NVIDIA Corporation NVDA is set to report its third-quarter fiscal 2026 results on Nov. 19, and it would be no surprise that the company would reach another milestone in sales and surpass the $54 billion target. NVDA has been setting new sales records for the past few quarters. In the last reported financial results for the second quarter of fiscal 2026, its revenues reached a new record of $46.74 billion, reflecting a 56% year-over-year increase.

NVIDIA is optimistic that the growth momentum will continue as it targets another record revenues of $54 billion in the third quarter. The key driver behind this outlook is its booming data center business, which continues to power the company’s growth amid the global buildout of AI infrastructure.

In the second quarter of fiscal 2026, the data center business unit reported $41.1 billion in revenues, up 56% from last year, fueled by strong demand from hyperscalers, artificial intelligence (AI) model developers and enterprise customers expanding their AI infrastructure.

The ongoing ramp-up of the Blackwell architecture is central to NVIDIA’s momentum. The GB300 systems, which offer higher performance and improved energy efficiency compared to the previous Hopper generation, are now shipping in large volumes. Customers are using these systems to support complex AI workloads, from large language models to real-time inference. NVIDIA’s full-stack approach, which combines graphics processing units (GPUs), networking and software, continues to make it the preferred partner for large-scale AI projects.

The growing demand for the company’s AI chips used in data centers is likely to continue aiding its overall top-line performance. Analysts’ projections also suggest that the company is expected to surpass the third-quarter sales target of $54 billion. The Zacks Consensus Estimate for third-quarter fiscal 2026 revenues is currently pegged at $54.59 billion, indicating a year-over-year increase of 55.6%.

NVIDIA’s Rivals in the AI Data Center Space

Advanced Micro Devices, Inc. AMD and Intel Corporation INTC are two major companies that are competing closely with NVIDIA in the AI data center space.

Advanced Micro Devices is gaining traction with its MI300 series accelerators, which are designed to handle training and inference for large AI models. AMD’s chips have attracted interest from major cloud providers seeking diversification beyond NVIDIA’s ecosystem. While Advanced Micro Devices’ software stack is still developing, its performance and pricing advantages make it a credible alternative.

Intel is also reasserting its presence with the Gaudi series of AI accelerators. The company is positioning Gaudi3 as a cost-effective and scalable option for AI data centers, targeting enterprise clients looking for flexibility. Intel’s broad reach in CPUs and server infrastructure helps it integrate AI solutions more easily into existing systems.

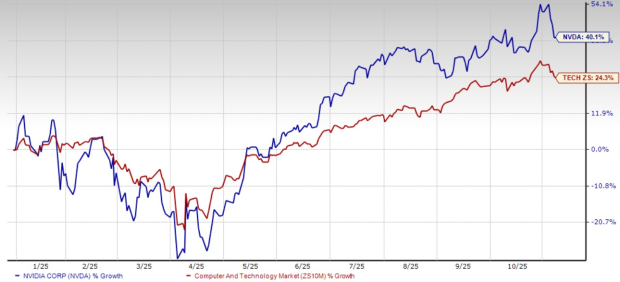

NVIDIA’s Price Performance, Valuation and Estimates

Shares of NVIDIA have risen around 40.1% year to date compared with the Zacks Computer and Technology sector’s gain of 24.3%.

NVIDIA YTD Price Return Performance

Image Source: Zacks Investment Research

From a valuation standpoint, NVDA trades at a forward price-to-earnings ratio of 32.26, higher than the sector’s average of 28.65.

NVIDIA Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for NVIDIA’s fiscal 2026 and 2027 earnings implies a year-over-year increase of approximately 49.2% and 40%, respectively. Estimates for fiscal 2026 and 2027 earnings have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

NVIDIA currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

Download Atomic Opportunity: Nuclear Energy's Comeback free today.Intel Corporation (INTC) : Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD) : Free Stock Analysis Report

NVIDIA Corporation (NVDA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.