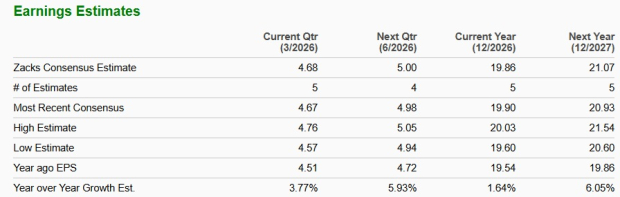

The Zacks Consensus Estimate for SNA’s 2026 and 2027 earnings indicates a year-over-year rise of 1.6% and 6.1%, respectively. The company’s EPS estimate for 2026 and 2027 has moved down in the past 30 days.

Image Source: Zacks Investment Research

Snap-on stock currently carries a Zacks Rank #3 (Hold).

Key Picks in the Consumer Discretionary Space

Crocs, Inc. CROX, which is a leading footwear company, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

CROX delivered a trailing four-quarter earnings surprise of 16.6%, on average. The Zacks Consensus Estimate for Crocs’ current financial-year EPS indicates a rise of 7.2% from the year-ago number.

Ralph Lauren RL, which is a designer and marketer of premium lifestyle products, currently carries a Zacks Rank #2 (Buy).

RL delivered a trailing four-quarter earnings surprise of 9.7%, on average. The Zacks Consensus Estimate for Ralph Lauren’s current financial-year EPS indicates growth of 31.8% from the year-ago number.

Kontoor Brands, Inc. KTB, which is an apparel company, currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for KTB’s current financial-year EPS is expected to rise 15.6% from the corresponding year-ago reported figure. KTB delivered a trailing four-quarter earnings surprise of 13.9%, on average.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpSnap-On Incorporated (SNA) : Free Stock Analysis Report

Ralph Lauren Corporation (RL) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report

Kontoor Brands, Inc. (KTB) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.