What’s Driving the Growth in Options Trading

Stock and options markets have both seen consistent increases in liquidity over the past 30 years as automation reduces costs, improves position hedging for professionals and expands accessibility to more investors.

We spend a lot of time explaining how stock markets and trading of stocks and exchange-traded funds (ETFs) work. Today we look at what makes equity options markets different from stock markets.

What makes options markets different from stocks?

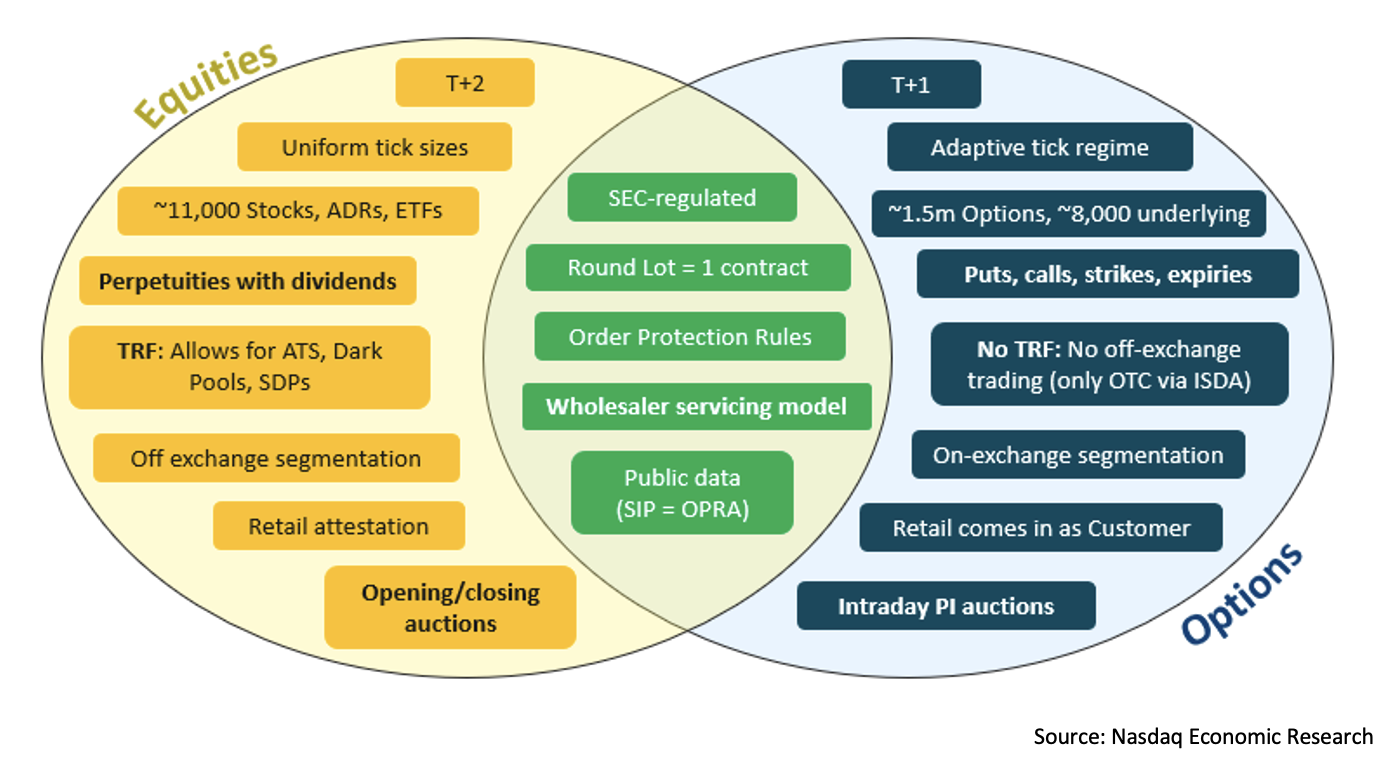

Stocks, equity options, and corporate bonds are all “securities” under the law and, therefore, governed by the U.S. Securities and Exchange Commission (SEC). Although equity options provide exposure to stock underlying, the details of how the markets work are, in many ways, very different.

For instance:

- Apple, the stock, has one ticker (AAPL) that represents a company’s earnings and dividends to perpetuity.

- But for AAPL, options markets have many types of securities you can trade AAPL in, such as:

- Puts (to protect against price falls),

- Calls (to participate in price rises),

- Expiries (dates where the option ends, ranging from a few weeks to a few years),

- Strikes (representing the price AAPL needs to be under (or over) for puts (or calls) to be “in-the-money.”) The stock price relative to the strike determines what the returns are on the option at expiry.

Consequently, there are many more instruments (options strikes) for a market maker to quote in options (around 1.5 million) than in stocks (around 10,000). This results in options markets producing the majority of market data overall.

Options markets also have a shorter settlement period than stocks (at least for now) and dynamic ticks (already).

However, executions in the listed options markets in the U.S. take place on exchange. There is no Trade Reporting Facility (TRF) like there is for U.S. equities. That makes retail trade on exchange, in contrast to how retail is traded bilaterally and off-exchange in stocks. Although institutions still trade OTC (using ISDA’s) and retail investors are still segmented when they trade on exchange, many retail orders trade in intraday price-improvement auctions that may have inspired the SEC’s new auction rules.

Figure 1: Similarities and differences between stock and options markets

A lot of venue competition is also a hallmark of equity and equity options markets. There are currently 16 stock exchanges and 16 different option exchanges competing for orders, including venues run by Nasdaq, Cboe and the New York Stock Exchange.

That’s in contrast to futures markets, where trading is much more centralized and mostly done on the CME and ICE futures markets. Although those markets offer options on equity index futures, those instruments are not part of the SEC-regulated equity and options markets and are not included in the data below.

What options have been driving the increase in overall activity?

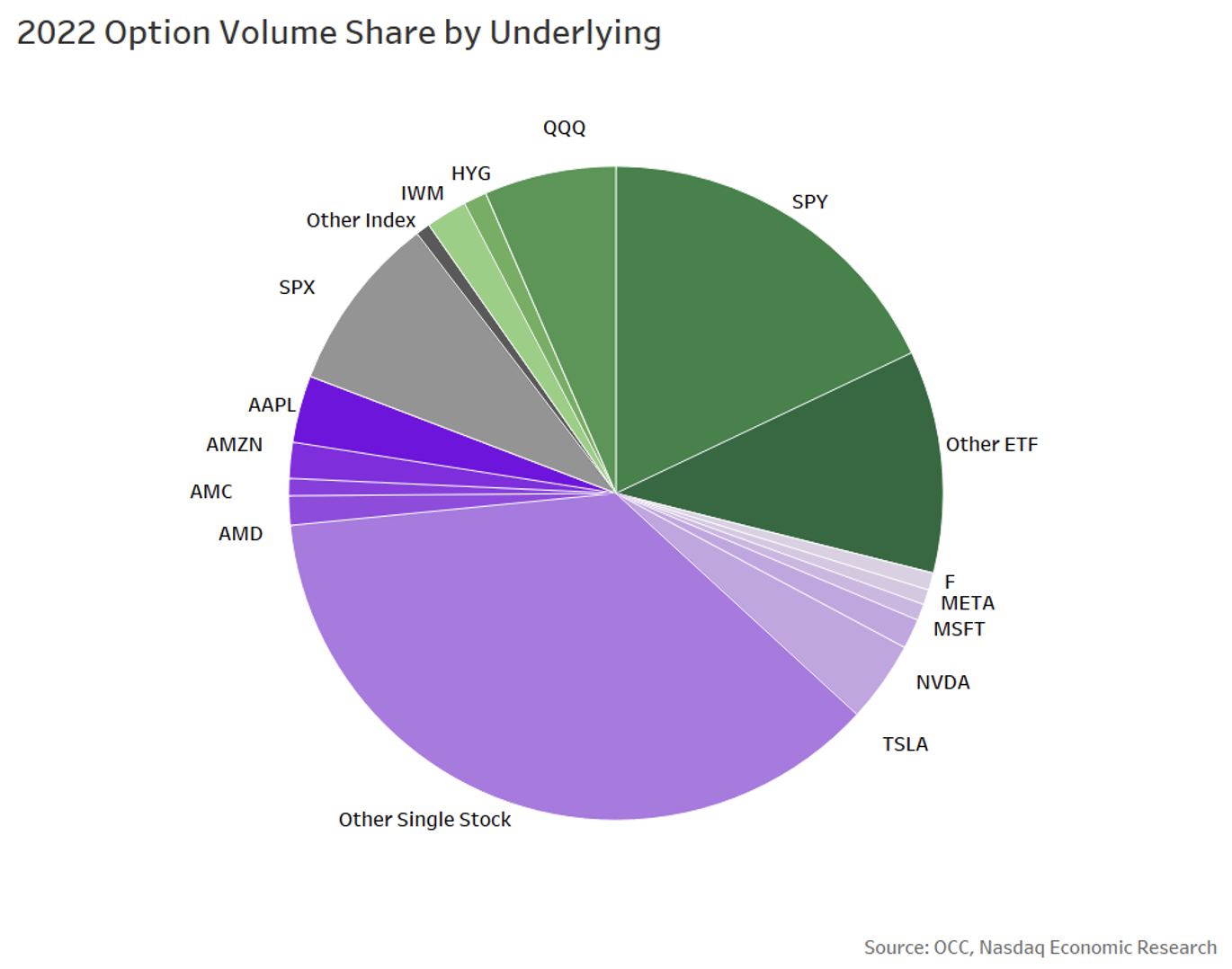

Each day, the options market trades around 40 million contracts. That’s up from 15 million in 2010 and less than 2 million in 1999. However, as we see in Chart 1, most of the volume is concentrated in a small number of underlying securities – with Nasdaq-100 and S&P 500 exposure adding to ~30% of all contracts traded on a typical day.

The data in Chart 1 also shows that index options contribute a relatively small proportion of total volume, at just over 9%. In contrast, ETF options offer a much larger amount of portfolio hedging liquidity, adding to nearly 39% of all contracts trading.

Although single stock options are the largest contribution to options ADV, we can see in Chart 1 that their liquidity is also concentrated in very liquid underlying securities, including TSLA, AAPL, AMZN and NVDA, adding to 20% of all single stock options trading. Importantly, those underlying also trade over $35 billion each day.

Chart 1: The majority of options trading is in very liquid underlying assets

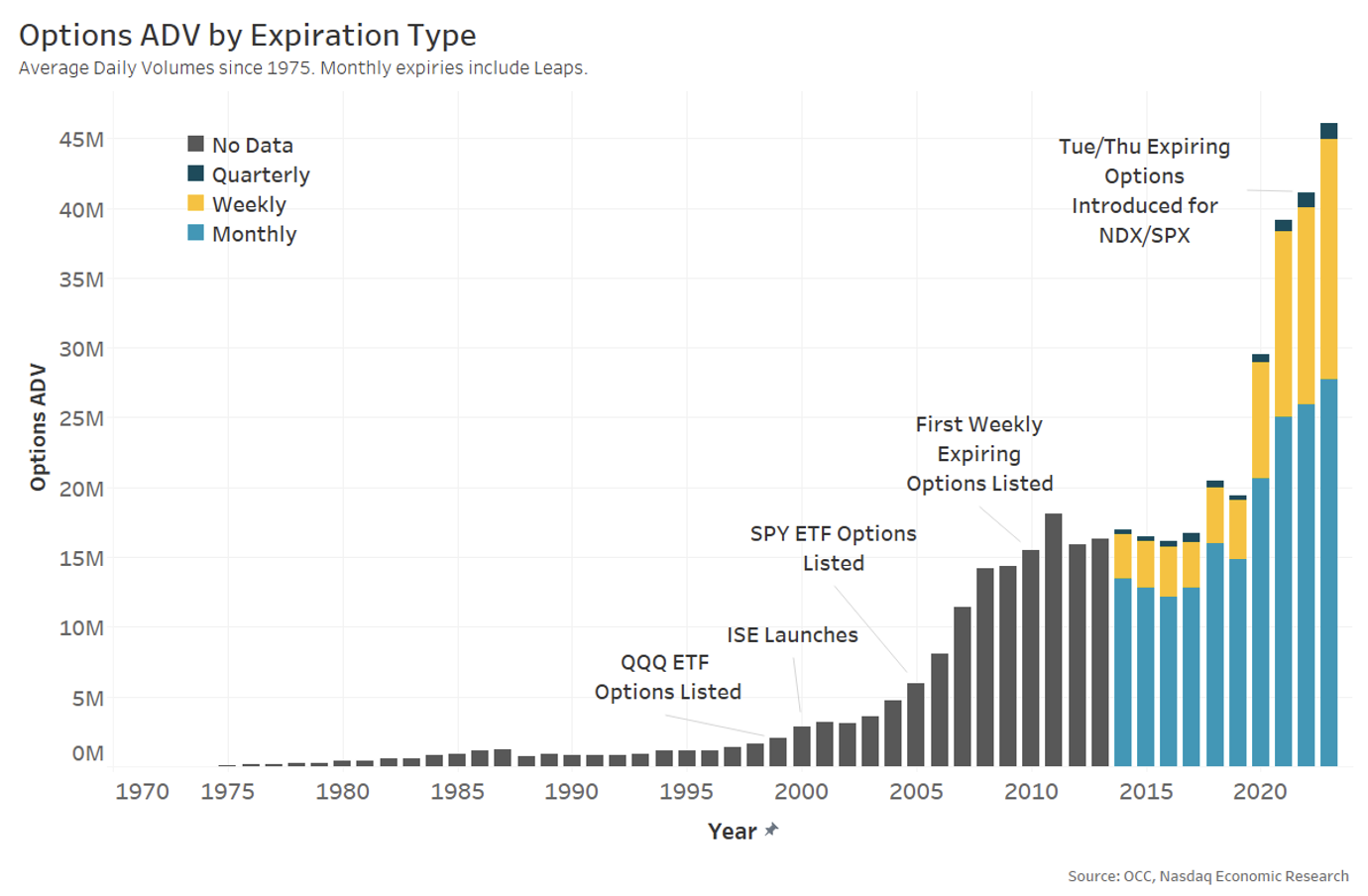

Just like we have seen in the stock market, activity in options has been consistently increasing since the 1990s. That’s partly because of an increase in the choices of options products available.

We saw in a recent study that there are numerous ways that options can enhance or modify a portfolio’s return profile — from protecting against selloffs to increasing portfolio income. However, each strategy benefits from using options in different ways.

- Portfolio income strategies benefit from more frequently selling shorter-dated options where the option is more likely to expire unexercised, allowing the portfolio to retain premiums.

- In contrast, those buying portfolio insurance on a long-term position may prefer to buy longer-dated options, so they only pay the option premium once.

We see that these investor preferences have led to the introduction of many more product choices for traders. From the introduction of QQQ and other ETF options in 1999 and then SPY options in 2005 to the addition of weekly option expiries in 2010 and the addition of weekly options that expire on different days of the week, allowing customers to truly align their options protections with cashflows and valuation cycles.

Chart 2: Historical options volume by expiration type

Although none of those innovations led to a significant jump in options trading, each has contributed to making options more useful to investors, increasing trading activity over the longer term.

More choices result in more cross-market option hedging trades too. That’s because of how options work.

A market maker can’t simply hedge an option trade with an underlying stock hedge – and lock in profits – like they can for ETFs.

- As the price of an underlying security increases, more calls will become “in-the-money,” making the option price return higher than the underlying stock hedge return.

- As the time to expiry falls, the chance that an option will end “in-the-money” (or not) becomes less uncertain, making the option value fall (time decay) even if the stock price has barely changed.

- With an increase in volatility, there is a higher chance that an option will reach expiry “in-the-money,” making an option worth more even if a stock price has barely changed.

These daily price changes (in the underlying) create profits or losses in a delta-hedged portfolio (directionally agnostic). However, traders can use algebraic and derivative equations to break these costs into components — like Gamma, Theta and Vega — sometimes called the “Greeks” because, in textbooks, algebra literally uses the Greek alphabet. Using other options, which have offsetting Greeks, can allow market makers to hedge these non-underlying costs better than simply hedging with stocks.

What are my “options” to trade options?

OTC options markets (that use ISDA’s with institutional investors) allow for full customization of option terms, from strike prices to expiry dates to notional sizes and sometimes how payoffs work.

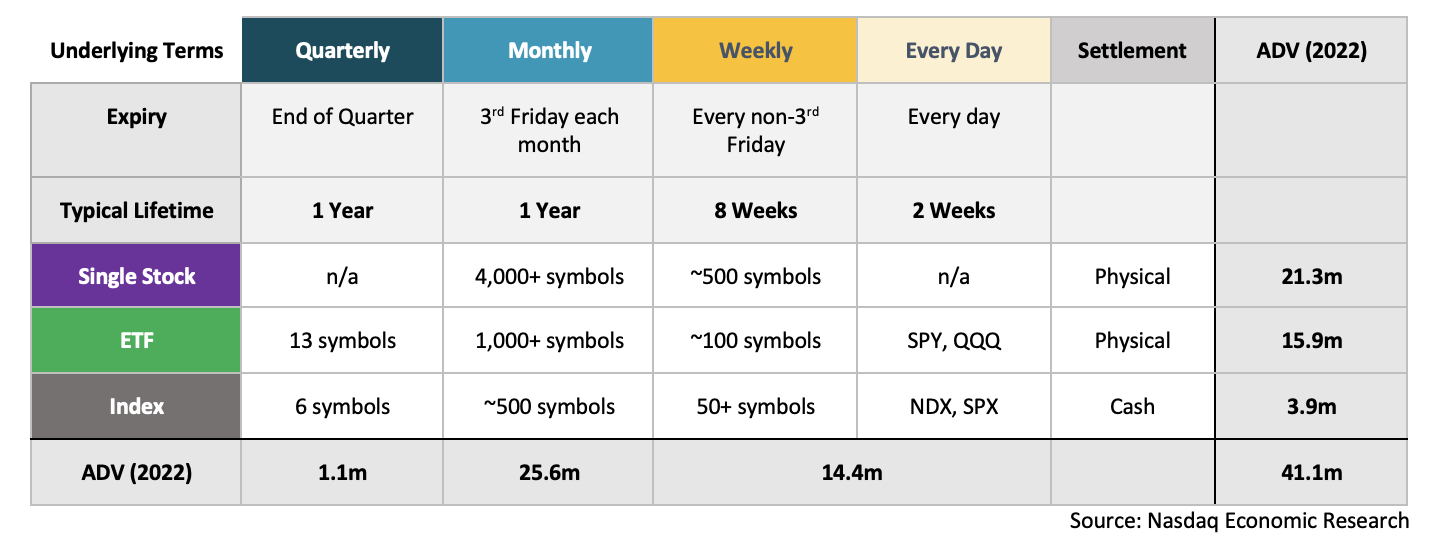

The structure of exchange-traded options is more consistent. However, to cater to different investor needs, options have evolved so that they:

- Track different underlying instruments, such as stocks, ETFs as well as indexes.

- Expire with different frequencies: Any unexpired options include a lot of uncertain returns, including potentially a lot of theta (time decay). Some investors prefer to protect portfolios with less theta, which requires more frequent expiries than each quarter.

- Settlement, which can occur with the delivery of the underlying (physical) or a cash payment for the amount of “in the moneyness” the option expires with (cash). For investors who want to hedge against losses but want to retain exposures, cash settlement would be preferred. Today, equity and ETF options settle physically, while index options are cash-settled.

However, not all underlying securities have all these choices for options. In fact, only the most liquid options tend to offer a full range of investor choices. For example, only the most liquid indexes and ETFs in the world offer option expiries for every day of the week.

Table 1: Different option underlying, expiry frequencies and settlement conventions (note, Symbols refers to the same underlying exposure. Say AAPL, or QQQ or Nasdaq-100)

All options last for weeks (or sometimes years)

Although we see in Table 1 that some underlying securities have options that may expire on every day of the week – it's important to realize that all options have a much longer lifecycle. If we look at the over 8,000 options that expired during December, around half were more than one year old when they were listed, with some being listed more than three years before their expiry. Even weekly options were almost all listed for at least seven weeks before their expiry. For example:

- Quarterly options are often listed over a year before the quarter of their expiry date. In reality, there are only a few underlying exposures with Quarterly options – including SPY, IWM, EFA, XLE, XLF SLV and GLD ETFs, as well as SOX, BKX , XAU and OSX indexes

- Monthly options can be listed years before the month of their expiry date, although they are more commonly listed a year before their expiry.

- Weekly options are usually listed seven weeks before their expiry date.

- So-called “daily” options are actually weekly options with expiries on different days of the week and have a duration of at least two weeks.

Some options expire in the open, others in the close

We looked at the impact of the expiry of futures and options, so-called “triple witching” day, on market volumes back in 2021. We found that:

- Equity index options, which settle in cash, expire in the open auctions. That, combined with equity index futures, made the open auction around 10 times larger than on a normal day.

- Stock (including ETF) options, which settle in physical, expire in the close auctions. That, combined with index rebalance trades from S&P and FTSE, made the close auctions around five times larger than normal.

However, triple witch only refers to the monthly options that expire on the third Friday of the month.

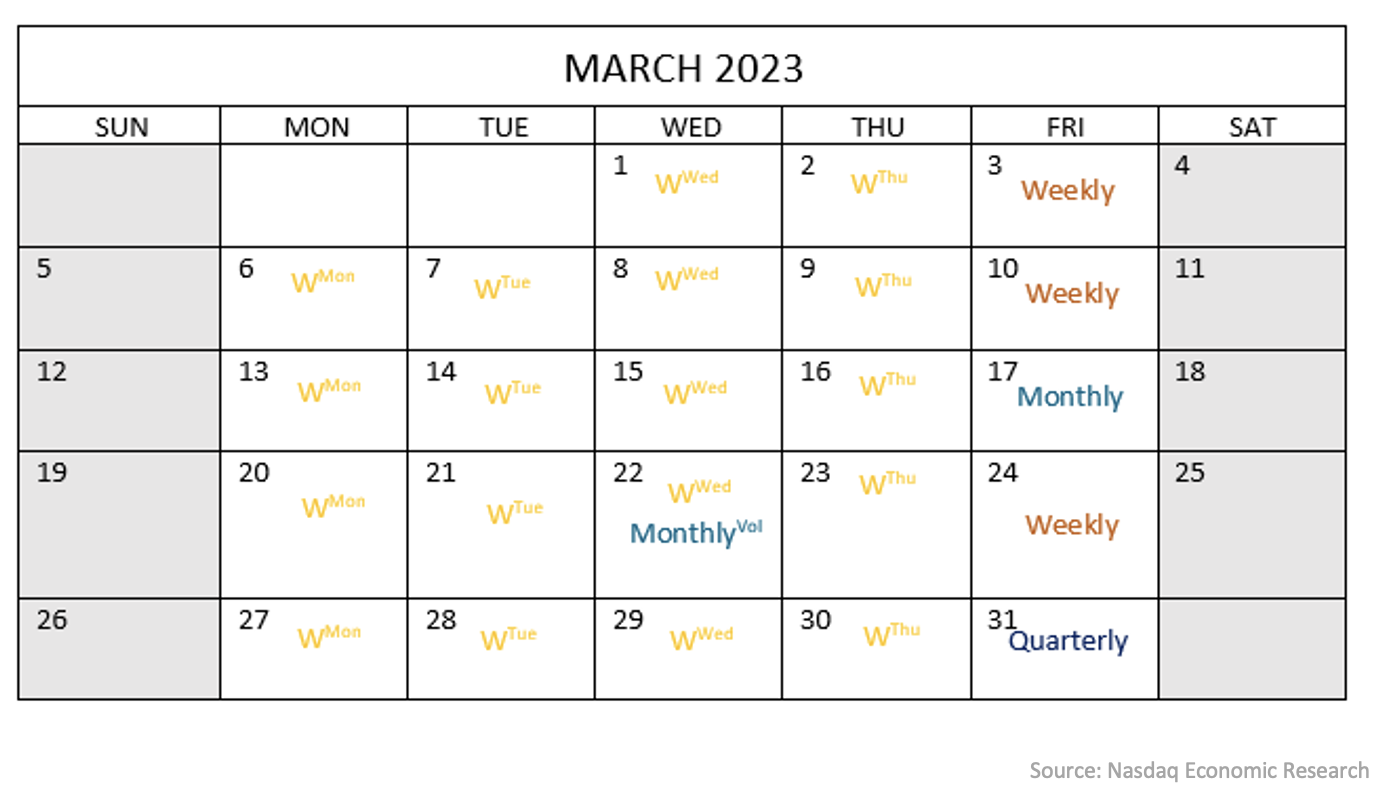

As we see in the calendar:

- Quarterly options expire on the last business day of each quarter (so month-end of March, June, September and December).

- VIX options, which are also monthly options, expire on the Wednesday that is 30 days before the third Friday of the following calendar month.

- Weekly options have expiries every (non-3rd) Friday.

- The two most liquid portfolio underlyings (NDX/QQQ and SPX/SPY) have weekly options on indexes and ETFs that expire each day of the trading week.

Chart 3: A calendar view of when different options expiry dates fall

When do investors buy options?

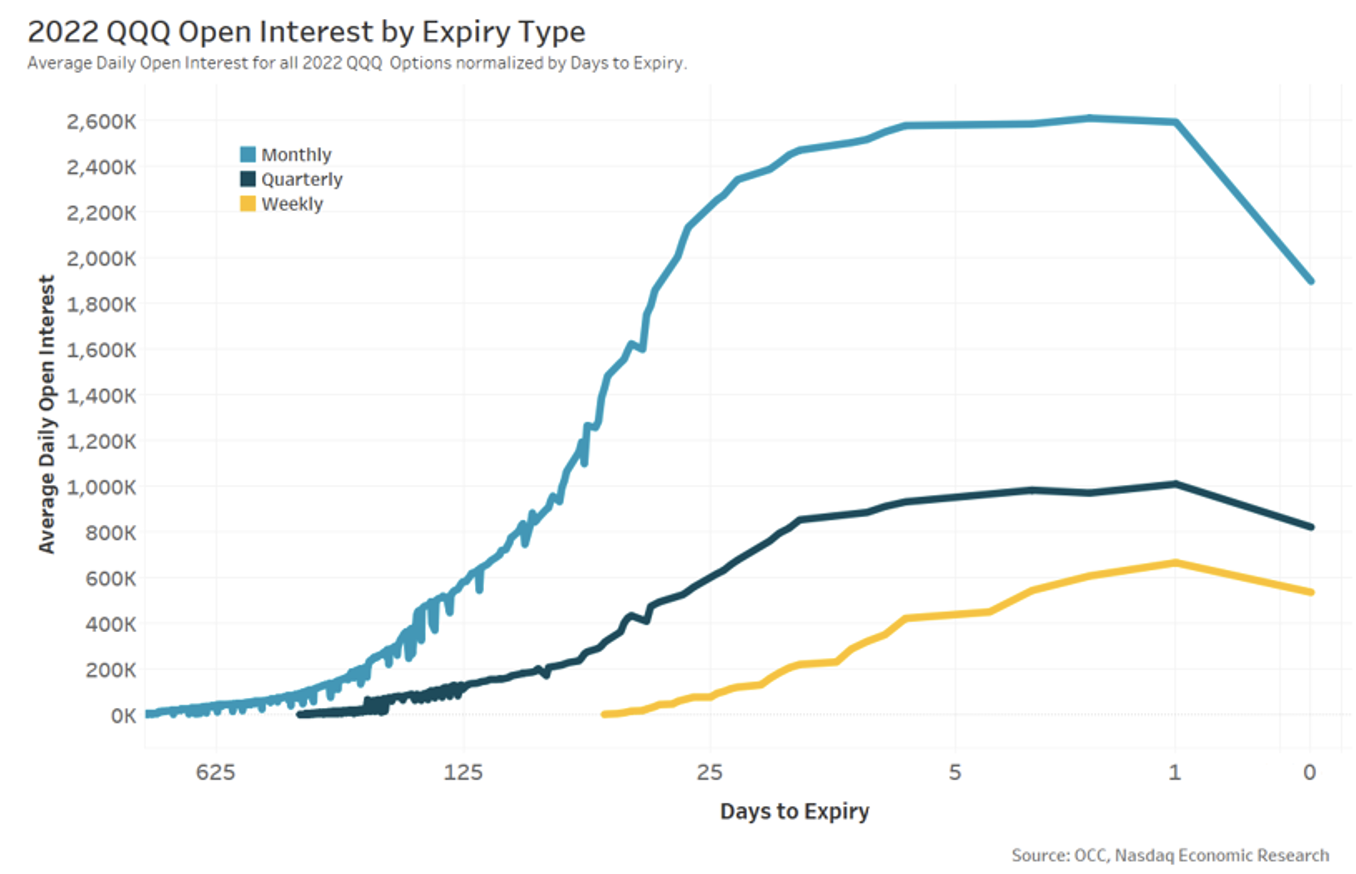

If we look at an example for QQQ options, we can see how investor interest changes throughout the lifetimes of different option expiries.

Open-interest data shows the level of investor exposure from inception until expiry. Chart 4 shows that almost all options start with a small open interest that increases consistently as the time decay falls.

Importantly, Chart 4 shows that even for so-called “daily” exercise options, there is open interest more than one month before expiry.

The data also shows a significant number of open positions are closed during the last day the options trades, locking in known profits and preventing physical settlement rather than risking an unknown underlying close benchmark, and the administration is required to exercise (or be assigned on) and settle options in-the-money.

Chart 4: Example open interest over an options lifespan

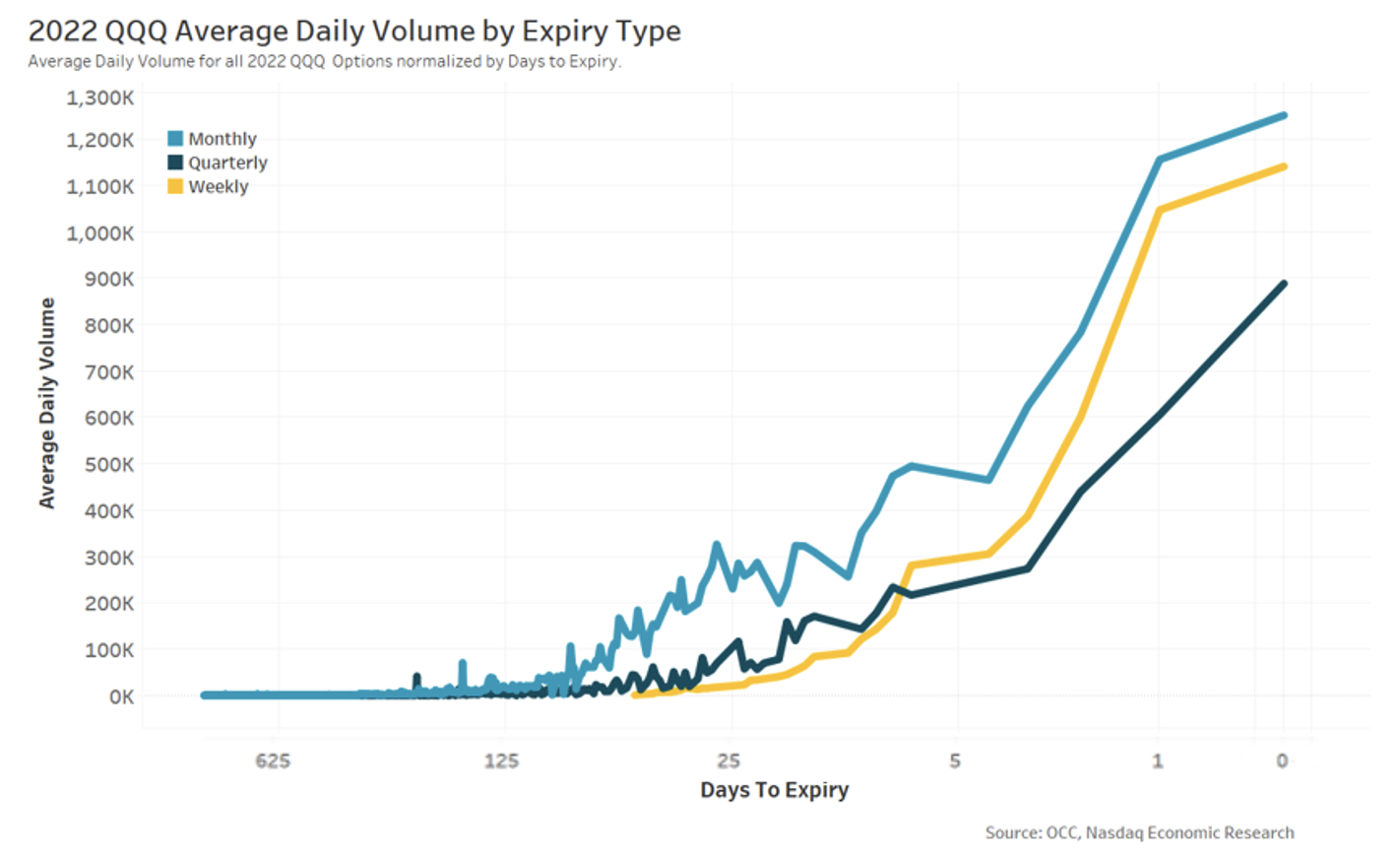

We could also look at trading activity the same way. Again, the data also shows that options typically start with a smaller trading interest, which increases as you near the expiry day. Undoubtedly, the closing of positions that we see in Chart 4 contributes to the elevated trading we see on expiry day in Chart 5.

Interestingly, the level of trading in the last month of each option’s life is consistent, whether we look at quarterly, monthly or weekly expiries.

As Chart 5 shows,

- For QQQ quarterly options, around 14% of all trading happens on the day of expiry, as traders finalize positions and close positions where they don’t want to run risks into the auction.

- For monthly options, around 7% of all trading happens on the day of expiry,

- Despite their shorter lives, for weekly options, around 23% of all trading happens on the day of expiry, with around 77% of all trading in the last week of the option’s life.

Chart 5: Example ADV (contracts traded) over an options lifespan

What does this all mean?

Options provide investors with more portfolio return profile choices — from insuring a portfolio against losses to earning income on top of a portfolio’s dividend yield.

Different use cases suit options with varying terms to maturity and even expiry dates. As a result, the market has evolved to offer options ranging from over two years (monthly and quarterlies) to two weeks (“so-called dailies”). For the most liquid portfolio options, investor demand has led to the establishment of weekly options that expire on each and every (other) day of the week.

As more investors realize the benefits options can provide and choose to add them to their portfolios, it’s no surprise that options markets have seen consistent growth that has persisted now for over 40 years.

Other Topics

Market Infrastructure

Phil Mackintosh

Nasdaq

Phil Mackintosh is Chief Economist and a Senior Vice President at Nasdaq. His team is responsible for a variety of projects and initiatives in the U.S. and Europe to improve market structure, encourage capital formation and enhance trading efficiency.

Read Phil's Bio