Pitney Bowes Inc. PBI appears to be positioning its shipping software business as a key growth driver. Recent management commentary suggests it could become the company’s next major growth engine. While traditional mailing operations continue to face secular pressures, the company is seeing encouraging momentum in software subscriptions, bookings and customer acquisition efforts.

During the first-quarter 2026earnings call CEO Kurt Wolf highlighted shipping software as the area with the greatest growth potential within the SendTech segment. Management is simplifying its portfolio of software offerings, reducing customer confusion and focusing resources on enhancing the most promising products. The company is also shifting toward a customer-centric development strategy, prioritizing features and services that directly address client needs rather than leading with technology alone.

Early signs of progress are already emerging. Pitney Bowes reported its first year-over-year increase in bookings in some time, while enterprise software subscriptions improved as sales teams exceeded targets. Management noted that stronger bookings not only support current revenues but also create recurring “stream” revenue opportunities in future periods through shipping-label and software-related services.

A unique advantage for Pitney Bowes is its banking operation. The company plans to leverage the bank to offer financing solutions and other value-added services to shipping software customers. Management believes this differentiates PBI from competitors, as few rivals possess an in-house banking platform capable of supporting customer cash-flow needs and providing attractive financing options.

While management remains cautious about predicting a precise timeline for accelerated growth, the combination of improving sales execution, rising subscriptions, streamlined products and banking-related opportunities suggests shipping software could become an increasingly important contributor to Pitney Bowes’ long-term growth strategy.

PBI’s Stock Price Performance & Valuation Trend

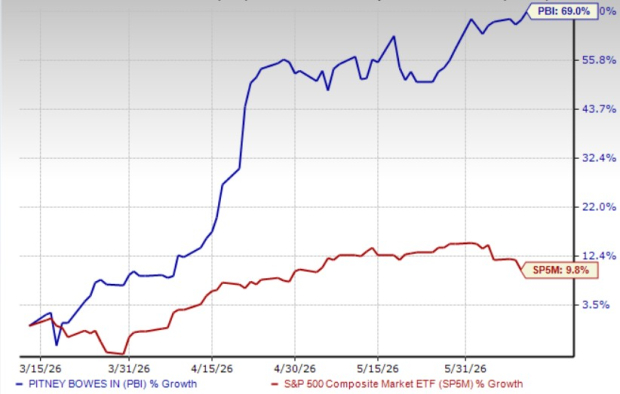

Shares of Pitney Bowes have increased 69% in the past three months, outperforming the S&P 500’s 9.8% rise. In the same time frame, other industry players like FedEx FDX and United Parcel Service UPS have declined 3.9% and increased 11.7%, respectively.

Price Performance

Image Source: Zacks Investment Research

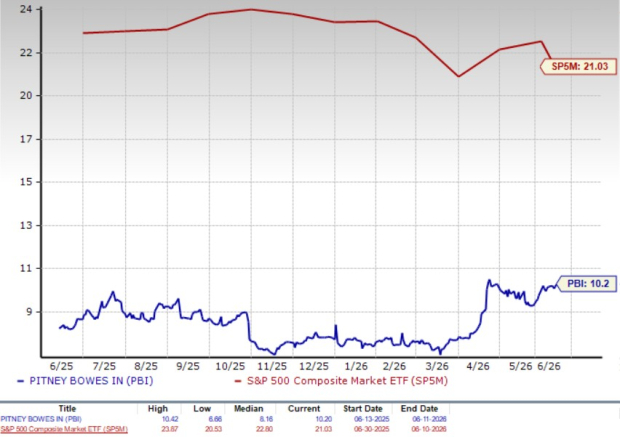

PBI stock is currently trading at a discount compared with the S&P 500, with a forward 12-month price-to-earnings (P/E) ratio of 10.2, as evidenced by the chart below. Conversely, industry players, such as FedEx and United Parcel Service, have P/E multiples of 15.65 and 14.57, respectively.

P/E (F12M)

Image Source: Zacks Investment Research

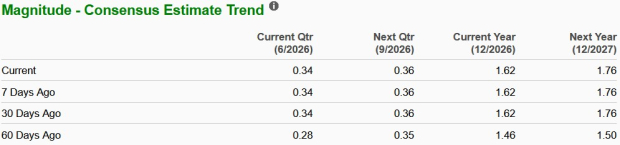

Earnings Estimate Revision of PBI

PBI’s earnings estimates for 2026 and 2027 have trended upward in the past 60 days to $1.62 and $1.76 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 20% and 8.4%, respectively.

Image Source: Zacks Investment Research

PBI currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>United Parcel Service, Inc. (UPS) : Free Stock Analysis Report

Pitney Bowes Inc. (PBI) : Free Stock Analysis Report

FedEx Corporation (FDX) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.