Credit: Shutterstock photo

Credit: Shutterstock photoBy Morningstar :

By Samuel Lee

For the past three decades, the rich world rode high a tide of debt-fueled prosperity. The financial crisis spurred U.S. households and firms to chip away at their debts. The eurozone crisis is doing the same to European governments. In the past--notably the 1930s' United States and 1990s' Japan--deleveragings of this magnitude took a decade or so to work through. They were punctuated by false dawns, tremendous volatility and sluggish growth. In this macroeconomic context, strategies less dependent on robust growth and steady markets make sense. The best of the lot: PowerShares S&P 500 Low Volatility ( SPLV ).

It implements a simple low-volatility strategy for a more-than-reasonable 0.25% expense ratio. Each quarter the fund sorts S&P 500 stocks by their trailing 12-month volatilities, picks the 100 least volatile, and weights them by the inverse of their volatilities. SPLV is laden with the boring, such as utilities and consumer staples firms. The strategy delivered steady returns during last year's volatility.

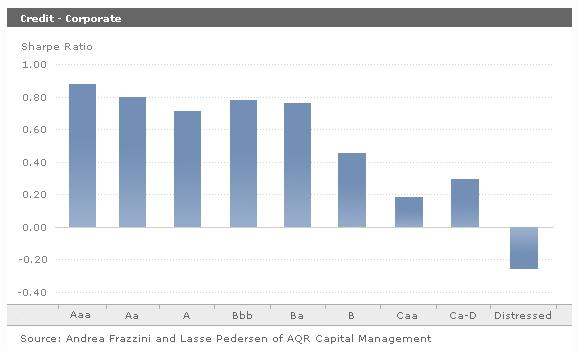

Low Volatility Everywhere

It wasn't a fluke. Over the past 50 years, low-volatility stocks have performed about as well as the U.S. market but with far less risk. They've also outperformed in most international markets. In fact, researchers Lasse Pedersen and Andrea Frazzini found superior risk-adjusted (and sometimes absolute) performance for low-volatility strategies in wide-ranging asset classes, including corporate bonds, Treasuries, currencies, and commodities.

click to enlarge

Researchers have come up with several explanations for why low-volatility strategies post such great risk-adjusted returns. The most convincing involves leverage aversion. Investors who target above-market returns may be unwilling or unable to use leverage to reach their expected-return targets. By resorting to volatile assets (more accurately, high-beta assets), which theoretically should outperform less-volatile assets, they hope to earn above-average profits. Ironically, their collective bet on high-beta leads to low risk-adjusted returns.

High Volatility Headwinds

In case the ubiquity of low-volatility strategies' superior risk-adjusted performances isn't enough, let's expand the case for long-term volatility in the markets. Several factors will slow down the rich world's growth over the medium- and long-term: deleveraging, debt, and demographics.

First, consumers and banks are busy winding down debts, or deleveraging, at the same time; the result is a balance-sheet recession, a rare and long-lived situation that puts the economy is a fragile state. Low demand means businesses will have a hard time growing their profits, while governments take in less revenue and run deficits. In the past, political considerations and inexperience with the unusual properties of balance-sheet recessions have induced governments and central banks to tighten prematurely fiscal and monetary policy, prolonging the pain.

Second, even if governments continue to support growth with deficit spending, growing government debt load presages higher taxes for everyone, meaning, again, lower earnings for investors. If the debt burden gets high enough, equity investors can suffer in many different ways. There's the printing press, the first and last resort of bankrupt sovereigns. Unexpected inflation, if high enough, hurts equity investors. There's also the possibility of a run on even more sovereign debts.

Finally, the rich world is graying. This is bad for equities for several reasons. The welfare state has promised free health care to retiring baby boomers, unfunded promises that look unsustainable. This is new territory; the world has never promised so much money to retirees while simultaneously experiencing a steep, coordinated decline in the ratio of workers to retirees. Aggravating potential volatility is the upward pressure on the equity risk premium, or the reward investors' demand for taking on stock risk. As investors age, they become more risk-averse, meaning they'll demand higher future expected returns from risk assets. This will pressure equity prices down in order to bring their yields up to acceptable levels.

Other Options

SPLV isn't the only low-volatility strategy. IShares and Russell have a slew of them, too. However, SPLV is the most transparently designed and simple, two qualities I hold dear. It's also the biggest of the bunch by assets, a big advantage when it comes to liquidity.

Regardless of how you actually implement a low-volatility strategy, it's important to stick to it for the long run--decades, really. Like any strategy, it won't clock consistent market-beating returns. While the strategy has the happy coincidence of theory, data, and good prospects backing it, our enthusiasm is based on the long-run view, not last year's happy returns.

Disclosure: Morningstar licenses its indexes to certain ETF and ETN providers, including BlackRock, Invesco, Merrill Lynch, Northern Trust, and Scottrade for use in exchange-traded funds and notes. These ETFs and ETNs are not sponsored, issued, or sold by Morningstar. Morningstar does not make any representation regarding the advisability of investing in ETFs or ETNs that are based on Morningstar indexes.

See also Wednesday Options Recap on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}