Dycom Industries, Inc. DY is going strong through fiscal 2026 with solid margins reflecting operational discipline, favorable pricing strategy and robust market trends, which are expected to continue into fiscal 2027. In the first nine months of fiscal 2026, its adjusted EBITDA increased year over year by 25.1% to $575.3 million, with adjusted EBITDA margin expanding 140 basis points (bps) to 14.1%.

Despite ongoing labor and equipment cost pressures across the construction and telecom services space, DY’s emphasis on selective bidding and holding onto higher-margin projects is keeping the trend afloat. A backlog of $8.22 billion, with nearly $5 billion expected to convert within the next 12 months, gives the company leverage in customer negotiations, allowing it to price projects in a way that reflects rising complexity, tighter labor markets and higher safety and compliance standards. Moreover, the positive trend across a strong public infrastructure funding environment and the optimism surrounding the Broadband Equity, Access and Deployment (BEAD) program also bodes well.

Importantly, margin expansion in fiscal 2027 does not depend solely on revenue growth but also on pricing discipline. Demand visibility is high, competition remains rational for large, complex programs and customers increasingly value execution certainty over lowest-cost bids. While weather, timing of BEAD awards and customer capital pacing remain variables, Dycom’s current margin trajectory indicates that disciplined pricing, supported by backlog strength and operational scale, can continue to push profitability higher.

The current approach positions Dycom not just for growth, but for stronger and more resilient margins through fiscal 2027 and beyond.

Earnings Estimate Trend Favors Dycom

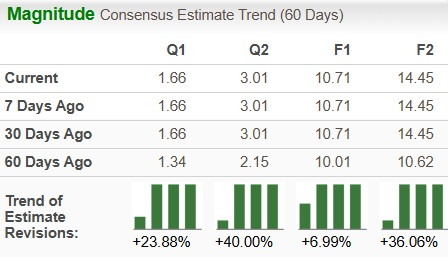

Dycom’s earnings estimates for fiscal 2026 and fiscal 2027 have trended upward over the past 60 days. The estimated figures for fiscal 2026 and fiscal 2027 imply year-over-year growth of 26.9% and 35%, respectively.

Image Source: Zacks Investment Research

The robust market fundamentals and DY’s strategic in-house capabilities likely induced bullish sentiments among analysts.

Dycom’s Competitive Position

Dycom is emerging as one of the most direct beneficiaries of the next multi-year U.S. fiber and digital infrastructure build cycle. However, this does not alter the competitive aspect in this vast market with key players, including EMCOR Group, Inc. EME and Quanta Services, Inc. PWR.

EMCOR is strongest inside the data center footprint, particularly in mechanical and electrical systems, but has limited exposure to outside-plant fiber networks and BEAD-funded rural broadband. Contrastingly, Quanta offers a broader scale and deeper exposure to power transmission, renewable energy and long-haul infrastructure. Quanta’s advantage is resilience across cycles, but its upside from BEAD and last-mile fiber is less concentrated than Dycom’s.

Summing up, Dycom stands out as the most leveraged pure-play on U.S. fiber expansion, BEAD funding and hyperscaler-driven data center networking. On the other hand, its peers EMCOR and Quanta offer broader, but less targeted, infrastructure exposure.

DY Stock’s Price Performance & Valuation Trend

Shares of this specialty contracting firm, operating in the telecom industry, have surged 33.6% in the past six months, outperforming the Zacks Building Products - Heavy Construction industry, the broader Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

DY stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 23.76, as evidenced by the chart below.

Image Source: Zacks Investment Research

Dycom stock currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

Download Atomic Opportunity: Nuclear Energy's Comeback free today.Quanta Services, Inc. (PWR) : Free Stock Analysis Report

EMCOR Group, Inc. (EME) : Free Stock Analysis Report

Dycom Industries, Inc. (DY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.