Bristol Myers BMY recently secured a meaningful label expansion for Sotyktu, with the FDA approving the drug for adults with active psoriatic arthritis (PsA). The decision adds a second major indication beyond plaque psoriasis, strengthening the product’s long-term commercial profile and lifecycle potential.

From an investment standpoint, this approval introduces a differentiated, oral therapy into a large and competitive PsA market historically dominated by injectable biologics.

Sotyktu’s position as the first TYK2 inhibitor approved for PsA could support uptake, particularly among patients and physicians seeking convenient, non-biologic options earlier in the treatment paradigm.

Strategically, the label expansion reinforces Bristol Myers’ immunology franchise and diversifies revenue streams beyond oncology. With psoriatic arthritis affecting a meaningful subset of psoriasis patients, Sotyktu now addresses both skin and joint manifestations, increasing its addressable market and cross-selling potential within existing dermatology and rheumatology channels.

However, commercial execution will be key. The PsA market is highly competitive, with entrenched biologics and oral agents already available.

Overall, the PsA approval represents a catalyst for BMY, enhancing Sotyktu’s growth outlook and supporting a broader shift toward immunology as a durable revenue pillar.

BMY is working on the label expansion of its drugs to strengthen its growth portfolio, which primarily comprises Opdivo, Orencia, Yervoy, Reblozyl, Opdualag, Abecma, Zeposia, Breyanzi, Camzyos, Sotyku, Krazati and others.

The drug raked in sales of $291 million in 2025, up 19% from 2024. Sotyktu is also being evaluated for lupus (data is expected later in the year) and Sjogren’s Disease.

Schizophrenia drug Cobenfy is being evaluated for psychosis associated with Alzheimer's disease, for agitation in Alzheimer's Disease and Alzheimer's Disease cognition.

The successful development of all late-stage pipeline candidates and label expansion of approved drugs should be a significant boost for BMY as its legacy portfolio continues to be adversely impacted by the continued generic impact on Revlimid, Pomalyst, Sprycel and Abraxane.

Competition for BMY’s Sotyktu

Sotyktu faces stiff competition from Amgen’s AMGN Otezla in the psoriasis space.

Amgen acquired global commercial rights to Otezla from erstwhile Celgene (now part of Bristol-Myers). Amgen is also evaluating Otezla in additional indications.

Novartis’ NVS blockbuster drug Cosentyx is approved for various conditions like hidradenitis suppurativa, psoriatic arthritis, plaque psoriasis, ankylosing spondylitis, and non-radiographic axial spondyloarthritis, as well as several pediatric inflammatory disorders.

Cosentyx is a fully human monoclonal antibody that blocks interleukin-17A, a cytokine involved in inflammatory pathways underlying several immune-mediated diseases.

It is one of the top drugs for NVS. The drug generated $6.7 billion in revenues for NVS in 2025, representing 8% growth from 2024.

BMY’s Price Performance, Valuation & Estimates

Shares of Bristol Myers have lost 4.8% over the past year against the industry’s growth of 11.2%.

Image Source: Zacks Investment Research

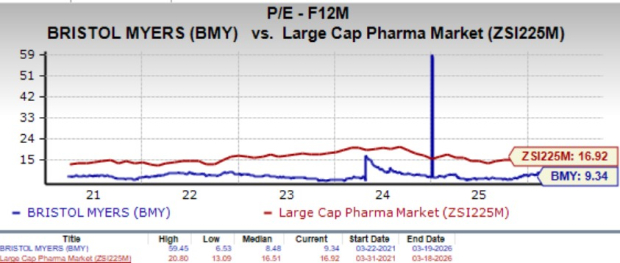

From a valuation standpoint, BMY is trading at a discount to the large-cap pharma industry. Going by the price/earnings ratio, the stock currently trades at 9.34x forward earnings, higher than its mean of 8.48x but lower than the large-cap pharma industry’s 16.92x.

Image Source: Zacks Investment Research

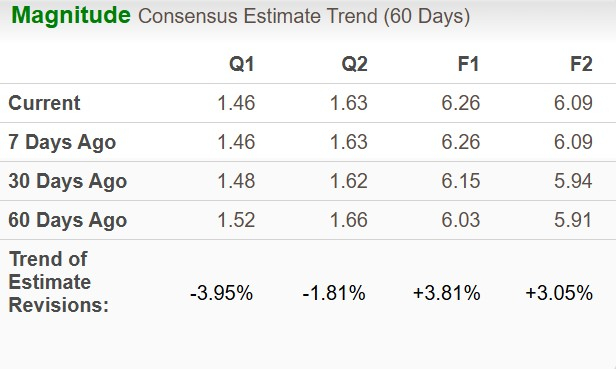

The Zacks Consensus Estimate for 2026 EPS has moved north to $6.26 from $6.15 in the past 30 days, while that for 2027 has increased to $6.09 from $5.94.

Image Source: Zacks Investment Research

BMY currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpNovartis AG (NVS) : Free Stock Analysis Report

Bristol Myers Squibb Company (BMY) : Free Stock Analysis Report

Amgen Inc. (AMGN) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.